On Wednesday, Chancellor of the Exchequer, Rishi Sunak delivered what could be the most important budget in a generation. A year on from the UK’s first lockdown, and the pandemic continues on but there is an end in sight – bringing some hope for all, including the UK’s public finances.

UK national debt exceeded that of GDP as of 2020, and the cost of this debt is an area for concern for many. The UK economy itself has a much more optimistic outlook for the remainder of 2021 going into 2022 and beyond, provided the covid-19 situation allows the UK to successfully complete PM Boris Johnson’s Roadmap.

In his budget announcement, the Chancellor explained the economy would recover much faster than previously estimated, returning to pre-pandemic levels by the middle of next year. The Office for Budget Responsibility (OBR) has announced expected growth of 4% over 2021, increasing to 7.3% over 2022. Further to this, national unemployment will peak at 6.5%, rather than the 11.9% previously forecast.

With UK businesses facing continued uncertainty following a turbulent year, and the UK’s finances reaching record debt levels, this budget carried enormous importance. It was a comprehensive budget, with announcements covering various taxes, further covid-19 response, numerous investment projects/ competitions and the introduction of 8 new freeports. However, given the state of the UK’s public finances, was it enough to support the UK economy through the pandemic recovery, and what are the risks of such large sums being borrowed?

State of play – UK Finance

As of December 2019, the UK Government had spent £280 billion solely on Covid-19 response. That same month, the UK borrowed £34.1 billion – the third highest monthly amount since records began. In 2021, the UK is expected to borrow a peacetime record £355 billion. The enormous amounts spent and pledged by the government have resulted in the overall national debt level increasing to £2.13 trillion, passing the £2 trillion mark in August of 2020.

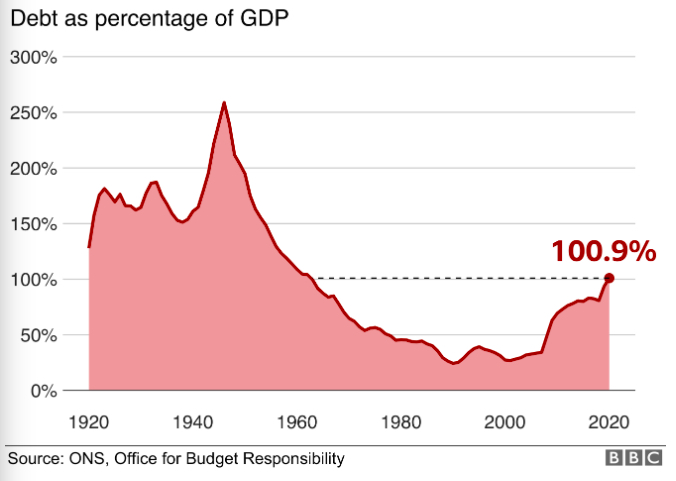

In 2019, UK GDP totalled £2.05 trillion. With the devastating effects of Covid-19 and resulting lockdowns, GDP over 2020 fell by as much as 9%. Pair this fall with the substantial increases in national borrowing and it resulted in the UK’s national debt being greater than GDP for the first time since the second world war.

The cost of said borrowing has also been a controversial topic in the lead up to this budget. The history of the UK’s public finance and indebtedness is interesting. The UK has seen debt not only exceed GDP, but more than double it as occurred in 1946 where UK national debt equalled 252% of GDP.

Firstly, it is important to establish how the government has raised such large sums of money. According to Parliament Commons Library, over 85% of the Government’s total debt has been raised by selling gilts and bills. A gilt is a monetary loan to the government for a specified amount of time (known as the gilt maturity), and in return receive an interest payment (coupon payment) every six months until the gilt maturity date. Upon reaching the maturity date, the government will also repay the original amount to the holder of the gilt at that point in time.

There is also a treasury bill, which are much more short-term in that the maturity date is less than a year. Both treasury bills and gilts are auctioned by the Debt Management Office (DMO) – the government’s debt management agency.

To understand the concern around the cost of UK borrowing, it is also important to understand how and why interest rates are used. The most common tool of monetary policy, the interest rate is managed by the Bank of England, and is used to control the level of spending/ investment in an economy. In its most simple terms, if inflation is increasing, then an increase in the interest rate would make saving/ investing more attractive, taking capital away from the consumption that was driving inflation.

This works both ways – if inflation is below target and the economy is not growing at a desired rate, by decreasing the interest rate you are making spending/ borrowing more attractive, encouraging economic activity and growth.

From a government’s perspective however, the knock-on effects of interest rate manipulation have a much more concentrated impact. When people refer to the ‘cost’ of the UK debt, they are referencing the interest the UK pays atop the original amount borrowed.

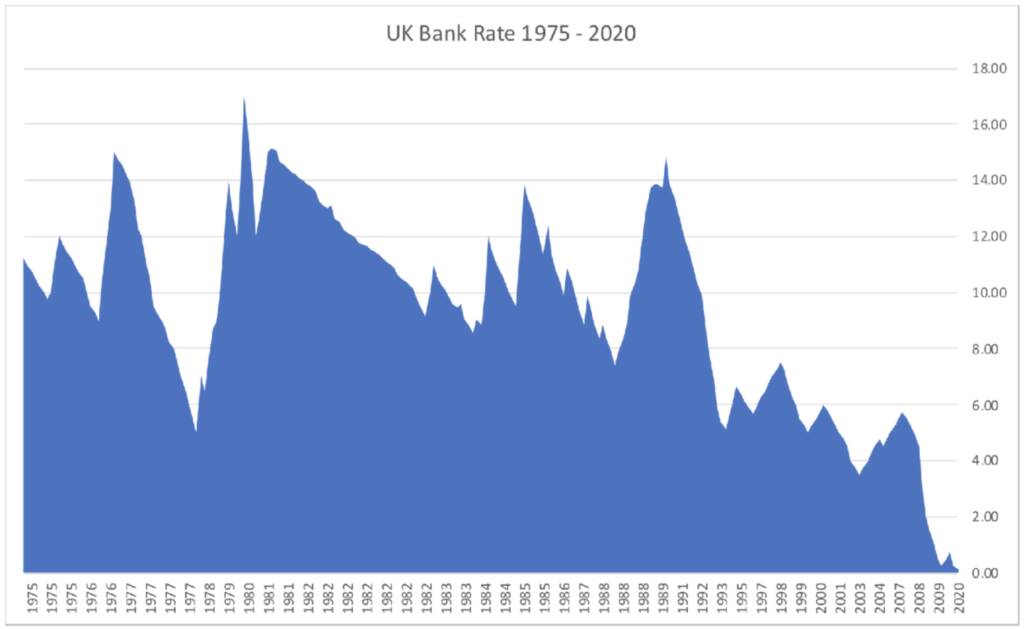

The Bank of England has become a significant holder of UK gilts as part of the quantitative easing programme introduced in 2008 in response to the financial crisis, which has continued in response to Covid-19. The Bank of England’s move to cut the bank rate to 0.1% in March of 2020, resulted in the interest payments the government paid on outstanding gilts decreasing, meaning it was cheaper for the government to continue to borrow sums. The issue is this works both ways, and when interest rates are increased, the rate of interest the government pays on said debt increases.

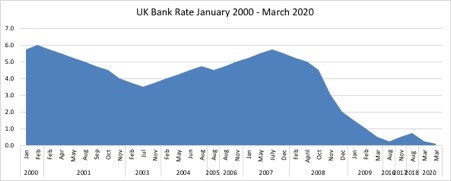

This is why the UK national debt is an area of concern. The UK has enjoyed comparatively cheap costs of borrowing over recent decades. Looking at data from the Bank of England, the UK’s Bank rate, currently at 0.1% have not only been reduced in the wake of the 2008 crash and 2020 covid-19, but have also followed a downward trend since the late 1980’s.

With the aforementioned OBR predictions of 4% growth this year and 7% next year comes a significant element of risk regarding inflation. As previously mentioned, the Bank of England uses the rate changes to manipulate the level of spending in the economy. The low rates seen since the financial crisis of 2008 have supported the economic growth, but some argue have overstayed their welcome.

The ONS estimated there were around 700,000 fewer people employed in 2021 than before the pandemic. This reduction in employment along with reduced demand from lockdowns have meant ultra-low interest rates have been necessary to stimulate economic activity. With the projected growth of 2021 and 2022, and the return of jobs in the UK inflation is expected to increase from the <1% levels seen in 2020.

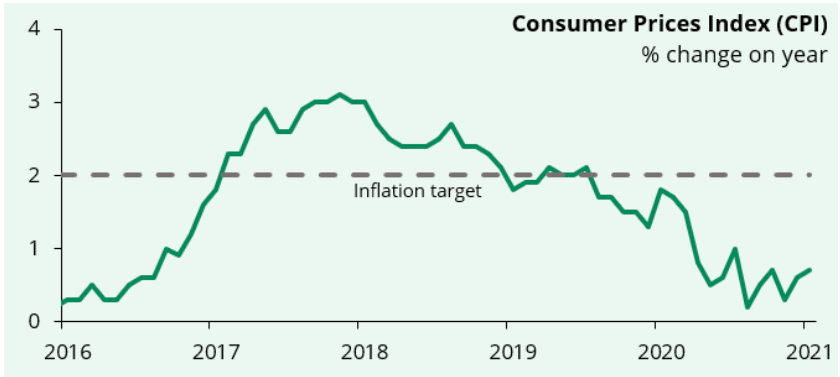

The above image from the UK Parliament library shows that over 2020 inflation was well below the Bank of England’s 2% target, but is showing signs of increasing. If inflation is to carry on, and indeed become a concern for the Monetary Policy Committee and Bank of England, interest rate increases could be a way for them to control the spending level in the economy in an attempt to curb inflation. This would however translate to higher interest payments on gilts, meaning the UK cost of borrowing would increase.

Trade and Freeports

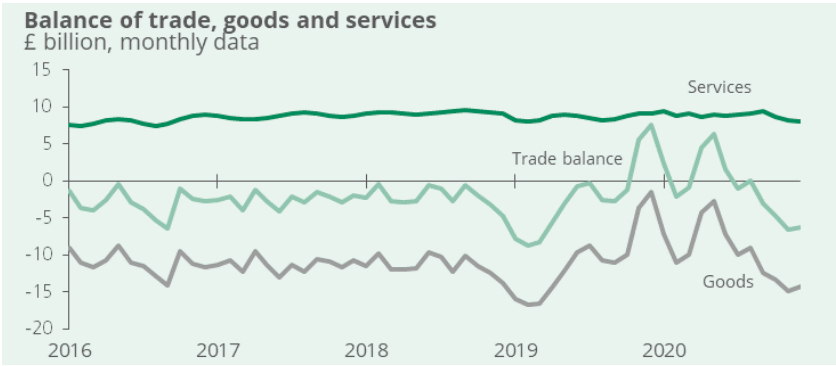

The economic slump of 2020 had clear impacts on UK imports and Exports, as supply chains around the world suffered through the pandemic. UK service trade had a turbulent year, with 2020 seeing a -21.8% decrease in the trade of services. Goods trade in the UK followed suit and decreased -15.7% over the year.

The UK has operated a goods trade deficit since 1998, and 2020 saw said deficit deepen follow steady decreases in 2019.

In 2020, UK total trade fell -18% (from 2019) to £1,153 billion. Exports totalled £571.7 billion (down 17.1% from 2019), and imports totalled £581.3 billion (down 18.9% from 2019).

In his Budget announcement, the Chancellor announced the introduction of 8 new freeports. A freeport is a specified area in which trade is not subject to the usual taxation/ customs processes. The Institute for Government (IFG) states that businesses operating inside the designated areas can manufacture goods using imports, and export their produced goods without ever facing the full tariffs or customs procedures.

Freeports are designed to support businesses that import materials to then produce and export. If the goods were to leave the designated areas, they would then be subject to the usual tariffs/ customs protocol it would usually face.

The 8 new freeports will be located in East Midlands airport, Felixstowe & Harwich, Humber, Liverpool City region, Plymouth, Solent, Thames and Teesside.

Invest in the UK

This year’s spring budget saw specific focus on investment – some from the government themselves and others a sort of crowd-fund. Looking at the governments summary of the budget, in relation to investment support they have announced:

- £375 million UK Future Fund – used to invest in “highlight innovative companies such as those working in life sciences, quantum computing, or clean tech”.

- Help to Grow scheme – offers up to 130,000 companies across the UK a “digital and management boost”.

- Research and Development Tax relief.

- £150 million Community Ownership Fund – aimed at facilitating communities across the UK investing in businesses that “matter most to them” – pubs, theatres, shops etc.”

- ‘Super-deduction’ in companies tax bill by 25p for every £1 invested in new equipment.

This stimulation of UK investment is aimed at supporting UK business and UK trade on the whole. Chancellor Rishi Sunak announced that rates are to be kept at 19% for roughly 1.5 million small businesses with profits of less than £50,000, and also announced there will be no tax charged on sales of less than £500,000. However, the budget also brought a future increase of corporation tax for larger firms, as tax on company profits above £250,000 are to increase from 19% to 25% in 2023.

The main challenge of any budget is to balance fiscal measures along with outgoings – both existing and those being committed to. In a year expected to set a peacetime record for borrowing, following 2020’s figures the reduction in taxations will temporarily add to the UK’s concerning financial situation.

The challenge of this specific budget is ensuring that businesses are supported enough to fuel the growth and much-needed economic recovery, whilst successfully managing the public finances.

A greener UK?

Amidst the global pandemic, there still remains the global environmental crisis. The 2021 spring budget did see various measures to move the UK into a more environmentally friendly nation, but some have criticised it for not going far enough. Labour leader Sir Keir Starmer said the budget “stopped way short”.

Environmental measures announced in this budget include:

- £20million fund for UK competition to develop ‘floating offshore wind demonstrators and help support the government’s aim to generate enough electricity from offshore wind to power ever home by 2030”

- £68 million fund for UK competition to deliver long-duration energy storage prototypes, aiming to reduce the cost of storing excess low carbon energy.

- £15 billion of new ‘Green guilts’ to be issued over the coming year. Said guilts will allow investment in “critical projects to tackle climate change”, as well as providing infrastructure to create more environmentally friendly jobs.

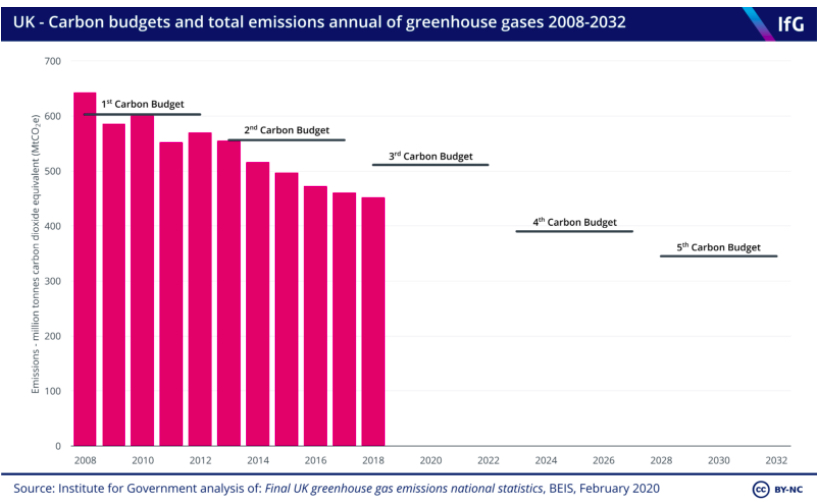

The UK introduced the Climate Change Act in 2008, which required the government set legal ‘carbon budgets’, with the aim to achieve net zero emissions by 2050. UK emissions have met said budgets each year since 2008, as we can see in the below image from the IFG.

High stakes ahead

The gravity of this budget was well understood by the Chancellor, and his budget announcement to the House was concluded with honesty on the challenges the UK public finances face now and over the coming years.

This budget was designed to provide sufficient stimulus to the UK economy for it to navigate the remainder of the year successfully, and reach the OBR’s expected 4% growth this year, and 7.5% growth next year. As the economy grows and businesses begin trading fully again, the governments income will increase with business and personal taxes increasing again. There will however remain a significant debt that must be repaid at some point. How this debt is managed will have significant impacts on the people and businesses of the UK.