- Access finance

- Case studies

-

Informing today's market

Financing tomorrow's trade

Soft commodities trader

Due to increased sales, a soft commodity trader required a receivables purchase facility for one of their large customers - purchased from Africa and sold to the US.

Metals trader

Purchasing commodities from Africa, the US, and Europe and selling to Europe, a metals trader required a receivables finance facility for a book of their receivables/customers.

Energy trading group

An energy group, selling mainly into Europe, desired a receivables purchase facility to discount names, where they had increased sales and concentration.

Clothing company

Rather than waiting 90 days until payment was made, the company wanted to pay suppliers on the day that the title to goods transferred to them, meaning it could expand its range of suppliers and receive supplier discounts.

Get Trade Finance

Informing Today’s Market, Financing tomorrow’s Trade.

-

- Case studies

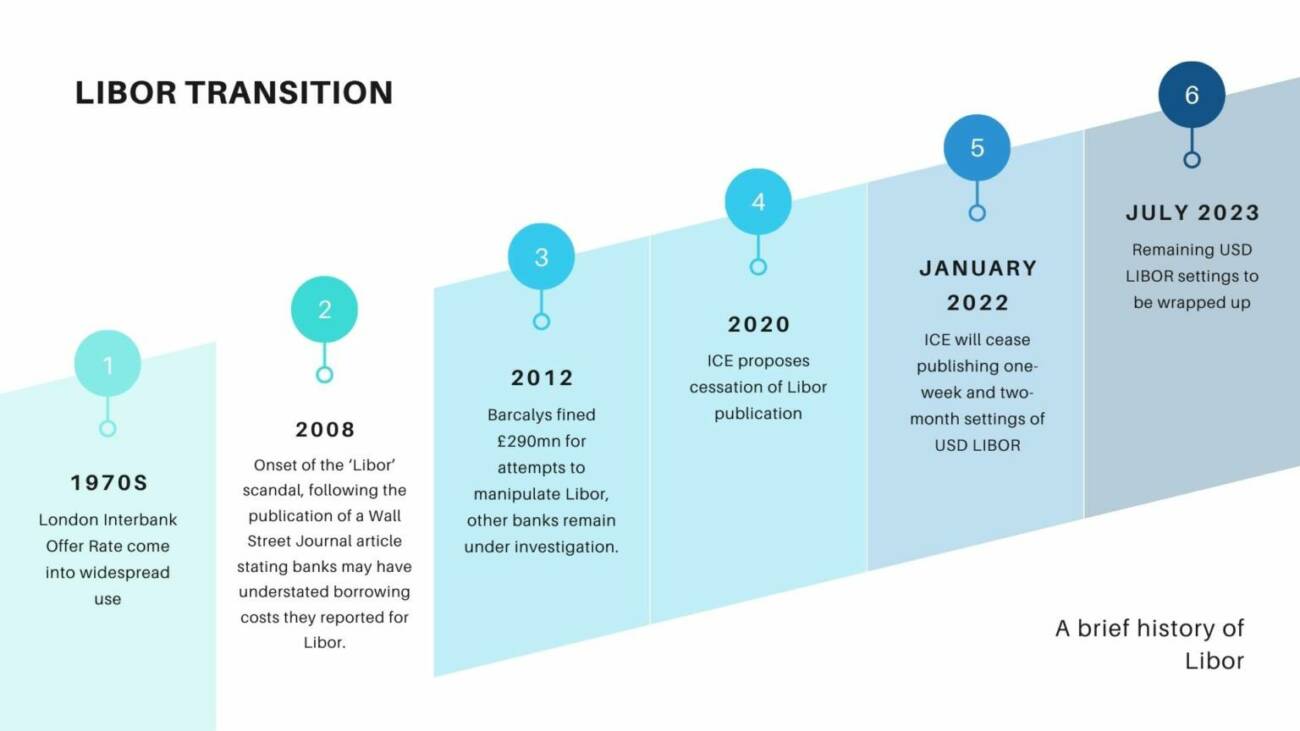

LIBOR Transition

Access trade, receivables and supply chain finance

We assist companies to access trade and receivables finance through our relationships with 270+ banks, funds and alternative finance houses.

Get startedContent

Welcome to the ITFA-TFG LIBOR hub. The change from the London interbank offered rate (LIBOR), the “world’s most important number”, to risk-free rates compounded in arrears as opposed to calculated upfront before the start of an interest period, is one of the most significant legal, commercial, and regulatory change events to hit the financial markets this century.

An Introduction to LIBOR

The purpose of this hub is to provide resources to the trade finance community. LIBOR transition is particularly challenging for trade finance. As we describe later, many trade finance products either require a discount rate or are offered to borrowers who are, for a number of reasons, unable to deal with the challenges posed by the use of a rate calculated in arrears.

The International Trade and Forfaiting Association (ITFA) is closely following market developments. It has released a number of newsletters with a view to providing guidance on the issues and how to solve them. In particular, and following the partnership now in place for a few years, ITFA has worked with the Bankers Association for Finance and Trade (BAFT) to modernize the master participation agreement. We will be releasing amendments to the market standing document in due course.

LIBOR Podcast – An introduction to the LIBOR transition

In 2014, the Financial Stability Board, or FSB, recommended that banks should use Risk-Free Rates (or, RFRs) as alternatives to LIBOR, the London Interbank Offered Rate, as well as other term-based interbank reference rates. Despite delays due to the COVID pandemic, term-based interbank reference rates are being phased out, and according to the Loan Markets Association, LMA, 2021 has seen a sharp increase in loans referencing RFRs. By the end of 2021, it’s anticipated that these rates will be discontinued, transitioning to the Sterling Overnight Index Average, or SONIA for short, and, for US Dollar benchmarks, the Secured Overnight Financing Rate, SOFR). But what does this mean for trade finance, trade finance documents such as Master Participation Agreements, products, and what are the current recommendations?

In this podcast, we discuss:

- A brief history of LIBOR, why it exists currently, and whether the ‘LIBOR transition’ is related to the LIBOR market scandals that we saw between 2008-2012

- Updates from the Loan Market Association and others for the trade finance community

- Why is LIBOR transitioning to Risk-Free Rates, and what is a Risk Free Rate?

- What is SONIA, and what is SONIA TSRR?

- What is SOFR and will there be a term SOFR?

- Trade finance products that currently reference Libor term rates

- Is the alternative to use the cost of funds?

- Are the RFRs produced compatible with standardised trade documents such as the BAFT and ITFA MPAs?

- Will switching outstanding contracts be a big job?

- ITFA and the Libor transition for trade finance

What is LIBOR?

LIBOR is an interest rate benchmark administered by Intercontinental Exchange Benchmark Administration (ICE).

It is the average interest rate at which major global banks borrow from one another. It is quoted for five currencies (the U.S. Dollar, the Euro, the British Pound, the Japanese Yen, and the Swiss Franc), and serves seven different maturity tenors (overnight/spot next, one week, one month, two months, three months, six months, and 12 months). This combination leads to 35 different LIBOR rates that are reported each day.

ICE asks a designated panel of major global banks at what rate they would be willing to lend to other banks. They then use the trimmed average of the responses to determine the rate each day.

LIBOR is used in an assortment of financial products around the world, not just interbank products like rate futures and options. Many personal financial products also make use of the LIBOR rates, such as individual mortgages or student loans.

About the LIBOR transition

Why is it being transitioned?

LIBOR is being phased out as a loan benchmark for a complex array of reasons. Among them are the role that it played in aggravating the 2008 financial crisis, scandals involving its manipulation, and the fact that it is based on increasingly infrequent transactions among banks, making the index less reliable and credible.

During the subprime mortgage crisis, many banks became reluctant to lend to each other. This led to LIBOR rate-setting banks reporting higher and higher rates. As LIBOR is determined by bank appetite to lend, the benchmark rates continued to increase each day, negating to some degree the efforts of global central banks to slash interest rates to stimulate the economy. Among other factors, these raising rates and reduced bank lending contributed to the Global Financial Crisis (GFC) even if they did not directly cause it.

Over the years there have also been instances of banks and traders colluding to manipulate LIBOR rates for their own gain. These scandals have challenged the validity of LIBOR and deterred panel banks from continuing their involvement in the LIBOR setting. The number of underlying transactions has declined in recent years whilst the question the contributor banks had to answer has not. The New York Fed estimates that transaction volumes for USD LIBOR have decreased from $200 trillion to less than $500 million since 2016. This decrease has reduced the reliability and credibility of the index and led to the desire for its replacement.

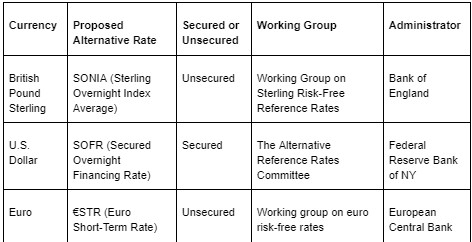

What will replace LIBOR?

Each LIBOR currency is to be replaced with its own unique Risk-Free Rate (RFR). The following table shows the proposed alternative rate for each currency as well as the group that is working towards the implementation of each.

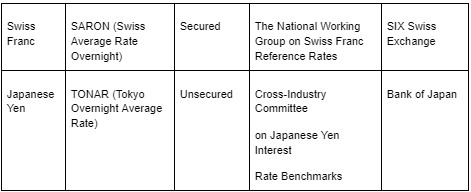

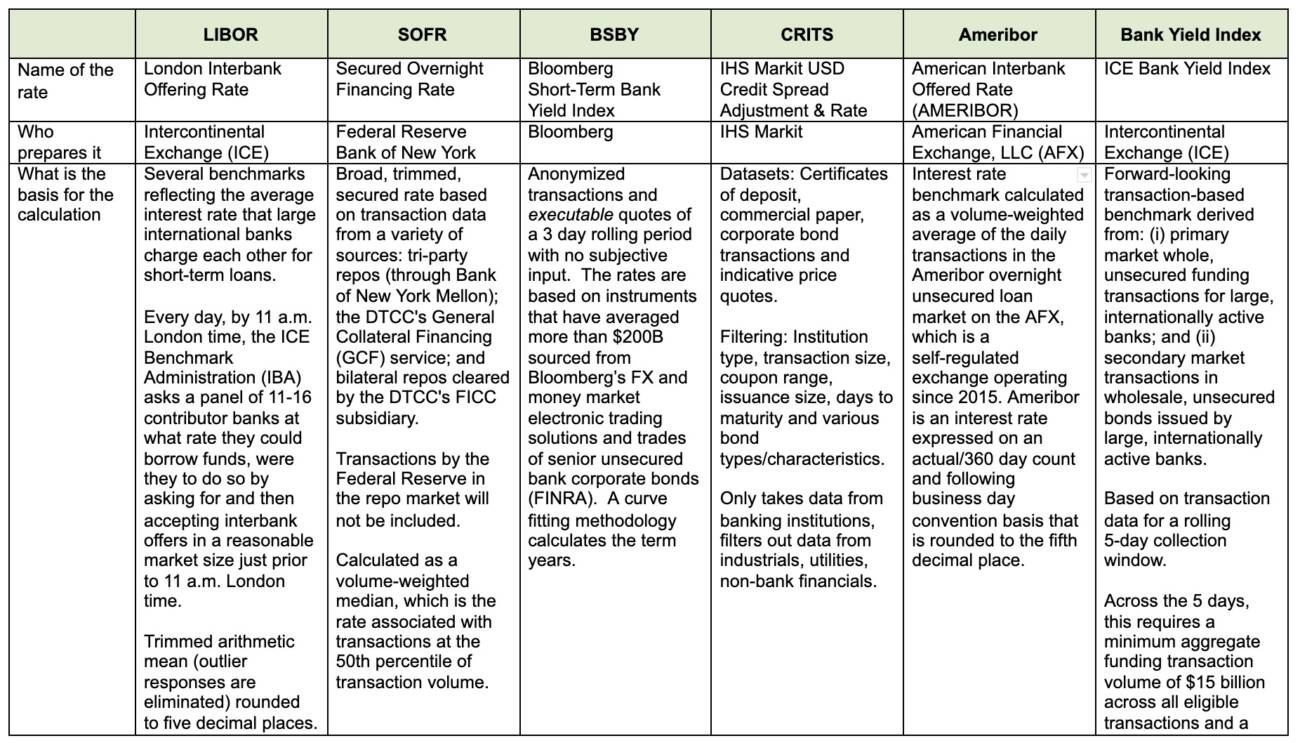

Cheat sheet – a useful chart showing alternatives to USD LIBOR

Includes LIBOR, SOFR, BSBY, CRITS, Ameribor and Bank Yield Index:

- Name of the rate

- Who prepares it

- What is the basis for the calculation

- What Tenors are available

- Where is it published

- If a “floor” included

- Is it IOSCO compliant

- Are there calculation or use contingencies

- Other considerations

Timelines

A number of jurisdictions are making efforts to create forward-looking rates that will replace LIBOR.

For the Sterling Overnight Index Average (SONIA), on January 11, 2021, after a six-month beta period, ICE and Refinitiv began live production of forward-looking term SONIA rates (TSRR). FTSE Russell is expected to release its TSRR as well. The Sterling Risk-Free Rate Working Group has advocated the market adopt a comprehensive shift to SONIA compounded in arrears, with the use of a TSRR being limited but inclusive of trade finance.

At present, the Sterling Working Group has not selected a single administrator among the providers, leaving the decision up to the industry participants. This is in contrast to the U.S. approach where the Alternative Reference Rates Committee (ARRC) plans to select a term rate administrator among the providers that responded to the request for proposal.

Provider interviews are currently underway by the ARRC and consultation on permissible use cases is expected. The ARRC was expected to recommend a term rate by the end of the first half of 2021, contingent on sufficient liquidity to produce a robust rate but has so far done so. Instead, it has indicated that a recommended rate may not be available by year-end and has encouraged users to consider alternatives and especially to consider rates using SOFR e.g. using the rate from the last interest period for the next.

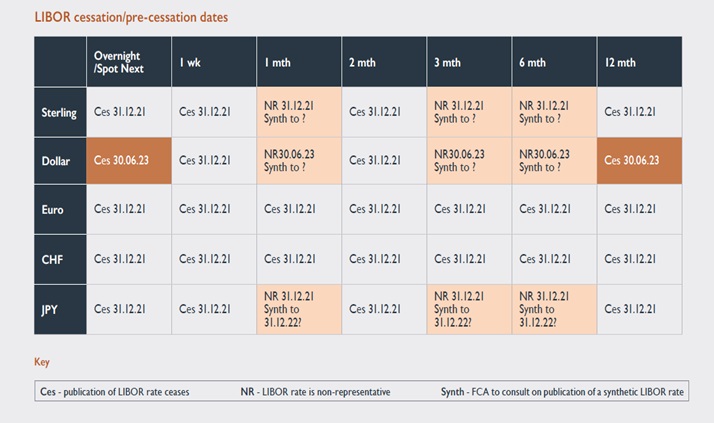

On 5th March, regulators and administrators in the UK announced that all LIBOR tenors, with the exception of the USD LIBOR (overnight and 1-, 3-, 6-, and 12- months) will cease to be published or become non-representative of the market (which means banks will not be able to use them except in very limited cases) at the end of 2021. The following table shows the dates and fates of the various tenor.

LIBOR transition and trade finance

The transition away from LIBOR, and especially USD LIBOR, will have a deep impact across a large number of financial markets but the impact on trade finance is different in certain respects.

Many trade finance assets are financed by discounting the asset or instrument underlying the asset. For this market to continue to function efficiently, all parties involved need to determine a mutually agreeable third-party rate to apply to the discount. In the case of sterling, as mentioned above, multiple providers are or will be publishing term SONIA and, as it is not yet clear which provider will become the market’s preferred option, settling on an agreeable rate may pose a challenge. In the case of US Dollars, the problem is that there may not be any official publisher(s) until after the end of 2021.

Forward- vs. Backward-looking Risk-Free Rates

Discounts must be calculated using a forward-looking interest rate. The desirability of using forward-looking RFRs for trade finance transactions has been recognized by industry bodies and currency working groups, including the ARRC, the Working Group on Sterling Risk-Free Rates task force, ITFA and the BAFT IBOR Transition Working Group. Despite this, the development of forward-looking RFRs has lagged behind that of backward-looking RFRs.

In addition to discount products, regulators have accepted that it may be appropriate to use forward rates for certain borrowers who need certainty on their interest expenses before the start of an interest period. This could be because, for example, the borrower needs to apply for allocation of foreign currency reserves, which can be a lengthy process. The need to introduce new operating systems and technology may also be unaffordable for many smaller or emerging market banks.

For banks able to price using LIBOR or RFRs there may also be difficult decisions over which of their counterparties can be permitted to use forward rates which may involve judging how ready or sophisticated a customer is to use RFRs and if the bank should agree to such use when their own regulator may be pushing them to impose widespread use of RFRs across the customer base.

Currently, forward-looking RFR term rates are only available for Sterling, while exposures in export finance and pre-export finance transactions are largely in US dollars. The impending cessation of LIBOR coupled with these facts creates a need to carefully consider references to forward-looking RFR term rates in the documentation and to identify appropriate alternatives. The ITFA newsletter setting out possible approaches can be found here.

Update – September 2021

The recent authorisation of a forward-looking US Dollar term rate by the Alternative Reference Rates Committee (ARRC) in the United States is the most significant development in the transition from LIBOR for trade finance banks and customers since the process began. Whilst the new recommended rate behaves operationally in a very similar way to LIBOR, changes will need to be made to existing documents and procedures and some important commercial decisions need to be made. As part of their ongoing efforts to assist and inform the market through the LIBOR Hub, ITFA, Sullivan and TFG have collaborated to bring you a guide to the issues to be tackled and some ideas on how to solve them. The guide can be found here on the Hub here.

Credit Adjustment Spreads and cost of funds

Conceptually, RFRs should be lower than LIBOR rates as they do not contain a risk premium. Consequently, and in order to ensure that lenders are not disadvantaged, a credit adjustment spread (CAS) can be added to the RFR. Alternatively, the margin can be increased. The market standard documentation produced for transitioning LIBOR allows for the addition of a CAS to the RFR. Where a CAS is added, this can be calculated either by looking backwards from a specified date or by looking forward. The UK Working Group on Sterling Risk-Free Rates task force has recommended a five-year lookback period based on the historic median between LIBOR and the RFR. This rate was published and fixed on 5th March 2021. Whilst this may seem artificial, it has been adopted by many market participants and has the advantage of simplicity and consistency across products. A forward-looking rate will need to be calculated using forward-looking basis swaps and is arguably closer to reality but will also be more complicated to calculate.

The use of a CAS is important when transitioning the legacy book to maintain economic equivalence but arguably much less so for new loans post-LIBOR. It is likely that any uplift will be added to the margin. It is also possible that the cost of funds, traditionally more widely used in trade finance products than other markets, will become more popular as a simple way of avoiding some of the issues described above. It should be noted that many regulators discourage the use of cost of funds except as a fallback of last resort

Export Credit Agencies

Export credit agencies (ECA) are private or quasi-governmental institutions that act as an intermediary between national governments and exporters. They generally offer a variety of products and services and are involved in supporting the full range of trade and commercial transactions—from short-term commodity exports to long-term capital projects and project finance. Often, these ECA loans reference LIBOR when determining the rate to be applied for a product.

Agents and lenders on relevant loans need to check the terms of the ECA cover documents to determine whether the consent of the ECA is required for a change to the basis on which interest on the loan is calculated.

The likely amendment and consent process may be time-consuming for ECAs, particularly if it results in any impact on an ECA’s budgeting procedures. It should be noted that whilst export loans are mentioned as a possible case where term rates could be used, in reality, many borrowers will be able to use RFRs.

Specific Guidance from ITFA and Resources

ITFA Guidance

Members need to take a number of decisions when approaching LIBOR transition:

- Should you transition to a new rate or stay with LIBOR? If you want to stay with LIBOR for how long will your Regulator allow you to use it for new transactions?

- Should you use a forward-looking term rate or a backward-looking compounded rate?

- What do you use as a fallback rate?

- Is the use of the cost of funds or fixed rates possible and permissible from a regulatory perspective?

Transition or stay with LIBOR

As we have made clear above, quotations for a number of currencies and tenors will disappear at the end of 2021 or become non-representative. For these currencies and tenors, the choice will be made for the market. However, for US Dollars, the currency used for most international trade, quotations will continue for most tenors into mid-2023. Members could therefore decide to continue using LIBOR until it disappears. The ability to do this will largely depend on the attitudes of regulators and the expectations and needs of clients.

In the US and UK, regulators have insisted that no new USD LIBOR loans are entered into after the end of 2021. Existing deals can be transitioned over a longer period and, for these, it will be permissible to continue to use USD LIBOR. Client or counterparty expectation may however force an earlier transition.

However, ITFA has many members outside of these countries. For these members, it may be possible to continue using USD LIBOR until it completely disappears subject to the views of their regulators.

This may create differentiated markets and could pose problems for inter-bank lending e.g. US or European banks may be asked to fund emerging market banks in LIBOR after the end of 2021 as the borrowing banks will want to lend in LIBOR but find themselves unable to do so.

Term rate or compounded rate?

The Sterling Risk-Free Rates Working Group and the Financial Stability Board have accepted the need for the use of term rates, see this Sterling RFRWG January 2020 paper and this FSB June 2021 paper. The general stance of the regulators is that term rates should be used sparingly and that the use of a compounded rate is possible and appropriate in most cases. One case where a compounded rate cannot be used is where discounting is involved as a deduction has to be made from the face value of the asset, usually a receivable or payable. Even in the case of loans, however, other counterparties commonly encountered in trade finance may be capable of using a compounded rate and will not need the comparative simplicity of a term rate. For example, borrowers under an ECA facility and bigger EM borrowers may be able to use compounded rates.

Where a term rate is necessary, numerous alternatives exist, see this ITFA paper. For US Dollars, the announcement by the ARRC of a recommended administrator of term SOFR has increased chances that a term rate will be available by the end of 2021 provided the ARRC’s term rate principles are met (essentially a deep and liquid derivatives market). See term rate principles here. There seems to be a growing confidence by ARRC that this might be achievable.

Alternatives exist to term SOFR e.g. AMERIBOR Ameribor® | The New Benchmark but their success will be determined by market adoption and regulatory direction possibly quite subtle.

Remember also the need to consider adding a credit adjustment spread as explained above.

Cost of funds and fixed rates

Why not avoid all these difficulties by just using cost so funds or fixed rates?

The use of the cost of funds is a reasonably widespread practice in trade finance. Will it continue or even expand?

Regulators would not encourage this. Indeed in some cases regulators are saying this cannot be used as the rate calculation must be transparent. Again, not all jurisdictions will have regulators with strong views on the subject and outside of the US and Europe, there may be none or little opposition.

Fixed or all-in rates are very similar but may be harder to use for loans with multiple interest periods. ITFA’s bulletin explains this in more detail.

The ARRC has formally recommended forward-looking CME SOFR term rate – what does this mean?

Sean Edwards, Chairman, ITFA, said: “In a significant development for USD LIBOR transition in trade finance, the Alternative Reference Rates Committee (ARRC), the body overseeing USD LIBOR transition in the United States, announced on 29 July 2021 that it is formally recommending CME Group’s forward-looking Secured Overnight Financing Rate (SOFR) term rates marking the completion of its transition plan. The ARRC has now given the market the missing piece of the jigsaw by providing much needed USD SOFR term rates administered by CME Group Benchmark Administration Ltd as a replacement for forward-looking USD LIBOR rates which can be used for trade finance transactions.

This announcement follows the ARRC’s press release on Monday 26th July 2021 when it announced a convention switch to SOFR First “recommending inter-dealer brokers change U.S. dollar (USD) linear swap trading from USD LIBOR to SOFR”. It also published its loan conventions and best practices for the use of a forward-looking SOFR term rates. The ARRC has accepted that term rates may be used for a wide variety of business loans including trade finance.

ITFA recommendations:

- Whilst the recommendation favours the use of the CME SOFR Term Rate, prominence is also given to the use of SOFR Averages (Applied in Advance) – the market will need to decide which rate should be used as its preferred rate recognising that the secondary rate could always be used as a fallback. It should also be remembered that USD LIBOR will continue to be published until June 2023 (although regulators are pushing for a switch by 31 December 2021 with, depending on the jurisdiction, only legacy contracts set to rely on USD LIBOR after that date), with other alternative term rate providers also existing, so there are multiple available options which may lead to a fragmentation of the market.

- Regulators in certain jurisdictions, such as in the UK, on the whole do not favour the use of term rates, recommending RFRs compounded in arrears as the norm; however trade finance is recognised as an exception in the UK and the US where a term rate is necessary for discounting products and for where transitioning to an overnight rate has been difficult, according to the ARRC announcement. Use of term rates for other trade products, such as loans where borrowers could use a compounded in arrears rate may not always be appropriate, so we suggest you consult the best practices guides issued by the relevant regulators or discuss the situation with them.

- Whilst most of the conventions for SOFR Term Rates are very similar to LIBOR, since both are forward-looking rates, there are some differences, most notably (i) Business Days which are linked to US Government Securities Business Days and (ii) fallbacks or unavailability of rates, (i.e. unavailability of SOFR Term Rate) , which the ARCC suggests could be the rate for the preceding Business Day, as long as that day is not more than three Business Days prior for USD LIBOR.

Resources

- Regulators and official committees

- ITFA guidance

- Publications from other trade associations

- Law firm publications

- Loan Market Association

- Alternative Reference Rates Committee