HO CHI MINH CITY, Vietnam, 11th June. Deepesh Patel, Editorial Director of TFG, spoke today on the Evolution of Receivables Finance at FCI’s 51st Annual Meeting held in Vietnam. Speaking on a panel chaired by Lionel Taylor, Trade Advisory Network, alongside Editorial Directors of BCR Publishing and Business Money, the panel gave an observer view on the evolution of factoring in Southeast Asia.

Speakers (Left to Right): Deepesh Patel (TFG), Bob Lefroy (Business Money), Michael Bickers (BCR Publishing)

The global volume of trade receivables stands at approximately $12tn, with factoring accounting for nearly 20% of this. Last month FCI released it’s 2018 global factoring volumes. Despite Europe claiming the lion’s share of global factoring volumes, Asia Pacific came out clear second, with nearly $700bn USD of factoring volumes; over a quarter of global volumes coming out of that region.

This article explores why technology is leading sweeping changes in South Asia, Southeast Asia and China’s factoring scene, the key drivers, and some of the key initiatives coming out of this market.

Figure 1: Total Global Factoring Volume as % of Total Global Volume, incl. Breakdown by factoring type. Sources: FCI, World Bank, AFSA

The factoring industry has seen a 4.4% CAGR since 2012, but whilst European markets have seen stable steady growth in last year, considerable growth has been experienced in South East Asia: Malaysia (170%), Korea (96%) and Vietnam (57%).

At Trade Finance Global, we have the pleasure of speaking to a number of corporates, bank and non-bank financial institutions (NBFI) and technology providers within the receivables space, and our view is that due to the current macroeconomic landscape in South-East Asia, the geopolitical situation in China, advances in technology, and a liquidity gap between developing and more established markets, the factoring landscape is undergoing significant change, and it will come from South East Asia.

Backdrop: Financial exclusion and a significant addressable market

Most people and most small businesses in emerging markets and developing economies (EMDEs) are excluded from the formal financial system. At a human level, 59% of South Asia’s adult population, that is, 642 million people, are excluded from the financial ecosystem.

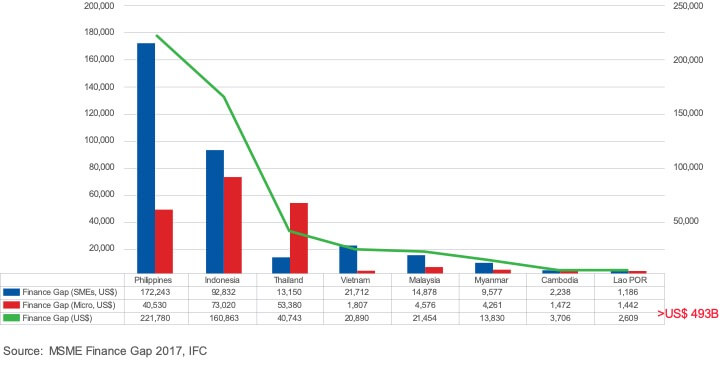

Both in credit and debt markets, SMEs across emerging markets cannot access the finance they need to grow, constantly reporting it as an obstacle to growth. Around half of SMEs are unserved or underserved in Southeast Asia, representing, a $493 USD credit gap.

Financial exclusion presents opportunities for fintechs, liquidity providers and entrepreneurs, not just in factoring, but in insurance, investment management, capital raising and payments.

These macroeconomic factors play a significant role in why we’ve seen extraordinary development in the trade receivables and factoring market in the past decade in Asia.

The Enablers

An outside-in view of the Asian market indicates 5 key enablers which make a tasty recipe for cutting edge technological innovations in factoring platforms, both for banks and factors.

- Market Opportunity. Asia’s Credit Gap is significant and is seeing the growth of trade-related operations and general development within these economies.

- Geopolitical Environment. The case for the growth of both domestic and also intra-regional factoring is significant, given opportunities such as the Belt and Road Initiative (BRI), a slowdown in US-China trade, and the demand for developing and emerging economies to provide goods to the larger Asian economies (Singapore, China, India and Bangladesh) continues to grow

- Regulation, sandboxes and scrutiny (P2P). Regulation within financial services in Asia is a double-edged sword. On one hand, central banks and regulators around the region have established ‘sandboxes’ designed to allow fintech players to test their services under relaxed regulations. On the other, digital financial services have come under the scrutiny of the regulator. For example, in late 2018 Indonesia’s OJK blocked websites and sent warnings to many of the peer-to-peer (P2P) lenders operating in the country in response to complaints about lending practices.

- Advances in technology. Receivables finance is a great candidate for many ‘enabling technologies’, including digital-based platforms and signposting services, big data and AI, and distributed ledger technology.

- The Liquidity Gap, and New Distribution Models. South East Asian countries have a great potential to grow in factoring since the level of credit provided to the financial sector is not sufficient for the robust markets. There is a big opportunity to bring together emerging markets with low factoring volume and the lack of sources of financing, and developed markets given their excessive investment capital.

We explore what this evolution means for the factoring industry, and why Asia Pacific is poised for sweeping changes in commercial finance.

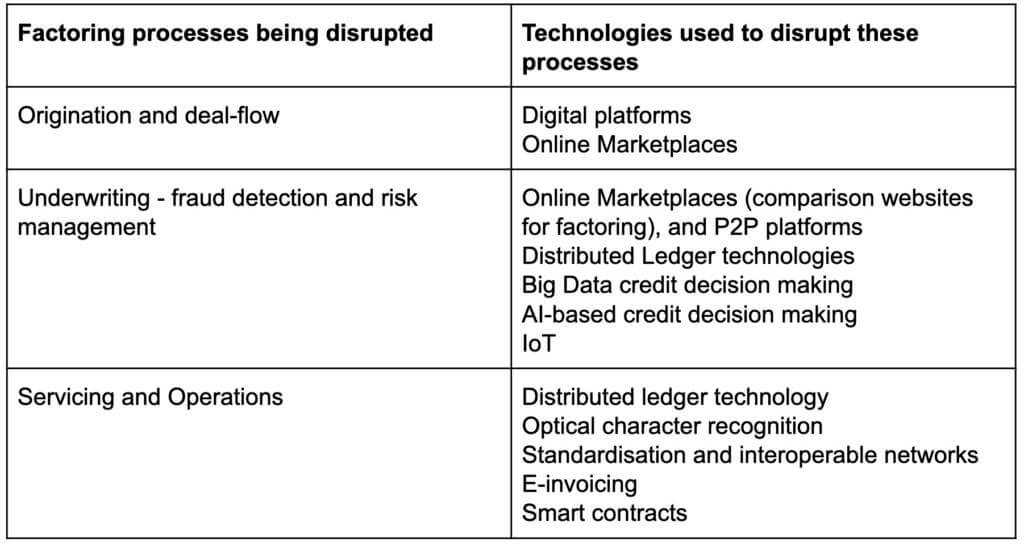

Within the factoring space, technological innovations could help digitalise and benefit three core processes within the sector, using various technologies:

So what’s actually happening?

Receivables fintech bears many opportunities for factors, providing new business models and digital transformation are considered by liquidity providers and end-customers.

There are huge innovations in the factoring space coming out of Asia, here are a few important case studies and notable fintechs:

Hong Kong

Qupital – Invoice finance for SMEs in Greater China. Branded Hong Kong’s largest platform for SME receivables finance, Qupital has raised $17m from Alibaba amongst others. To date, it’s financed around 8k trades, $250m USD volume.

FundPark – FundPark is bringing purchase order and invoice finance for SMEs in Hong Kong.

Velotrade – Velotrade are a factoring platform allowing businesses to sell their trade receivables (up to $500,000 USD at a time) to investors. Based out of Hong Kong, Velotrade are also gaining significant traction in China, Taiwan, Thailand and Vietnam.

WeLab – WeLab is a technology-based company using the brands WeLend (lending platform) and WeLab (virtual bank), as well as big unstructured mobile data to lend to consumers and growing companies.

Crowdo – Crowdo are a Hong Kong, Singapore and Indonesia based peer-to-peer debt and equity provider for businesses, whose investors are primarily the public.

Malaysia

PitchIN – PitchIN helps projects and businesses get funded through both a rewards-based and equity finance model using peer to peer crowdfunding. Its rewards-based crowdfunding platform is one of the most successful in South East Asia.

Singapore

CoAssets – A Singapore based lending platform, listed on the Australian Securities Exchange, CoAssets is a peer to peer based platform for projects and companies. Investors range from entry-level retail investors to high-net-worth individuals and institutions wanting to grow shareholder value through prudent capital enhancement.

Acudeen – Acudeen is an online platform for receivables discounting. Acudeen’s technology allows businesses to sell their invoices to their network of retail investors.

Invoice Interchange – Invoice Interchange allows Singapore based businesses to sell invoices from large corporates, integrated with Xero Cloud, funded by peer-to-peer private and institutional investors.

FundedHere – A regulated Singapore based equity and lending-based crowdfunding platform

A note on India

As mentioned earlier, regulation and disruptive intervention that is led by central governments / the state has been an enabler for large-scale disruption in South and Southeast Asia. Although not in South or Southeast Asia, it would be remiss of us to not discuss a fairly revolutionary move, led by The Reserve Bank of India (RBI), which back in April, licensed the three largest factoring platforms in India to provide a more efficient way of preventing financial fraud and double invoicing problems, by using hyperledger, a blockchain based solution to enhance the control over duplicity of transactions. These platforms are RXIL, A.TReDS, and M1xchange, powered by MonetaGo.

What are the challenges?

Receivables finance and factoring continues to grow across Asia, as corporate debt grows, and inter-regional economic activity also grows. However, there still lie inherent challenges:

- Adoption of digital contracts remains slow. Whilst recognised in some markets, others, such as Germany, do not recognise fully digitalised contracts without a written agreement. A number of initiatives are being led at a local level, supported by intergovernmental trade bodies such as the ICC, who are working on the implementation of digital signatures across local governments (UNCITRAL), but there is still much progress to be made.

- Business models need to be aligned with the objectives of a number of digital initiatives in the factoring space. Banks continue to invest heavily in networks and consortia, in attempts to rewire receivables finance. However, demonstrable proof-of-concept and live transactions on any of the platforms have not yet surfaced, and questions around profitability and ROI are arising.

As Marc Auboin from World Trade Organisation said: “A 10% increase in factoring would result in 1 % in additional SME trade”, so attempts to disrupt the three core processes within factoring would help reduce the costs of origination, facilitate the underwriting process, and potentially reduce servicing and operational costs within receivables finance.

The author would like to thank Derek Lee, Ooway, for input and recommendations here