“The rules-based multilateral trading system is the bedrock of economic globalization and free trade, and provides important safeguards for win-win outcomes” – WEF

In the midst of 2020, with nations battling the health crisis whilst attempting to balance the economic crisis also, the Presidential election has come at a particularly significant time. President-Elect Biden – once he assumes office – will inherit the US trading power, which over the last 4 years has solidified itself as a force to be reckoned with after its aggressive approach to trade.

The 2020 US Presidential election, although expected to be a particularly controversial event, has proved itself to be much more than that. At the time of writing it has been over a week since the official election date of 3rd November and the US is still yet to officially certify the election results.

Joe Biden has been announced as “President-Elect”, however Trump is refusing to enter into transitions with the elected administration, and the current President’s attorney general has authorized investigations into voter fraud, according to the NY Times. Furthermore, the current administration has most recently filed a law suit in the state of Michigan, requesting a federal court block the certification of their state election due to further allegations of voter fraud.

What’s more, is that “multiple [Trump] administration officials” have confirmed it is continuing to prepare a 2021 budget to present to congress in February, as reported by the Washington Post in their article “White House tells federal agencies to proceed with plans for Trump’s February budget in latest sign of election defiance”.

Once Biden does take office, what can the global trading economy expect from the US and more specifically, how would this compare against the last four years of the Trump administration?

4 Year hindsight – Trump’s Trade

The Trump administration held firm on their “America First” agenda. Looking back over the past 4 years, Trump’s unilateral approach global trade is quite clear – Rachel Brewster, Law Professor at Duke University wrote for the Yale Journey of International Law:

“The United States’ escalating trade war with China, its combative relationship with European trading partners, its forced renegotiation of the North American Free Trade Agreement (NAFTA), and its block on the appointment and re-appointment of Appellate Body members at the World Trade Organization (WTO) have all vaulted trade politics into the spotlight from its once quiet existence.”

The impact of this approach can be drawn upon from many areas. If we first look to the US’ balance of trade with China throughout Trump’s administration, we can see that overall, the deficit has reduced by -$1,708m (-$31,380.00m in Jan of 2017 vs. -$29,671.60m as of Sept. 2020).

3 scenarios

[Yellow] US raises 25% tariffs on Steel imports and 10% on Aluminium

[Green] China raises 25% tariffs on 128 US Products

[Red] Trump announces tariffs of 25% on roughly $50bn worth of goods

The above three points are believed to be the beginning “tit-for-tat” tariffs of the US-China Trade war. We can see that over the period between the first US tariffs on Steel and Aluminium, where the deficit sat at -$25,641m, and September of 2020, just prior to a “Phase 1” deal where the deficit then sat at -$29,671m, the trade deficit on US goods with China has actually increased by 15% (-$4,030). It’s also worth remembering that the period between the initial steel and aluminium tariffs and September 2020 we saw import tariffs between 10% and 25% on up to $300bn worth of goods. There is an argument that the US economy is worse off and suffered due to these tariffs. Because US tariffs not only increased prices for businesses in the US purchasing relevant products from China, but also because it lead to retaliatory tariffs from China, then harming exports to China (of which the US exported $106bn in 2019 according to the Office of the US Trade Representative).

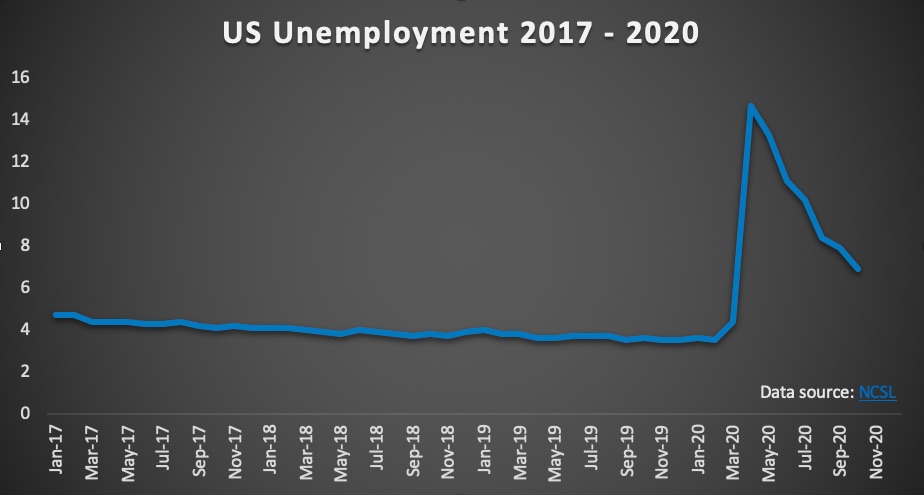

US Unemployment over the same period has held relatively stable throughout. In January 2018 US Unemployment sat at 4.7%, compared against 3.5% in January 2020. From this, it could be argued that the impact of the tit-for-tat tariffs did not harm the US economy in the ways as initially predicted.

Biden’s Take on Trade

Biden’s approach to trade is believed to be much more toward the cooperative, multinational side. According to Reuters, “Uncle Sam’s allies across the globe have high hopes for President-elect Joe Biden” referencing German Economy Minister, Peter Altmaier’s comments that Biden’s election win “augured a return to a stronger multilaterism”.

Throughout his campaign, Biden’s stance on global trade has been much more relaxed than that of Trump’s administration. That being said, the two do share fundamental beliefs that historic free trade arrangements have not benefitted the US, and that China is a problem that needs addressing.

Although Trump and Biden share these beliefs, their approach to addressing them differ greatly, and this is where other nations will look to benefit through the Biden victory. Previously, the Trump administration looked to use its weight in the global trading market to pull out of deals, jeopardise international trade body’s integrity alone, and also participate in focused, tit-for-tat tariff wars with other nations directly. Biden on the other hand, has thus far expressed intention to approach what he believes to be their issues relating to international trade in a collaborative way with other nations, and to use this to “build leverage”.

Biden however, did of course serve as Vice President to Obama, who’s impact on US and global trade over his 2 terms is not in complete contrast to the beliefs of Trump and Biden, but certainly does not align to the actions of the Trump administration. Over his 8 years in office, Obama “brought 24 trade enforcement cases to date to the World Trade Organization (WTO) – including 15 cases against China – and won each case that has been decided” (Cabinet Exit Memo – Ambassador Michael Froman).

President Obama was vocal about inequalities and concerns around whether other nations were “playing fair” in the global trading environment. The Obama-Biden administration ushered the TPP in 2016, in a bid to promote trade and jobs both domestically and abroad. This Obama administration was a cooperative nation on the global trading platform. Ambassador Michael From goes on to express how the administration “engaged with other countries – bilaterally, regionally, and multilaterally”.

“I have made rigorous trade enforcement a central pillar of U.S. trade policy, and we have moved aggressively to protect American workers and to improve labor laws and working conditions with trading partners across the globe.” – USTR

Podcast: The Transatlantic Love Triangle

State of Play – 2020 GDP

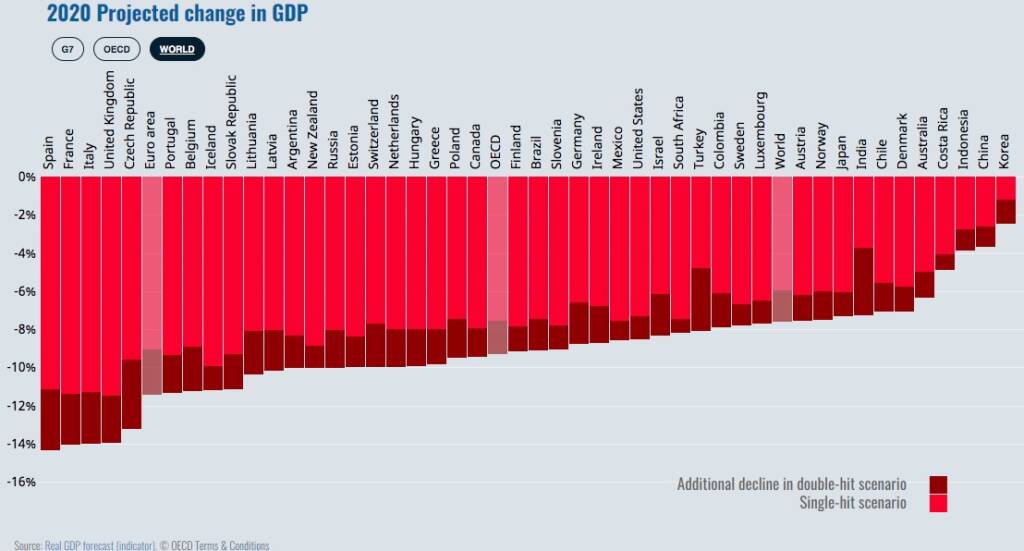

A turbulent time for the world’s largest economy, atop an already disruptive global pandemic. With the global health crisis that is Covid-19, 2020 has seen reductions in GDP not seen in decades, and recessions that stand far above that of 2008. Over 2020, the OECD predicts declines as steep as -14% for Spain, the UK and France. The US is estimated to decline by as much as -8.5%. The euro area as a whole is forecasted to contract by -11.5%, whilst Asian and East Asian areas such as Indonesia, China and Korea are expected to contract by much less damaging figures (-3.9%, -3.7% and -2.5% respectively).

This year has witnessed extraordinary disruptions to international trade due to the impact the health crisis has directly had but more specifically the impact of methods of reducing the virus (lockdowns, international travel bans etc.).

Parts of China began to go into lockdown as early as January 23rd this year, greatly impacting supply chains around the world. In January China’s export growth turned negative, recording $188bn worth of Exports against 2019’s figure of $191bn. According to The Observatory of Economic Complexity (OEC) China’s export growth dropped to as low as -40.7% in February following the lockdown’s, illustrating the impact on exports for a nation as manufacturing-dense as China and adding context to the disruptions felt by businesses around the globe.

However, China and other Asian nations have since taken place as some of the least affected from COVID in GDP terms. Comparing the aforementioned contractions for Indonesia, China and Korea and comparing against the number of recorded cases of Coronavirus since it began, we can see China with 92k cases (0.006% of population), Korea has 28k cases (0.05% of population, though questions have been raised around this) and Indonesia with 452k cases (0.17% of population).

If we compare these figures with some of the heavier GDP impacted nations, such as Spain with a -14.4% GDP contraction (with 1.42m Covid cases which is 3% of their population), or France with a -14.1% contraction (with 1.9m Covid cases which is 2.8% of their population), we begin to see the correlation between the presence of Coronavirus in a nation against their population, and the level of pessimism included in the 2021 forecast.

2021 – A fork in the road

According to the World Trade Organization’s (WTO) recent press release, global trade is forecast to decline by -9.2% in 2020, significantly less severe than the -12.9% forecasted under the more optimistic scenario in April’s forecast. Interestingly however, 2021 growth projections (7.2%) are now much more pessimistic than the previous forecast (21.3%).

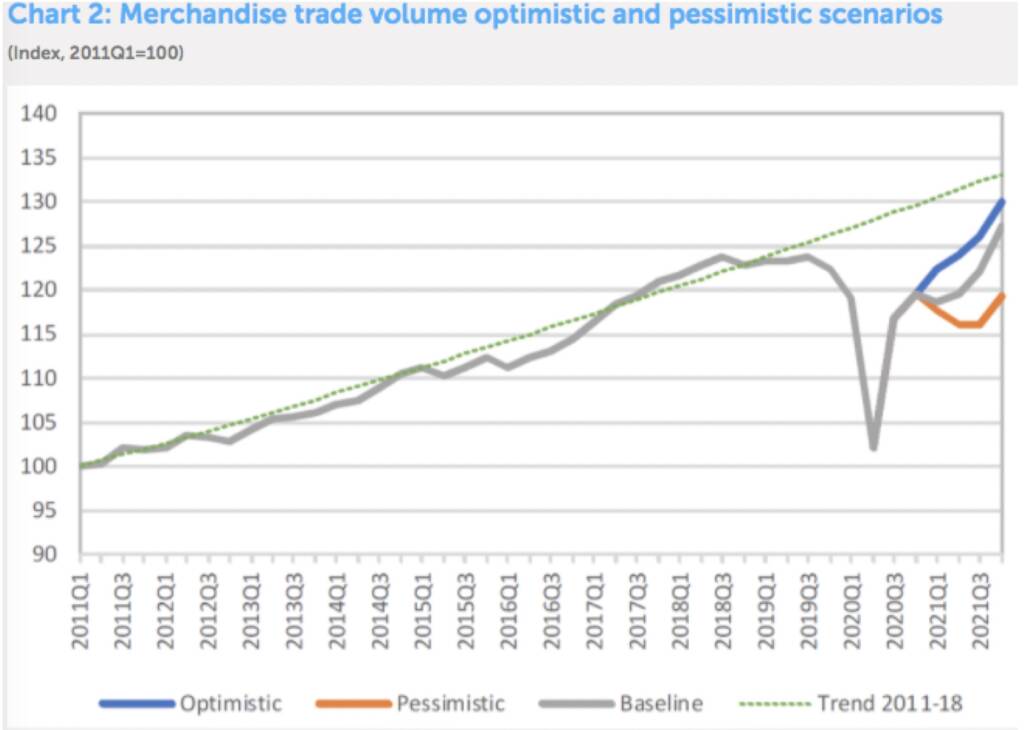

Below, the WTO have released a revised version of the scenario’s for global trade Covid-recovery:

We can first of all see the baseline which sees global merchandise trade end 2020 Q4 at an index score of 120, leading into Q1 2021 slightly below 120, and finally increasing to above 125 after Q3 2021.

We then have the Optimistic Scenario, in which global merchandise trade enters Q1 2021 at around 124 (3.33% increase on the baseline), increasing to 130 (8.3% increase on the baseline) after Q3 2021.

Following this is the pessimistic scenario, where global trading volumes fall from Q4 2020 score of 120 to 117 (-2.5% decrease on the baseline) in Q1 of 2021. Following this, trading volumes then decline slightly again in Q2 to 116 (-3.33% decrease on the baseline), where it remains until Q4 2021 with a score just below the baseline of 120.

President-Elect Joe Biden – what to expect

It goes without saying that the main driver behind global trade following either the optimistic or pessimistic scenario is Coronavirus and how well the global economy is handling it. But outside of Coronavirus, Biden’s role as President of the United States is bound to have a great impact on the world’s trading patterns of 2021 and beyond.

With Obama, we saw an administration be vocal and active about trading complaints, and with the Trump administration we saw vocality, activity and aggression with their approach to world trade. It is expected Biden will follow a path closer to that of Obama, but the trading landscape which Biden is inheriting is undeniably tense.

The key difference between President-Elect Joe Biden and President Trump, can be found in the differences between unilateralism and multilateralism, between cooperation and disassociation. As Biden himself said in a in his speech upon becoming President-Elect “I pledge to be a President who seeks not to divide, but to unify”.