- Trade credit insurance (TCI) protects businesses against non-payment by customers in open account transactions, compensating suppliers for outstanding debts lost to insolvency, protracted default, or political risk events.

- Beyond basic protection, TCI delivers four core value propositions: financial risk coverage, ongoing buyer creditworthiness monitoring, the ability to safely grow turnover by extending higher credit limits, and improved working capital.

- TCI is not a standalone solution but works best alongside internal credit management practices.

Trade credit insurance (TCI), also referred to as accounts receivable insurance, is a financial risk management tool designed to protect businesses against the risk of non-payment by their customers. It applies primarily to business-to-business transactions conducted on open account terms, where goods or services are delivered before payment is received.

At a basic level, TCI covers accounts receivable – the money that’s owed for open account transactions – in situations where a customer fails to pay due to insolvency or protracted default, a political risk event, or other defined credit events. In such cases, the insurer compensates the supplier/ policyholder for a portion of the outstanding debt.

However, beyond its function as a form of protection, TCI can also play a broader role in supporting robust credit risk management, safe growth, and improved working capital.

A significant proportion of global trade is conducted on open account terms, often ranging from 30 to 90 days. While these terms facilitate commercial activity and strengthen customer relationships, they also introduce risk. When offering open account terms, suppliers are exposed to the possibility that their customers may delay payment or default entirely.

This exposure can be particularly significant in industries with high transaction volumes, long supply chains, or customer concentration. In such contexts, even a small number of defaults can have a disproportionate impact on cash flow and profitability.

TCI addresses this exposure by transferring part of the financial risk associated with receivables to an insurer, thereby stabilising financial outcomes and reducing uncertainty.

Value propositions of TCI

TCI is one of several tools available to manage credit risk. Alternatives include self-insurance through bad debt reserves, letters of credit (LCs), and factoring arrangements. Each approach has different cost structures, risk profiles, and operational implications.

Compared to these alternatives, TCI combines risk transfer with ongoing risk assessment and monitoring. It is typically used alongside internal credit management practices rather than as a complete substitute for them.

The value of credit insurance can be understood across four main propositions:

1. Risk protection

The most direct function of TCI is to provide financial compensation in the event of non-payment. By covering a portion of accounts receivable, it reduces the financial impact of a customer’s non-payment to a supplier, and helps maintain business continuity. This protection is particularly relevant in situations involving large exposures to individual customers, businesses operating on very thin margins or in sectors experiencing financial stress or volatility.

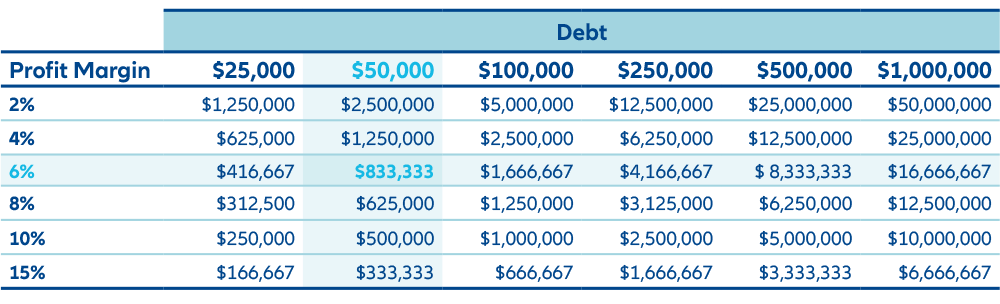

The light blue figures highlighted in Table A show the example of a company working on a 6% profit margin and does not use TCI. The company experiences $50,000 unpaid receivables debt. Because they’re uninsured, they’d need to generate an additional $833,333 just to break even – 16 times the value of their preexisting debt.

This is based on the notion that, to recover a loss of $50,000, you must generate enough new sales so that the 6% profit on those sales equals $50,000. It can be expressed as a formula, whereby:

Required sales = 50,000 / 0.06 = $833,333

Table A:

2. Credit risk assessment and monitoring

TCI supports suppliers/ policyholders through comprehensive credit risk assessment and ongoing monitoring of buyer portfolios. Insurers evaluate buyer creditworthiness using financial data, payment behaviour, sector insights, and macroeconomic trends, assigning credit limits that define the level of insured exposure – the maximum amount the insurer is willing to reimburse. As conditions evolve, credit limits evolve accordingly, intending to provide timely insights and support informed credit decisions.

In addition to risk assessment, TCI enhances the efficiency of credit management functions. Activities such as evaluating customer risk, setting credit limits, and monitoring receivables can be resource-intensive, particularly for companies with large or geographically dispersed customer bases.

3. Safe turnover growth

By providing structured frameworks, external data, and continuous monitoring, TCI reduces administrative burden and improves consistency in decision-making.

This enables businesses to scale their credit management processes more effectively while maintaining strong risk discipline.

TCI enables safe, profitable growth. Many companies limit expansion due to concerns about customer creditworthiness, particularly in new markets or with new buyers. With TCI, businesses can oftentimes extend higher credit limits to existing customers, enter new markets with greater confidence, and offer competitive payment terms to win business. Increasing a customer’s credit limit based on improved risk visibility may allow a company to expand turnover.

In the example in Table B, a company has a comfort credit exposure of $500,000 to a customer, and under a credit insurance policy, the credit insurer has agreed to support a higher limit of $750,000. This means the company can now extend a higher credit limit to its customers – effectively selling more products to them, and therefore earning more revenue. They are protected against the risk of non-payment by the insurance policy.

Based on a 10% margin and receivables which turn eight times a year – meaning the business collects credit payments from outstanding sales – this one customer could yield an additional $2,000,000 in revenue and $200,000 additional gross profit.

Table B:

4. Financial and working capital implications

Accounts receivable are a key component of working capital. Their reliability and quality influence liquidity, borrowing capacity, and overall financial stability. Receivables that are insured may be viewed more favourably by lenders, as the risk of non-payment is partially mitigated. This can positively impact borrowing terms and access to credit, although outcomes depend on the specific arrangements between the business and its financial institutions.

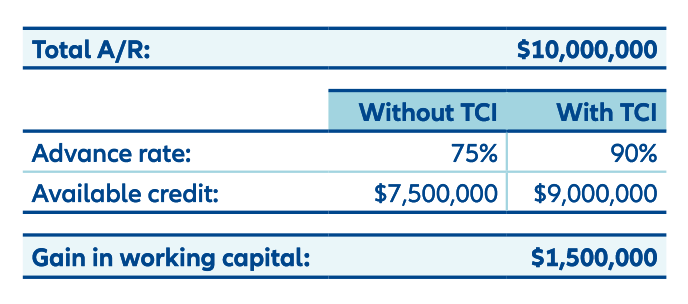

Similarly, insured receivables may influence lending arrangements by improving the perceived quality of collateral. In some cases, this can lead to higher advance rates or increased borrowing capacity, as demonstrated in Table C. This increase provides higher immediate cash flow against accounts receivable.

Table C:

The bank voice: RBS Invoice Finance

“RBS Invoice Finance Limited (part of the NatWest Group) and Allianz Trade acknowledge that TCI could be an effective tool to mitigate against counterparty risk and strengthen the overall quality of receivables. For suppliers operating internationally, TCI could offer important protection against buyer insolvency, protracted default, and certain political risks.

While funding decisions and credit assessments remain subject to RBS Invoice Finance’s credit approval, insurance limits might not always align directly with funder appetite – an insured receivables portfolio could contribute to a more holistic assessment of non‑payment risk. In this context, TCI may support risk management within existing funding structures and help businesses continue trading through periods of heightened exposure, such as customer concentration or rapid growth, by mitigating the financial impact of insolvency events rather than replacing lost revenue.”

– James Vandenbergh-Harwood, RBS Invoice Finance (part of NatWest Group)

—

In summary, TCI is a multifaceted tool that supports businesses in managing the risks associated with trade on open account terms. While its primary function is to protect against non-payment, it also contributes to credit assessment, turnover growth, and potentially gains in working capital.

Its effectiveness depends on how it is integrated into broader credit management practices and how actively it is used in decision-making processes.