2021 opens in the middle of the greatest crisis of our lifetimes. The healthcare response to the pandemic defined 2020. The economic response to its lasting damage will define 2021.

Risk is all around us, and TXF CPRI revealed what could be in stock for the trade, commodity finance and export community at their flagship virtual event: CPRI 2021. As proud partners of the event, TFG reports on the key potential risks identified by the community.

Hosted via TXF’s Kujenga, a TXF’s custom-built platform with all the bells and whistles, this future looking conference provided all sorts of CPRI insights into what 2021 had in store.

Central to the discussion was geopolitical risk. Samuel Wilkin, Director of Political Risk Analytics at Willis Towers Watson and Charles Hecker, a Partner at Control Risks, gave us the full story on what this meant for supply chain finance and commodities in 2021.

The following is based on the panel session ‘Control Risks’ Geopolitical Keynotes for 2021’.

1. Long Covid and fragile global value chains

2021 will be a year of uneven vaccine rollouts and uneven recovery.

“There is no escaping that the pandemic will be the number one driver of risk around the world, short and long term,” says Hecker.

In the aftermath of 2008, only 20% of countries worldwide entered a recession, with economies like China and India still growing. By comparison, 2020 saw 90% of the world’s economies go into recession. The fallout of which has still not been properly realised due to unprecedented bailouts.

“If 2021 does not mark the end of the pandemic, it will be the year that determines what is left when the worst is over,” says Hecker.

He predicts a slow, fragmented exit from the COVID crisis, determined by access to vaccinations in a case of “have and have not countries”.

COVAX, which 92 countries are dependent on for their supply of vaccines, have said they can only supply 20% of their member states’ populations. Which one in five people have access to these doses will be up to them, and will be critical in the speed of their recovery.

Both Hecker and Wilkins are skeptical that any further attempts at track and trace programmes will be successful. Low levels of trust in governments and tech firms across Western countries prevent their effectiveness, with all hopes of suppression now being placed on vaccines.

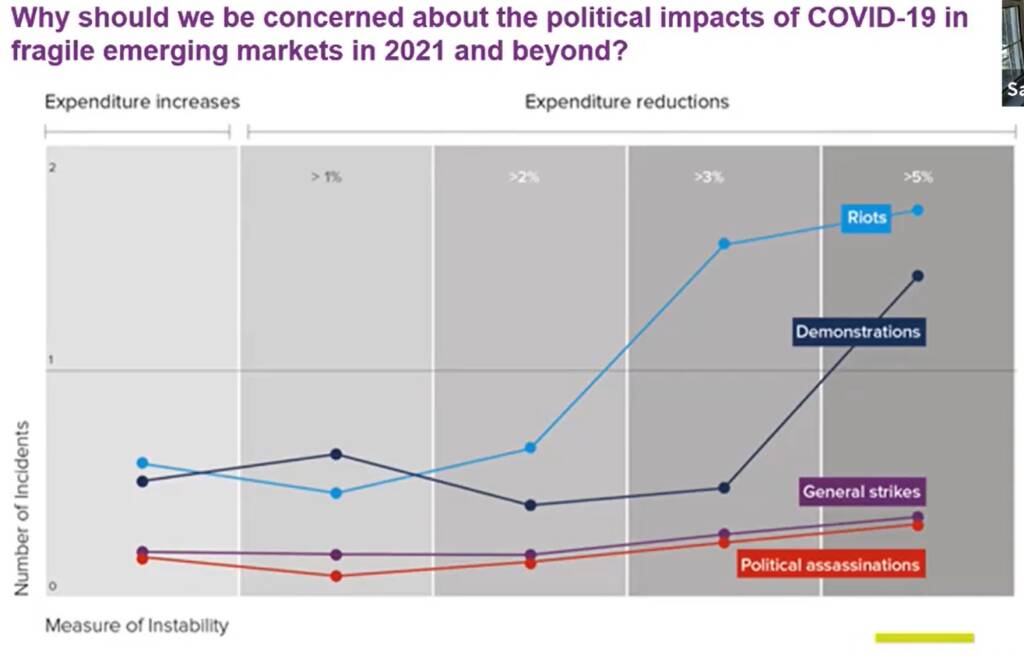

For the first time, countries with historically hard budgets have also had to spend on bailout programmes. With this inevitably having to be paid back, predicted expenditure reductions will lead to social unrest in the form of riots, demonstrations, and general strikes.

2. No stopping US- China tensions

The big geopolitical shock from the fallout of the pandemic was the deterioration of the relationship between China and the West.

“It got ugly fast,” claims Wilkin. “In Europe, China made this ill-judged intervention in Italy, trying to bail [them] out with medical supplies when they were first hit, [while] Italy was feeling abandoned by the rest of Europe. Russia was doing the same thing, trying to sow European disunity by association. Europe really turned on China at that point.”

With a new administration in the White House likely to bring with it significantly less anti-China rhetoric, 2021 will see the relationship shift into a period of “stabilisation without normalisation”.

“Companies won’t have to wake up and check Twitter to see what’s happening between the US and China,” says Hecker. “The heat will come out, the emotion will come out…but there will be broad continuity on sanctions, the same thing with export control. You [can] add the element of human rights to the relationship, and that is a dripping red flag in front of Beijing.”

“If there is a momentary reset in the relationship between Biden and Xi Jinping, take this moment for companies to roll out their strategies and get their heads around it.”

“It’s going to be an intimate relationship, one where you’re in love,…but still can’t stop hurting each other,” adds Wilkin. “As they lash at each other, these two lovers [will] lash out at companies, because it’s more ambiguous and it doesn’t invite retaliation.”

3. Going green is not a fad

National lockdowns caused factories to cease production and left highways empty across the globe. For the first time in recent memory, residents could see blue skies in Delhi, views of mountains in Los Angeles, but at a devastating cost to the economy.

Expect much more accountability on green initiatives on the back of this, says Hecker, as the agendas of Extinction Rebellion and private equity investors briefly align.

“We have companies and countries tripping over each other to issue these carbon neutral statements and green investment plans,” he says.

“Asset managers are going to comb through their portfolios, and say: ‘which of our companies understand the impact of climate change on them and the impact that they have on the environment’…The same thing with listing agencies, the same thing with governments.”

With the easing of restrictions, expect a return to the social action that came to dominate 2019.

“As soon as people can gather on the street again…there’s absolutely no turning back from an incredibly targeted and sophisticated attack from the activist community,” he adds.

4. The arms race between cyber crime and digitalisation to continue

2020 saw companies embrace cyber at hyperspeed, leaving a litany of holes in their protective measures along the way. The new equipment was not the issue, it was the safeguarding and usage policies surrounding its use, Hecker explains.

“Everytime a company stumbles on tech implementation at breakneck pace, cyber threat actors pounce. This can be state actors, non-state actors, cyber criminals, cyber activists or cyber terrorists. You name it – they’re waiting.”

“We rushed into the cyber world and did not look where the vulnerabilities were,” Wilkin adds.

Cyber also impacted social justice and community action in 2020. Black Lives Matter, the assault on the US capital and the running up of GameStop stock all had common themes: collective action and political communication.

“A demonstration was once a bunch of angry people going on a walk, and now, every demonstration is a potential flashmob. Fundamentally, these technologies empowered the many at the expense of the few, including now, on Wall Street.”

5. Be careful not to miss the rebound

While forecasters are hoping for a responsibly sharp economic rebound in the second half of 2021, risk will ultimately come down to how companies adjust to any sort of “new normal”.

“There are a lot of companies that are back in crisis management mode, after that mini-recovery we had in the summer,” Hecker explains.

“To catch this rebound when it comes, [they] have to be able to do two things at once. Take care of the tactical management, but also keen an eye on strategy and the future. This sounds like a no brainer, but it’s incredibly hard to do.”

“The pandemic was longer, deeper and more severe than anyone ever thought… A lot of companies put all hands on deck to steady the ship, and sparing energy, bandwidth, and people to think about the next year, five years or ten years became very difficult. The risk there is we lose sight”.

Buckle up – it’s a bumpy ride ahead

TXF CPRI wasn’t the only event that caught us clinging to our seats. For sure, 2021 will bring about further chaos, uncertainty and volatility, but there were many takehomes for the trade, commodity and export community.