Estimated reading time: 5 minutes

Central Bank Digital Currencies (CBDCs) have infiltrated the agenda of countless innovation meetings at the world’s central banks.

In light of the ongoing shift to digitalisation, these and many other interested organisations have been actively investigating the potential impact that these digital currencies can have in trade and supply chain finance.

And those potentials are immense.

In this article, we will delve into the significance of CBDCs in international trade and supply chain finance, and scratch the surface of their potential to revolutionise the transactional landscape in the digital era.

What is a central bank digital currency?

A central bank digital currency (CBDC) is a digital version of a country’s currency that is issued by the country’s central bank and can be used by the general public, businesses, and government agencies.

They are designed to be a more efficient and secure form of money, designed specifically for digital transactions and can be used for a variety of purposes, including payments, remittances, and settling international trade agreements.

In the world of supply chain finance (SCF), their release has the ability to facilitate faster and more secure transactions, making it easier for counterparties to transact across the value chain.

For example, the use of CBDCs could allow a buyer and seller to conduct a trade transaction instantaneously, with the buyer’s currency automatically converted into the seller’s currency at the current exchange rate.

While they were once largely considered a far-off pipe dream of digital currency enthusiasts, the vision of a CBDC-populated world is becoming increasingly grounded in reality.

Pilot projects such as mBridge – a joint project between the Bank for International Settlements Innovation Hub and four central banks – have already demonstrated the wholesale feasibility of CBDCs for cross-border payments.

Similar pilots are also underway in Mainland China, Hong Kong and a number of other jurisdictions, showing the technology’s applicability from a retail perspective.

Standard Chartered and PwC China recently launched a whitepaper, “Co-creating the future ecosystem of banking with Central Bank Digital Currencies”, looking to explore the commercial usage of CBDCs and how they could transform retail finance.

James Lee, partner of advisory digital, at PwC China said, “Greater collaboration between industry bodies and regulators across jurisdictions will be critical to validating CBDC use cases and creating a programmable banking ecosystem that fulfills the potential of CBDCs,”

Central banks are motivated to develop CBDCs because they offer the potential for greater financial inclusion, faster payments, and improved accuracy and security.

A CBDC-fueled shift in cross-border payments

When comparing CBDCs with existing payment systems like SWIFT and correspondent banking, there are several key differences to consider.

One of the main advantages of CBDCs is that they can offer increased speed and efficiency in processing transactions. With traditional payment systems, transactions can take several days to clear, but with CBDCs, transactions can be completed in a matter of seconds.

CBDCs also offer increased security and transparency compared to traditional payment systems. Since the digital tokens are issued and regulated by central banks, there can be greater accountability and oversight compared to traditional payment systems.

Another advantage of CBDCs is that they are more accessible to individuals and businesses who may not have access to traditional banking services. With CBDCs, anyone with a smartphone and an internet connection can participate in the global economy, regardless of their location or financial status.

Standard Chartered and PwC China believe CBDCs will be instrumental in breaking down the barriers of trade finance.

Traditional payment systems like SWIFT and correspondent banking have served the international trade space well and are unlikely to disappear, but they are likely to be joined by CBDCs.

For many of the small and medium-sized enterprises struggling to access the financial system in the current climate, this will be a welcome addition.

Making supply chain finance digitally deeper

Supply chain finance programs, where networks of suppliers to major corporate partners leverage these connections to acquire the financing they need, have helped inject an amplitude of financing since they came into prevalence.

Unfortunately, many of the benefits that these programs convey do not trickle down to deeper tiers of the supply chain and instead tend only to benefit the buyers and suppliers that already have sound credit ratings.

This has meant that many of the SMEs further down the chain still face barriers when seeking to access these financing solutions due to their lack of scale, collateral, or credit history.

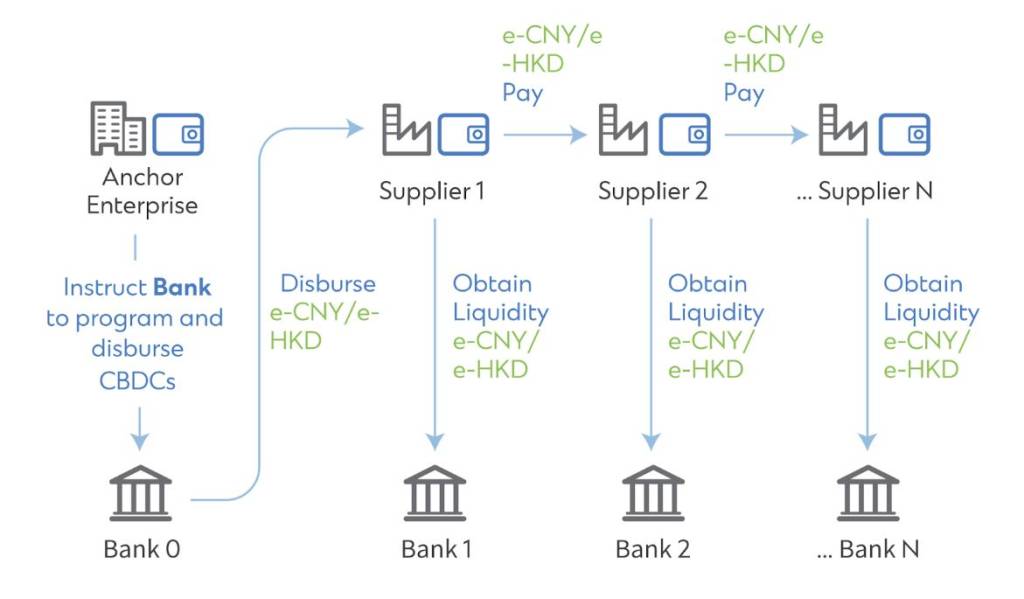

Programmed CBDCs, however, can help to change this, with benefits being passed more easily down the chain, with these SMEs able to benefit from the fact the good they produce is ultimately being sold to a financially reliable global corporation.

For instance, a CBDC could be programmed to initiate a payment from the buyer directly to the SME once the goods have been received and verified, greatly streamlining the process and giving those at the bottom of the chain the chance to access much-needed financing.

By combining trade and payment information, the CBDC can be programmed according to payment conditions so as to become a new form of trade finance instrument.

For example, the flagship corporate can pass a programmed CBDC to its suppliers, who can subsequently use the token to pay deeper-tier suppliers who can then use it to serve as collateral for financing.