In today’s economic landscape, there exists a substantial gap of approximately $2.5 trillion in trade finance, limiting businesses’ ability to flourish and capitalise on lucrative opportunities. The ramifications of inadequate support are significant, highlighting the importance of addressing the challenges faced by borrowers in accessing trade finance.

Several factors contribute to the impediments restricting borrowers’ access to trade finance.

Chief among these challenges is the lack of technical capacity among businesses to formulate and present compelling business plans and bankable proposals. The manner in which businesses approach banks is crucial, requiring careful consideration of various elements to enhance their chances of securing financing.

High-interest rates further compound the obstacles faced by borrowers. Banks, as risk-averse entities, demand higher returns for higher-risk ventures.

Understanding the inherent risks within business operations and implementing effective mitigation strategies is pivotal in negotiating favourable interest rates. This underscores the significance of risk management in facilitating affordable financial arrangements.

Understanding commodities:

Commodities, ranging from raw materials to agricultural products, can be classified into three main categories:

- Agricultural (”Agri”) Commodities: Encompassing crops and animals from farms or plantations, including staples like grains and livestock, as well as non-food agri commodities like cotton and tobacco.

- Metals and Minerals Commodities: Covering mineral resources, industrial and base metals such as steel, copper, and aluminium, along with precious metals like gold and silver.

- Energy Commodities: Encompassing crude oil, heating oil, natural gas, and gasoline.

Each category comes with its unique set of challenges and opportunities.

Businesses seeking financial support must equip themselves with a comprehensive understanding of financial institutions, available products and services, credit policies, and procedures. Additionally, borrowers must meticulously assess and articulate their financing needs to navigate the landscape of trade finance successfully.

Determining the appropriate amount of financing is a critical facet of effective financial management. Underestimating or overestimating financial needs can have significant repercussions. Underestimation may restrict resources, expose the business to risks, or result in missed profitable opportunities.

Conversely, overestimating can lead to unnecessary debt, potential penalties for early repayment, and increased costs. Striking the right balance is essential for sustainable financial health.

Before approaching financiers, businesses must carefully evaluate their actual financing needs.

Commodity trade finance mechanisms:

It’s imperative for any Borrower to understand distinct financing terms to be able to understand the different options they have.

- Commodity Finance: The overarching term for financing activities throughout the commodity value chain, spanning production, processing, and trade.

- Commodity Trade Finance: A subset focusing on financing the underlying exchange of commodities from supplier to buyer, intricately tied to the asset conversion cycle.

- Structured Trade Finance: Another subset employing specific financing techniques to minimise risks, particularly in situations where the tenor exceeds the typical asset conversion cycle.

Decoding commodity trade finance mechanisms:

Commodity trade finance essentially acts as the bridge between the procurement and sale of commodities. It’s essential to note that this process doesn’t always involve direct funding but can be structured through contingent instruments, with letters of credit being the most common.

The choice of structures hinges on factors such as the borrower’s governance, financial position, and the type of commodities in play.

The general classifications include:

- Transactional Trade Finance: Involves a trader entering agreements with suppliers and buyers, seeking financing from their bank for purchases and sales.

- Borrowing Bases: Allows borrowers to raise finance against an aggregated pool of working capital assets, with periodic valuation setting maximum limits.

- Working Capital: Obtained based on historical performance assessments, relying on audited financial statements.

- Structured Trade Finance: Utilised for situations where financing tenor exceeds the standard asset conversion cycle, involving techniques like prepayments, tolling, and structured inventory products.

We can split the types of finance in three phases as follows:

- Pre-shipment: Pre-shipment finance includes any finance that a business can access before delivering the goods to the Buyer.

- Post-shipment: Post-shipment finance includes any finance that a business can access post-delivery of the goods to the Buyer.

- Receivables: Receivables financings refer to all financing methods used by businesses when the goods have been delivered and invoiced to the Buyer with deferred payment terms.

Navigating commodity trade finance requires borrowers to overcome obstacles, understand their financing needs, and grasp the intricacies of different financing mechanisms. Clarity and strategic approaches are essential in securing the right financial support for business endeavours.

By addressing these challenges and adopting informed strategies, businesses can unlock the vast potential of commodity trade finance, bridging the global trade finance gap and fostering sustainable growth.

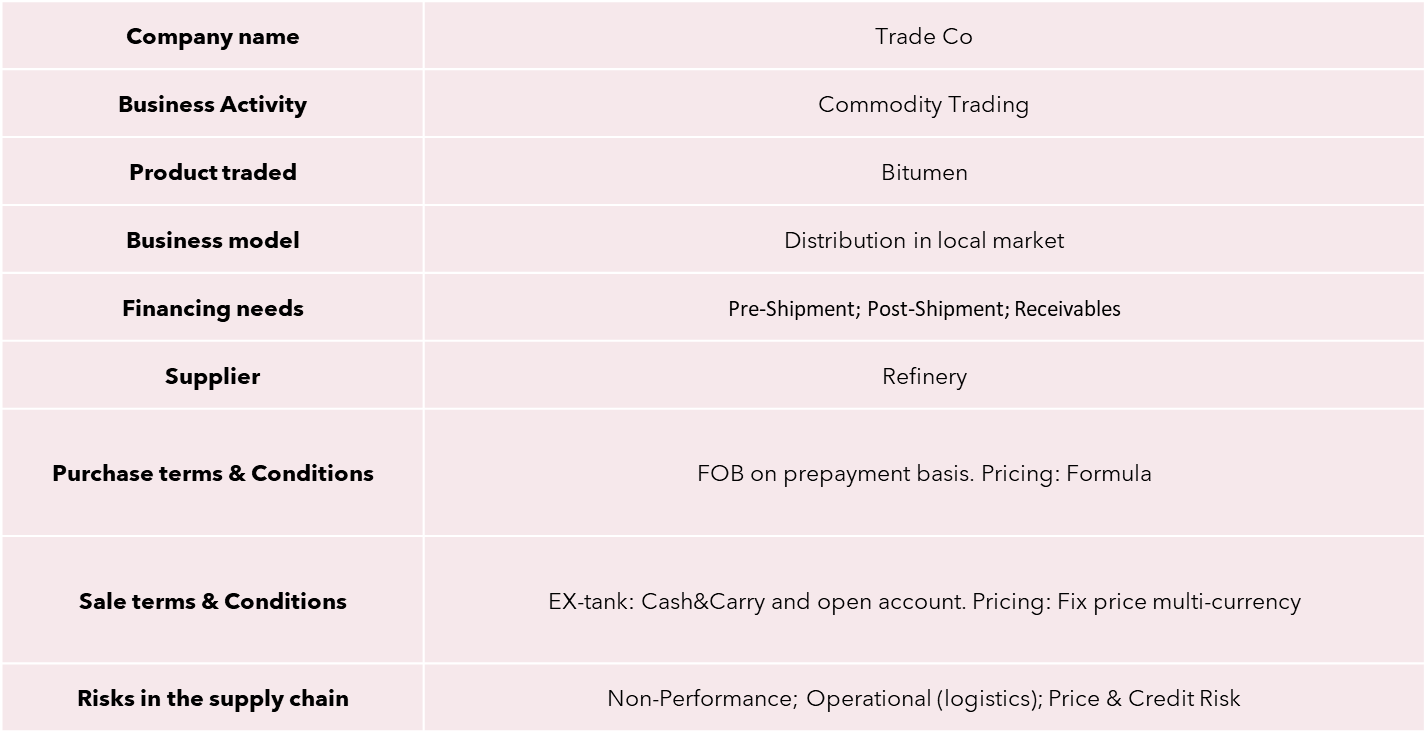

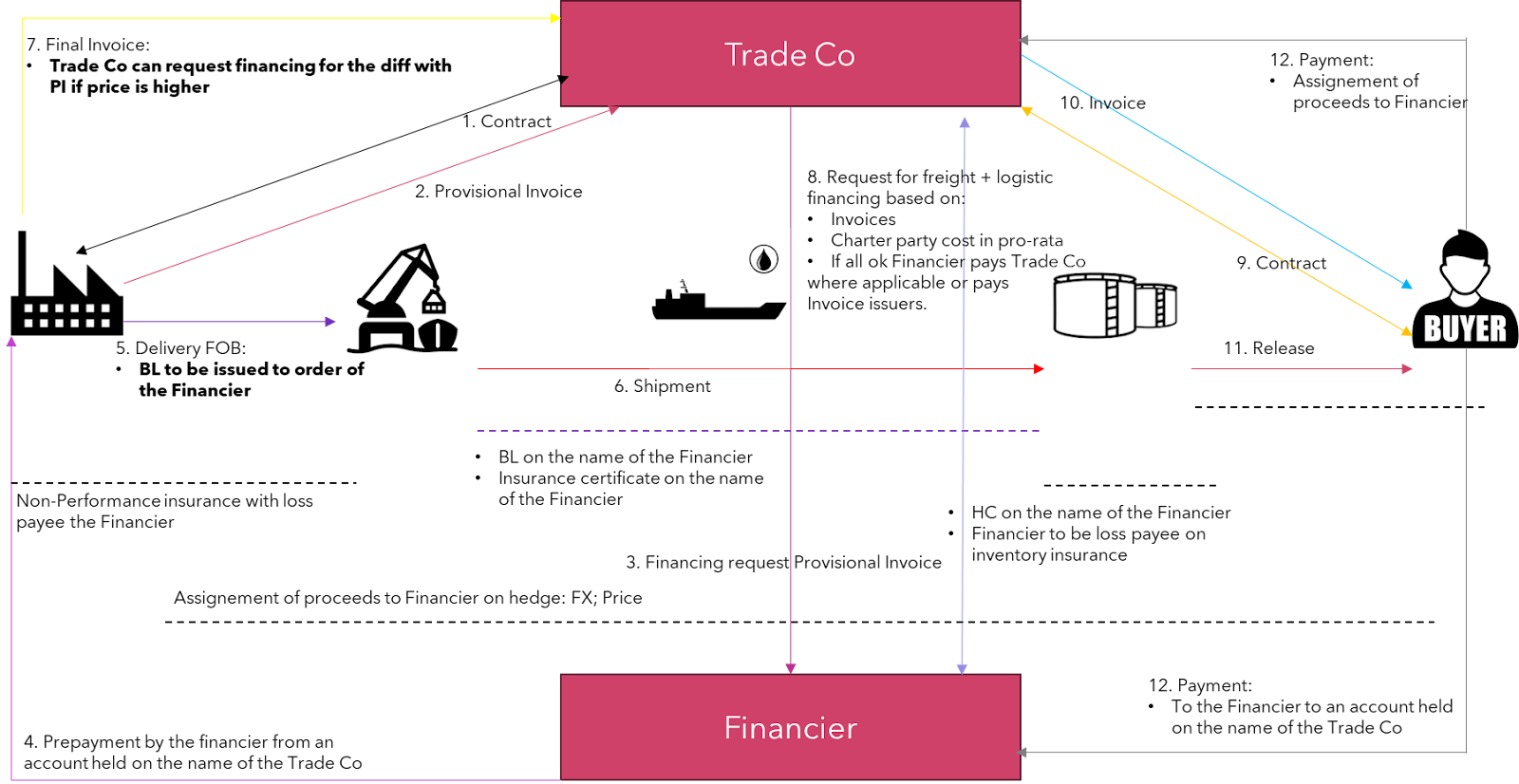

Case Study