")

Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn, PodChaser

Season 1, Episode 23

Host: Deepesh Patel, Editor, Trade Finance Global

Featuring: Charles Bryant, Secretary General – European E-invoicing Service Providers Association

Today TFG record live from the ITFA Annual Meeting in Budapest. The conference covered developments within areas of supply chain finance, credit risk insurance and ever more creative risk distribution techniques, as well as the rise of FinTech within the trade and open account environment. TFG heard from Mr Charles Bryant, the founder and Secretary-General of European E-invoicing Service Providers Association EESPA, discussing e-invoicing.

Deepesh Patel: I’m Deepesh Patel, Editor at Trade Finance Global.

Today, we’re broadcasting live from the ITFA Annual Meeting in Budapest. I have an excellent keynote speaker joining me today to discuss two major themes at the ITFA Budapest conference, Mr Charles Bryant, Secretary-General for the European E-invoicing Service Providers Association (EESPA). So Charles, in no more than 30 seconds, can you introduce yourself and tell us what you do at ESPA?

Charles Bryant: Well, thanks for that introduction. I’m actually a former banker in trade-related businesses. I then worked for service organisations in the industry like SWIFT, the European Payments Council, and one or two other associations, and then I became very conscious that e-invoicing is rapidly developing. So I worked with people to set up an association of about 70 service providers. I act as Secretary-General and organise activities amongst the group, which I will go into some detail later.

DP: Charles, from your perspective within the financial services and e-commerce sector, what have you seen over the last decade or so when it comes to improving processes, embracing technology and helping suppliers unlock liquidity in the supply chain?

CB: The last couple of decades have been characterised by the growth of networks, with the internet being the paradigm case. So it’s networking the creation of a networked world, both in the financial services area and in commerce and e-commerce. Secondly, we’re moving into the stage of serious digitisation. Some people use the word digitalisation, which is more comprehensive, perhaps regarding where you change your business model, but just digitising data – and then transmitting it across networks – is absolutely feasible now. It’s changing the way we live.

The Benefits and Problems with Electronic Invoicing

DP: Just going into a bit more detail, how is technology helping to close that gap? Can you talk to us about some of the E-invoicing projects that ESPA are leading on? Some of the success stories, why invoicing is hard to digitise, and the benefits from e-invoices?

CB: Well, electronic invoicing is a network play and a digitisation play. The benefits of it are massive, in terms of efficiency, generation and cost reduction, transparency, reduction of fraud and under-recovery of tax revenues. So there are huge benefits there.

The problem with it is invoicing itself, which creates some complexity. For example, the tax compliance that is essential, and the invoice is the last thing that happens before a payment gets made, so it has to be very secure and very clear before money changes hands. Some of the projects we work on connect platforms which provide services to both buyers and suppliers.

In many cases, the starting point of a marketplace like this is ‘three corner platforms’, where people invent a solution, develop a solution, and deploy a solution. There is a wish to onboard both the buyer and supplier and provide services for both: data capture, invoice creation, validation, secure transmission, receipt and integration into the IP system of the receiver. All of this can be orchestrated quite well across the three-corner model.

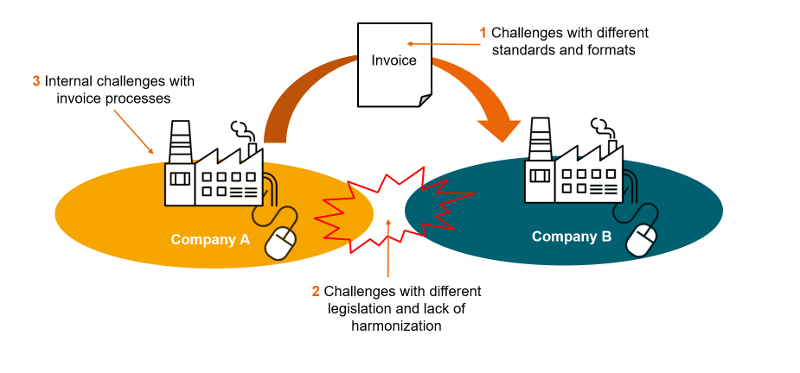

But as scale builds, you’re going to find the reality that not every supplier is on the same platform as their buyer or doesn’t want to be. So we have developed some successful models for interoperability, as we call it, whereby partners on different platforms can communicate with each other. For that, you need to develop standards, protocols and practices to make that happen.

European Commission on Digitisation of Invoicing

The other thing that’s been happening in the European Commission, is that the European institutions have been very supportive of this digitisation of invoicing – they see it as a catalyst for digitisation, especially in the B2B and B2G world. They don’t in the B2C world, because there are other channels, such as Facebook and other social media, that drive digitisation in that world. But in business, the invoice is a sort-of catalytic document, a fulcrum in the relations between two entities, which is an important process to automating the supply chain. So we’ve been very active in helping the European Commission and the standards body for years, to create a standard which everybody can adopt. Those are a couple of examples of things that we’ve been doing.

Invoice Model for Supply Chain Finance

DP: Thanks. Yes, we have talked about standardisation and interoperability being those catalysts for success quite a lot. Now, let’s move on to talk a bit about supply chain finance. Just a couple of weeks ago, we discussed the benefits of supply chain finances as a win-win-win for suppliers, corporate and buyers – is it really a win-win-win Charles?

CB: Supply Chain Finance is quite a complex area. I have become involved in that tangentially to my work in invoicing, although I do consider them as being very linked. I see supply chain automation as one side of a coin, with the other side being supply chain finance, so they are definitely joined. But supply chain finance is an amalgam of instruments and techniques that have developed in many different contexts – but now they are slowly coming together with digitisation to become easier to use and create solutions.

I have done some work on standard definitions in that area and that type of clarity is what the market needs, which is why I’m here actually – because I work closely with Sean Edwards and others who are in this area. In terms of the relationship between invoicing and supply chain finance, some of my members – but not all of them – are taking a close interest in whether the adjacent space of financing and maybe even payments represents an opportunity. I think they’re doing that in a collaborative manner, so I think there’s huge potential for us too. We want to join forces and create bridges between the community of FinTechs, banks and our members – we have 75 within EESPA and the number is growing.

It’s a globally representative number to see whether we can use our skills in networks and digitisation to provide services that the banks and FinTechs could benefit from. So we do see that as a win-win with the clients, especially in the case of an invoice model for supply chain finance; where you get an invoice that your buyer integrates into their system. They might then issue a promise to pay, an undertaking to pay, a response to pay, or an approved for payment message – something like that. Our members are able to package these receivables and have been discounted various models for that. We have millions and millions of invoices in digital form within our networks and I think there is an opportunity to sit down and figure out how to use that as a feedstock for supply chain finance amongst asset managers, banks and other FinTech organisations.

SCF in Europe: A Dream in the Making or a Giant on our Doorstep?

DP: Yes, that’s a theme we’re increasingly seeing at the IFTA conference. We’ve seen the ecosystem of FinTechs and where they’re playing – whether it is around big data and the mass collection of invoices etc. Moving back to your earlier point, we really liked the work you did with Sean on the standardisation of SCF definitions and the non-player-centric approach. I think it’s important to understand the different views, but also standardise those definitions in the market. So, moving on, is supply chain finance in Europe a dream in the making or a giant on our doorstep?

CB: I think the idea of a giant on our doorstep was referring to automating our e-invoicing supply chain. That’s a giant in the sense that if we can unlock all those invoices – which are evidence of receivables that can be financed – we have a great asset. But there is also a giant in the making, in terms of the supply chain finance itself, in all of its various aspects. All the different instruments: receivables, finance, factoring, payables, finance, distributed finance and finance – all these various techniques can be unlocked. When the European Commission get serious about an issue, things can happen, but time will tell.

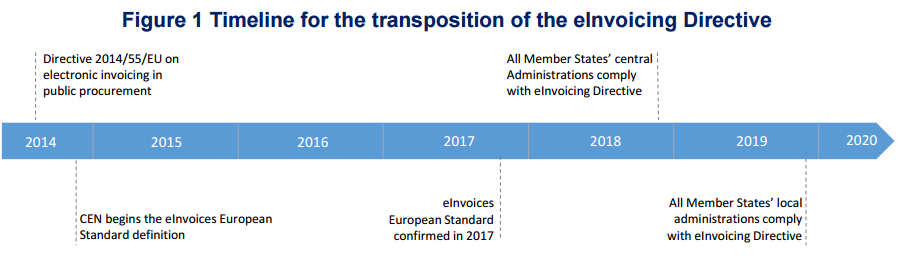

But European institutions and the European Central Bank floated the idea of a common payment system and that has since been achieved – I was involved in that some time ago. They’ve looked at invoicing and they brought in the harmonisation of the VAT directives that drive the invoicing compliance. They’ve also introduced a directive that makes it compulsory for all public bodies in Europe to be able to receive invoices, according to a standard. So, there is a study going on at the moment and I have a feeling that the Commission and the European institutions might think about whether there is an opportunity to create more of a single market or capital markets union associated with supply chain finance. There’s a lot of consultation going on, so let’s see whether some of the legal and other barriers could be lifted so that we can create a genuine single market for the services because they are complex at the moment with different legal regimes and different market practices. Time will tell.

DP: Thank you very much, Charles, and it’s good to have you here today at ITFA Budapest. We look forward to hearing some of the updates coming out from yourselves in the future.