- This article forms the first chapter of the whitepaper from Trade Finance Global (TFG) and the Bankers Association for Finance and Trade (BAFT): “From lenders to leaders: Banks in flux”.

- The COVID-19 Pandemic brought about a total restructuring of global trade networks to a once-in-a-generation extent.

- With tariffs, disruption en masse is starting to seem less generational and more commonplace.

Saying that tariffs have been transformative for global trade is, by now, a cliche. However, the impact of those tariffs in facilitating and accelerating trade reconfiguration – from nearshoring to South-South trade – is yet to be fully reckoned with.

The only thing that’s certain is uncertainty

The uncertainty brought about by the recent tariff war pushed corporates to break new ground in their response.

“We’ve had uncertainty in the past with the previous disruptive events, but not to this level,” said one participant.

Responding to every latest development is not only exhausting but futile, with the tides turning in an instant. Instead, corporates have come to expect the uncertainty and are planning around it: For example, by diversifying to new, low-risk markets like Australia and New Zealand, or taking advantage of fresh trade agreements to access new markets at a lower cost. The UK’s recent trade deals with the US, EU, and India, for example, could provide an opportunity for UK corporates to diversify into new markets or find new suppliers.

In summary, large corporates are delaying investment decisions until they have more clarity about the current geopolitical and tariff-related developments. As a result, banks are not seeing large-scale supply chain and market transformations just yet – especially as those are often costly, time-consuming, and a large strategic commitment.

This could change towards the end of the year as the tariff-related dust settles and the impact of new regulations becomes clear. In the UK, the next budget (due to be announced on 26 November 2025) is rumoured to include changes in taxes levied on banks and digital services providers as well as incentives for companies relocating to the UK. This is likely to give corporates more confidence about the regulatory landscape – for better or for worse – and solidify some of the recent trends around supply chain reconfiguration.

Market mayhem… or a lack thereof

While each tariff announcement seems to be immediately bringing tumbling stock prices across the world, the long-term reactions of markets and corporates have been far more measured. Even the 4% fall of the S&P Global index that followed Trump’s memorable Liberation Day announcement in April was quickly recouped. Markets appear to be partially buoyed by faith in TACO (Trump Always Chickens Out) as Trump paused measures for three months just a few days after the initial announcement.

Overall, while we know reactions have not been drastic and supply chains have survived mostly unscathed so far, the overarching impression – from roundtable participants and Sibos panellists alike – is that tariff impact will be measured in years, not days. Therefore, just a few months out from the initial announcement and with some tariffs yet to take hold, it is impossible to predict what their more transformative long-term effects will be – if any.

Tariff whiplash

“Not quite my tempo,” jazz band instructor Terrance Fletcher (played by actor JK Simmons) tells Andrew Neiman (Miles Teller) in the 2014 film ‘Whiplash’. In the film, it’s something of a turning point, the last, considered piece of feedback Neiman would receive before Fletcher becomes a monster, abusing his pupil to no end under the guise of pushing him to become a jazz drumming great.

The learning? When you’re not keeping tempo, if you can’t tell whether you’re rushing or dragging, you risk getting a cymbal thrown at your head – or the equivalent in trade sanctions.

Previous supply chain shocks, like the COVID-19 Pandemic, offer little guidance on how to handle tariffs. The questions raised by this year’s geopolitical shocks – on themes such as nearshoring, physical and conflict-related risks, and cybersecurity – are leading to a dynamic landscape that banks and corporates have never dealt with before. The resilience needed to handle all these risks, as well as any new ones that may arise, necessitates corporates to have broad-based strategies around their supply chains and buying and selling markets, which many of them are struggling with.

Banks are feeling the same shocks as their clients, but they have taken on an additional advisory role, helping corporates navigate the shocks and plan their next moves. Just as the pandemic led to a renaissance of relationship banking, tariff shocks are motivating banks to help clients strategically as well as financially. At the same time, though, banks themselves are managing their own response to the uncertainty, which often involves, in the words of one participant, “hovering around waiting for what’s next”.

What can be moved, will be

Different trade flows are changing at different speeds in response to the tariffs, but commodities are a good predictor of what future changes might involve. “Where people can move quickly, they have: you can see it in the commodity flows, which have moved already,” said one participant.

US tariffs on China, at nearly 60%, are some of the highest the US has imposed – and may be set to rise by another 100% soon. They have led to a drastic fall in commodity flows between the two countries this year.

For example, soybean – once the single largest American export to China and a key US agricultural commodity – has stopped being exported to China entirely. China once bought over half of all US soybean exports; now, orders have dried up completely since May 2025, a month after the tariffs were announced.

On the other hand, countries that have recently signed trade deals with the US may be looking to fulfil their commitments to buy a set value of US goods – a provision the US has been including in most of its recently announced trade deals. This will most likely translate to higher US energy and agricultural exports to Asian countries such as South Korea, Japan, and Indonesia.

Regionalisation and China-isation

Changing a soybean order to adjust to tariffs is one thing, but more long-term commitments, like deciding where to build a factory, will naturally adapt more slowly. However, while investment in Asia faltered in the immediate aftermath of the tariff announcements, it is quickly bouncing back – especially as Chinese companies set up factories in neighbouring countries to avail of lower tariff rates when exporting to the US.

Chinese manufacturers, especially in automotive and some industrial sectors, are increasingly setting up factories and assembly plants in Africa. This is largely to avoid high tariffs in Western markets and tap into Africa’s growing demand. For example, Chinese car brands like BYD, Chery, and Great Wall Motor are investing in local assembly in South Africa and exploring other regions.

Overall, regionalisation has been growing quickly this year, especially in emerging economies, far outpacing the growth of international trade flows. As corporates nearshore their supply chains and South-South trade and investment increases, intra-regional trade is growing by double digits in many emerging markets, much faster than it is in Europe. Much of this is driven by China, which has far outdone the rest of BRICS in terms of emerging markets investment and trade.

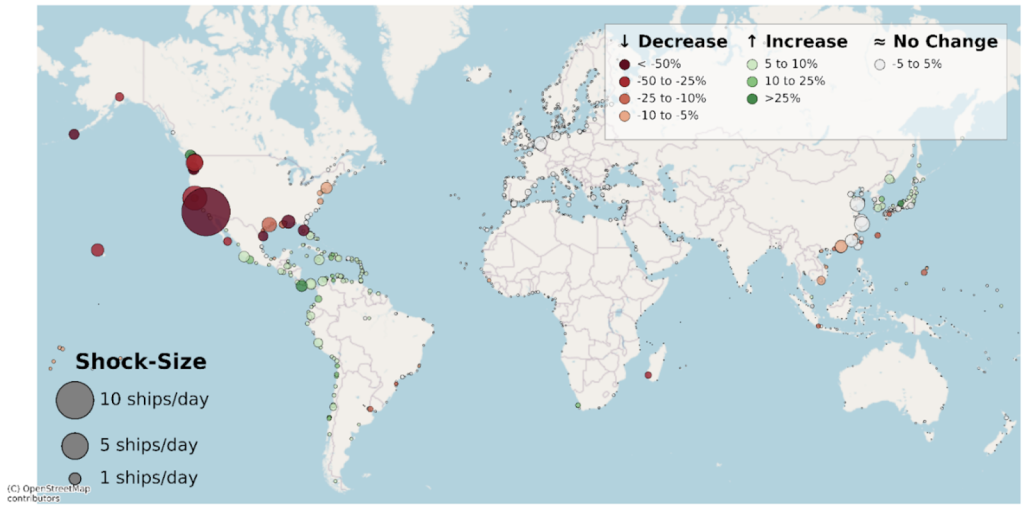

Source: Complexity Science Hub. As countries adapt to tariffs, changing trade relationships are affecting shipping routes and ports across the world, benefiting some South American and East Asian shipping hubs. The map shows the impact of US-China tariffs on ship arrivals in the major global ports.

The tariff upshot

Supply chains are reconfiguring to adapt, especially in the fast-changing world of commodities, but this is not having the destructive effect many feared. Instead, an increase in intra-regional trade and a renewed focus on diversification are counterbalancing the negative effect of tariff uncertainty on investment.

Around the world, corporates have generally accepted the price hikes created by tariffs, and are adapting to them, not just by changing their supply chains, but also by looking elsewhere to reduce costs. Investments to this end – often in the form of tech or AI-related projects – have become about more than just cost optimisation. Instead, they are crucial for resilience and long-term survival.

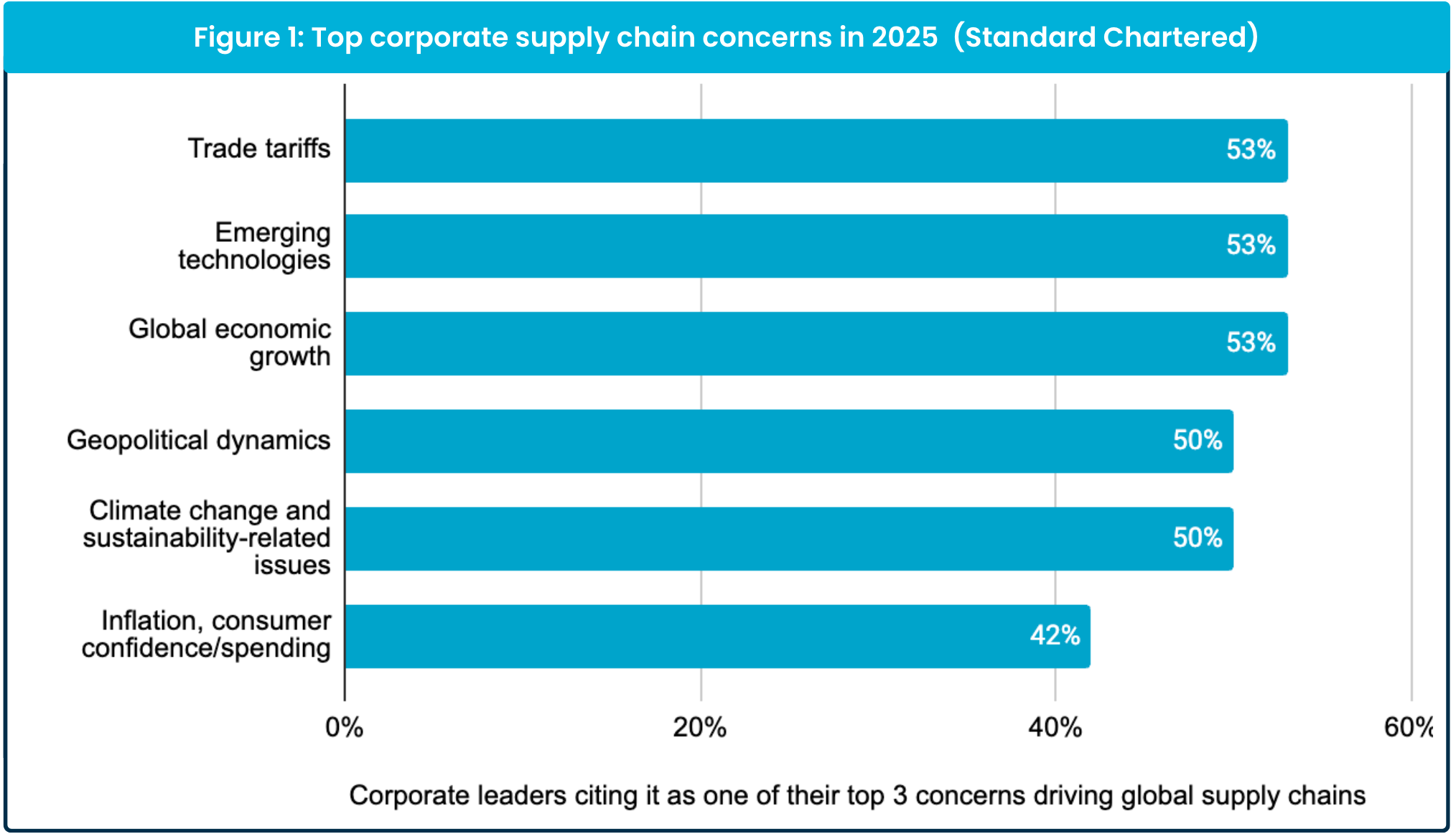

Source: Standard Chartered Future of Trade: Resilience Report, 2025

Banks are responding to these pressures themselves while at the same time taking on a leading role for their clients, advising them and helping them anticipate and prepare for the next shocks.