Estimated reading time: 8 minutes

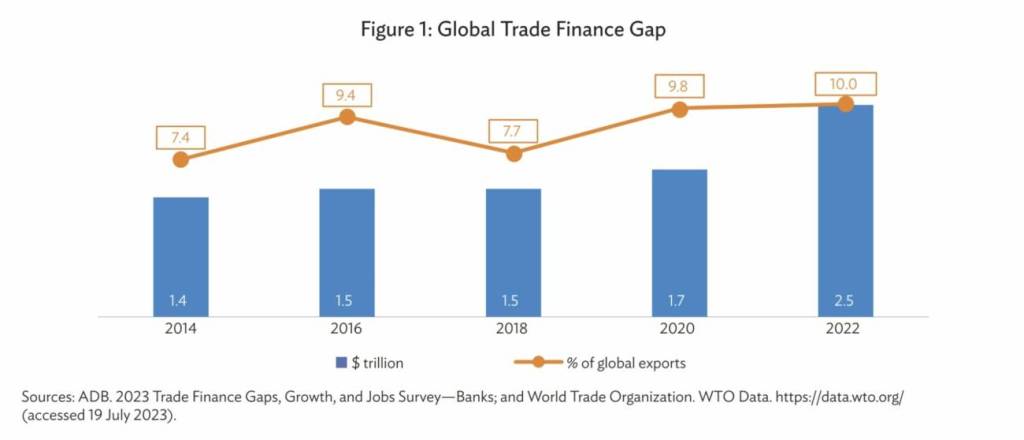

In its largest single-period increase since its inception, the Asian Development Bank’s (ADB) latest Trade Finance Gaps, Growth, and Jobs Survey indicates that the trade finance gap in 2022 rose to $2.5 trillion, up from $1.7 in 2020 and $1.5 trillion in 2018.

The 2023 ADB report provides a comprehensive analysis of the current state of global trade finance, offering insights into the challenges and opportunities that lie ahead, particularly in the wake of a global pandemic that has disrupted trade flows and financial systems.

This latest report takes a global view, emphasising that the trade finance gap is a worldwide issue, suggesting that international cooperation is key to resolving these challenges, a point that resonates more strongly in the current geopolitical climate.

It underscores the need for international cooperation to address the global trade finance gap and calls for a concerted effort from all stakeholders, including governments, financial institutions, and international organisations, to find sustainable solutions.

Don’t have time to read the full report? Here are Trade Finance Global’s (TFG) Five key takeaways that stakeholders in the trade finance ecosystem should consider.

1 – The trade finance gap is widening

The report reveals a significant escalation in the global trade finance gap, which has surged to an estimated $2.5 trillion in 2022, up from $1.7 trillion in 2020.

This is not just a statistical increase; it’s a sign of deepening systemic issues in global trade. The widening gap underscores the persistent challenges that small and medium-sized enterprises (SMEs) face in accessing trade finance, further exacerbating economic disparities.

Richard Wulff, executive director, ICISA said, “Credit insurance narrows the trade finance gap by providing security (the policy) based on its unrivalled ability to assess risk. ICISA’s trade credit (re)insurance members have a credit rating of at least A- (S&P or equivalent). This credit rating takes the place of that of the buyers when a financial institution finances invoices. Other than banks, who are not equipped to assess large numbers of (sometimes very small) risks, this is the credit insurance community’s core competency, aided by large databases of information on diverse buyers and automated, semi-automated and (as an exception) manual procedures.”

Evolution of the Global Trade Finance Gap (2014-2022)

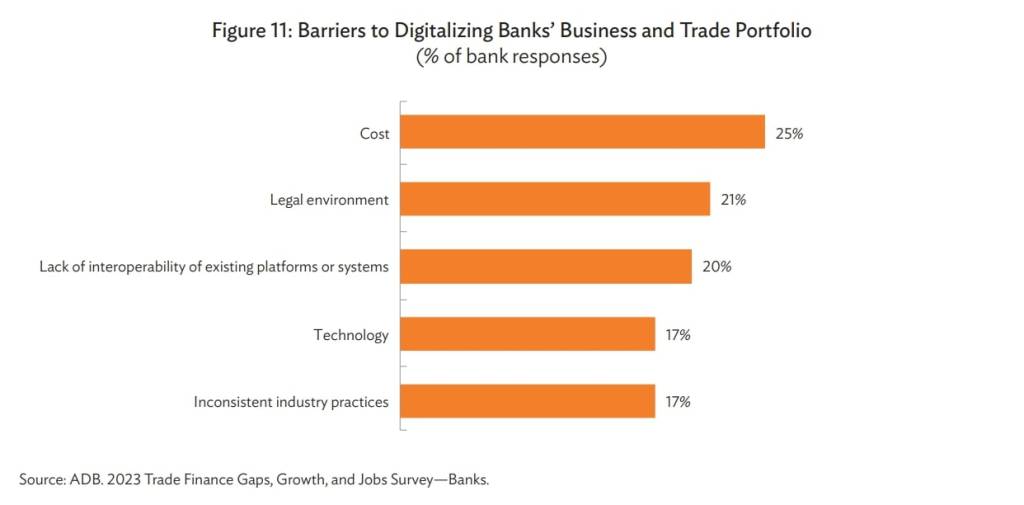

2 – Digitalisation is both a solution and a challenge

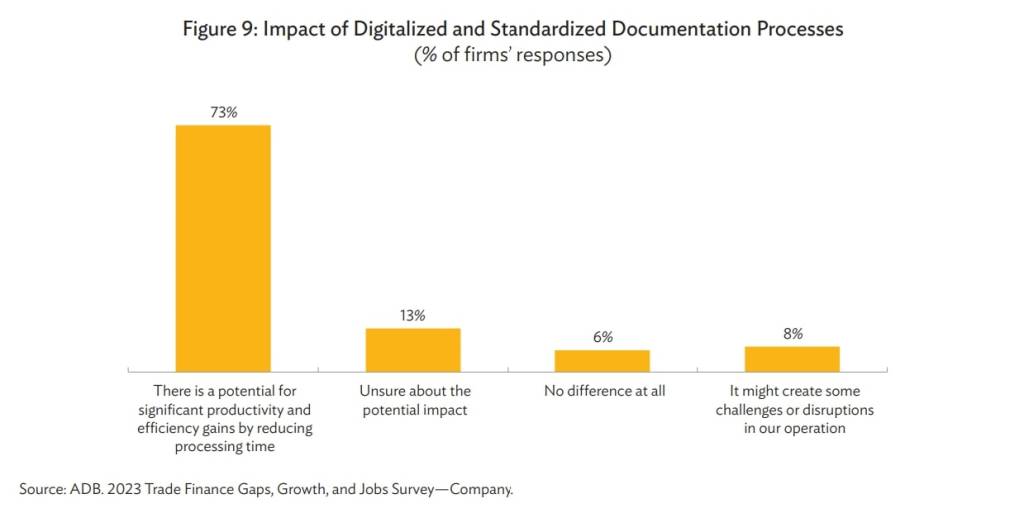

Digitalisation is commonly viewed as a remedy for the trade finance gap.

Seventy-three percent of the firms surveyed recognise that digitalisation and standardisation of trade documentation processes can provide significant productivity and efficiency gains.

While digitalisation offers solutions, it also presents challenges, particularly without standardised electronic documentation.

The absence of a unified digital framework hampers the full realisation of digitalisation’s potential benefits and will require industry-wide collaboration for effective solutions.

Pamela Mar, managing director of ICC DSI, told TFG, “ICC DSI is tackling standards harmonisation for trade data and processes in an inclusive public/ private process, whilst driving adoption through initiatives like the FIT Alliance universal EBL Declaration. This report rightly points out that sustainability linked financing could play a role in bridging the SME finance gap, and this too points to trade digitalisation as the key to generating verifiable trusted data for the financing process. The process is there, technology is there, and banks are ready. The missing link is legal recognition for electronic records. Adopting UNCITRAL’s Model Law on Electronic Transferable Records (MLETR) is a must for accelerated industry action.”

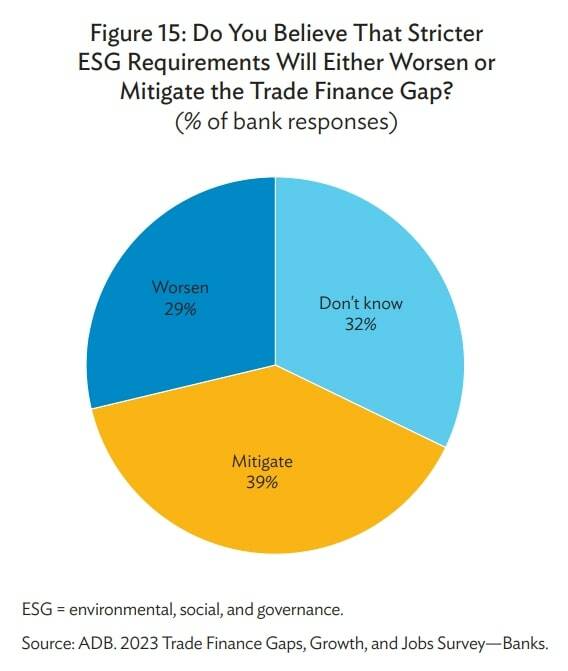

3 – Sustainability is an opportunity, but…

The results of the survey show that most banks have an accepted definition for green trade finance transactions – although these definitions often vary amongst banks – and are moving towards implementing sustainability-aligned financing with growing urgency.

While this is purportedly a step forward in terms of the environment, there are mixed views on how this will impact the trade finance gap.

Slightly more than one-third (39%) of bank respondents feel that stricter environmental, social, and governance (ESG) requirements will mitigate the trade finance gap. In comparison, slightly less than one-third (29%) believe it will contribute to worsening the gap. The remaining 32% of respondents indicated that they do not know.

Peter Mulroy, secretary general of FCI, told TFG, “ESG has changed mindsets among FIs and Corporates globally in recognition of the influence they have in changing behavior relating to supply chains. Although still in its infancy stage, we’re seeing more and more interest from FIs engaged in factoring implementing ESG strategy, but especially relating to large anchor buyer reverse factoring programs. However, we do not see ESG as an inhibitor to growth in factoring. ESG is one of the Strategic pillars of FCI today, in support of the importance it has in influencing behavior for a better tomorrow!”

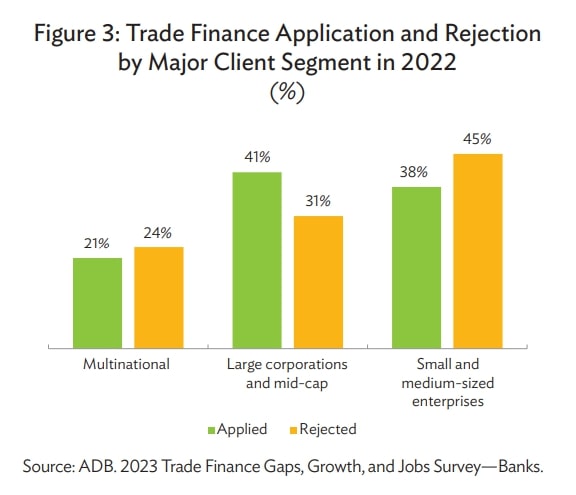

4 – SMEs remain at the forefront of the challenges

This year’s survey again emphasises the challenges faced by SMEs in accessing trade finance. SMEs are often more vulnerable to economic shocks, making access to trade finance even more critical for this segment.

ADB recommends enhancing trade financing capacity through SME-targeted credit processes, a crucial step for economic recovery. It also calls for increasing trade finance capacity through deep-tier supply chain finance and attracting new capital, both of which are expected to benefit smaller firms.

Michelle Knowles, Managing Director, Head of Trade and Working Capital Product (Pan Africa) at Absa told TFG, “This risk of an increasing trade finance gap was anticipated on the back of a multitude of risks that emerged, the pandemic, the macroeconomic and the current geopolitical environment.

Unfortunately, those that suffer the most are SMEs, the backbone of emerging market economies and those hardest hits are often women and youth-owned businesses.

Digitization will be key to help increase access to much-needed funding by reducing inefficiencies and associated costs. However, there are systemic issues that will require collaboration across the trade ecosystem to increase the availability of trade finance this includes enabling regulations, interoperability of platforms and in particular access to the hard currency liquidity to address the trade finance gap.”

5 – A call to action for policymakers

The report concludes with a set of actionable recommendations that can serve as a roadmap for policymakers and industry stakeholders, underlining the urgency of the situation.

The five recommendations are:

- Create additional capacity for trade financing.

- Support and advocate for the adoption and use of innovative financing that adds to net capacity, while appropriately targeting those most in need of trade-related financing.

- Leverage transformative developments such as sustainability and ESG to drive financing for SMEs and others in need of greater liquidity.

- Advance the global agenda around digitalisation of trade and trade financing.

- Continue to leverage trade financing as an effective and proven crisis response mechanism, addressing unmet demand in crises or in recovery phases.

Advancing change across such a diverse and wide-ranging industry requires a multi-stakeholder approach involving governments, financial institutions, and trade bodies to address these challenges effectively.

While banks are keen to support sustainable financing, they are often impeded by regulatory challenges and the absence of a unified framework. While the ultimate implementation of enabling regulation is beyond their realm of control, banks can be more proactive in driving the conversation forward and helping to shape these regulations.

Tomasch Kubiak, Policy Manager, ICC told TFG, “ICC is pleased to have facilitated the contribution of member-banks data to the ADB survey and to gain insights on the intricate elements widening the trade finance gap. Despite this, the ADB survey echoes existing insights from the ICC Trade Register, underscoring that trade finance remains a low-risk asset class.

The challenges identified in the survey are at the heart of our efforts. Digitalization, ESG and climate related requirements, knowledge of trade finance products and rules and KYC compliance matters are the highest points on our agenda. Through the ICC Digital Standards Initiative, standard-setting and advocacy on behalf of banks, corporations and small businesses, ICC is proactively addressing many of these concerns.

On the topic of sustainability, the ICC Sustainable Trade Finance Standards are currently being piloted in the textiles sector and will soon expand to the automobiles and agriculture sectors. The development of common use assessment frameworks for trade finance transactions is essential to clarify and inform the actions needed to reduce the trade finance gap.”

The 2023 ADB report serves as a comprehensive guide to understanding the evolving landscape of global trade finance.

It has been authored by Steven Beck, head of trade & supply chain finance at Asian Development Bank.

As the gap widens, these key takeaways offer a framework for stakeholders committed to bridging this growing chasm.

The report identifies the challenges and provides actionable recommendations, making it an indispensable resource for anyone involved in trade finance.