The latest technology has significantly transformed the operations and data handling processes involved in trade finance. TFG spoke to Herbert Broenes about the digitalization of credit risk management.

Credit Risk Management and Trade Finance

So, what about the credit processes and decision making tools available in trade finance?

Solutions which are fast and cheap are important for markets. Smaller, single credit decisions are generally easier to make, and the market offers tools which are able to make those decisions for smaller companies. However, for many international debtors operating across different jurisdictions looking for a larger debt product, automation isn’t straight forward.

If we even get a solution to automatically evaluate trade risk, even at larger transaction sizes, the financial community would be able to handle and monitor the risk of financing trade assets, even for larger floated companies. However, this takes time, and here are the complications.

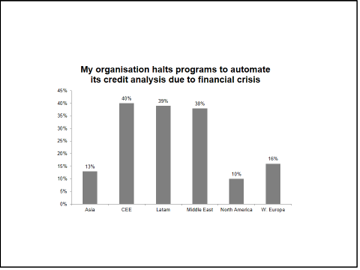

Figure 1: Percentage of organizations that utilized automated credit analysis

Before we can come to a solution on decision making in credit risk, there are a number of issues we need to address:

Credit Evaluation Process

Firstly, the credit evaluation process can take into consideration many points, first and foremost, the firm’s equity position, profitability, assets owned, and the legal framework of the deal; but there are other hard and soft factors. There can be many criteria for evaluating credit risk, all can seem very different from each other.

In trade finance there are some additional requirements to consider. The accounting rules in countries are still very different, the requirement for a credit may vary by region and the legislation and legal landscape is varied. Furthermore, the credit evaluation process today is still largely based on the decision of a human (a credit analyst) They decide on giving credit based on prior experience, knowledge of the market / product and often gut feeling about the cost of credit and credit limit. This can be done through either rule books, automatic credit scoring, or a combination of both.

Information Provided

The credit information which is requested and provided by parties, varies for the different trade finance requests. Also with trade finance, there is no central repository for all global credit finance transactions, and there’s is certainly no online credit information provider. To overcome this, trade finance can also be insured by an international credit insurer. International banks have two instruments to counter this: inhouse information on the trade / transaction, or through the issuance of a confirming letter of credit, where at least two banks are involved. All existing solutions involve cost and often time, which eats margins, erodes consumer trust and can be painful for all parties.

Solutions:

If we compare credit evaluation with other businesses, they have the same problems, and the solution is a standardisation of data so that we can compare, teach, learn and then price a product based on certain factors.

Let us take two examples: Firstly in medicine: Students are trained globally in a similar way, such as how to treat an illness. Students learn that in 95 percent of situations, a standard solution is the best option for that patient, however, in certain cases, a bespoke solution or treatment is necessary. In 2002, US Professor Fitzgerald wrote in his standard finance book for students: “A trained financial analyst should have his tools and knowledge to test the health of a firm like a medicine doctor tests the health of a patient”.

The second comparison can be seen in the handling of financial options with the Black Scholes method. The method was original only for heavily traded assets but today you can get options prices for stocks, fixed assets, currency and many kinds of commodities. In all cases the importance of the remaining time and the meaning of the volatility on the price is similar, even when the future outlook can be quite different.

Where Black Scholes is used in option prices, and doctors work based on standards, there are already models in the credit market. However, the standardisation of the overall credit market for businesses is lacking, which inhibits us from comparing apples with apples.

To bring the market closer to some form of standardisation, we must find the most important criteria in our businesses and then overlay rules which can govern credit risk. This is a critical step if we want to make trade finance and receivables a more investable asset class, where we can then create portfolios of receivables which can be anonymised, bring liquidity and further investment into the market and new participants. Information can include defaults / loans for bad credit, payments information, turnover, and current debt portfolio.

Table 1: Example of a method to illustrate and evaluate the credit risk of a portfolio

| Risk class | No risk | Low risk | Normal risk | High risk | Unacceptable

Risk |

| Average default rate | 0,00% | 0,25% | 0,75% | 1,25% | 3% |

| mEuro volume | 500 | 1,000 | 800 | 600 | 200 |

| mEuro securities | 0 | 200 | 400 | 200 | 100 |

| mEuro risk volume | 500 | 800 | 400 | 400 | 100 |

| mEuro default expectations | 0 | 2 | 3 | 5 | 3 |

My proposal concerning the model is to take only figures and ratios, that everybody can calculate and check. That means soft data like the evaluating of the management or the customer relation management cannot be taken. Furthermore, criteria that are not only linked to the non-payments prediction, like late payments, should be excluded as well. Some of the criteria that could be included here are:

- The turnover per year

- Home country of the debtor

- Years in business

- Equity ratio

- Nominal equity

Profitability figures and calculations however are hard to come by, especially because definitions are different so this isn’t as useful when doing a deal

Furthermore, in credit management the data is not always in depth enough and there are many variables, so it’s difficult to do a calculation score or create a model using raw company results unless the parameters fall within broader criteria.

The analytic credit database of the European Central bank (ANA requirements), which starts in September 2018 to control better the banks, uses some of the criteria as well. Let’s us the one, who build something special for everybody in trade finance and create the Dow Jones Index for Trade receivables. When we can realize it, trade finance will fast reach lower credit handling costs and more online credit offers. The total volume will be much higher than today, partially due to new products.