Trade Finance Global, in partnership with Finastra, sat down with 6 global experts in trade to get a low down of 2019, the key themes and trends, as well as what’s been at the front of mind for practitioners in trade, receivables and supply chain finance.

Host – Deepesh Patel (DP)

Respondents:

- Hans Huber. Trade Finance Innovation Project Manager, Commerzbank (HH)

- Iain MacLennan. VP Trade & Supply Chain Finance (Product and Engineering), Finastra (IM)

- Peter Jameson. Head of Trade and Supply Chain Finance, Asia Pacific, Global Transaction Services, Bank of America Merrill Lynch (PJ)

- Ping Xiao. Head of Transaction Banking, Bank of China (PX)

- Sean Edwards. Chairman, ITFA (SE)

- Ms. Arancha Gonzalez Laya. Executive Director, International Trade Centre (AGL)

Geopolitics & the global economic slowdown

DP: With regard to macroeconomic movements and the geopolitical environment we have experienced in 2019, from an industry perspective what were the key trends of 2019?

IM: The trade dispute between the US and China, plus Brexit, have had a significant impact on trade throughout 2019. These have generated a level of uncertainty in the marketplace, which impacts both trade flows and overall investment.

Though, Banks have used this as an impetus to focus more on the effectiveness of trade from a back-office processing perspective. They are trying to minimize any additional costs/impacts to their customers, so innovation and efficiency are coming to the forefront in their trade processing.

HH: Despite the current push back on multilateralism, most participants in trade finance have understood the significance of communal efforts and that cooperation is indispensable in order to reap digital dividends.

The concept of cooperation has become accepted in reconstructing the paper-based world in bits & bytes. In 2019 we have witnessed widespread activities in trade digitization, which could eventually form an operating system of trade on a global scale.

PJ: Slowing global economic growth and excess market liquidity resulted in reduced demand in certain trade corridors, and increased uncertainty for clients.

The impact of various trade disputes led many to look at how to recalibrate their supply chains in response. This, combined with increasing focus on domestic supply chains, has presented opportunities for more client dialogue on their changing needs such as the need for increased risk mitigation and better working capital management.

PX: 2019 has been a year that was a mix of instability in the Macroeconomic and Geopolitical landscape and some significant wins and growth in the Trade Finance ecosystem.

The US/China Trade War and Brexit, is taking its toll in the Global landscape. Having said that, it has created some opportunities as suppliers are looking at remapping their trade flows to other regions with less or no trade wars.

SE: The effect of US-China was compensated to some extent by the continuing spin-out of the supply chain to lower costs for countries in APAC which resulted in opportunities for banks (not always taken).

The final result of US-China is uncertain given its genesis as a political contest (and so resolvable by politicians) rather than a more fundamental trade issue. Banks and other lenders have gritted their teeth and got on with it regardless during the year. South America has been strong as has Africa although the former has been hurt by the recent imposition of US tariffs.

AGL: Services sector growth (mainly led by tech., tourism and design) has doubled in most EDE countries and more young people and women are starting businesses than ever before.

There are negatives though – the impact on otherwise high growth economies of the incessant rise in bi-lateral trade agreements, national self-interest, non-tariff barriers, import-country specific market and sustainability standards, multiplying uncertainties, raising production and export costs.

Technology – Evolution or Revolution?

DP: In your opinion, what technology and innovations had the biggest impact on the trade/trade finance environment in 2019?

IM: With the use of open APIs, what were traditionally closed systems are now bringing in other capabilities to extend their offerings. For instance in document checking/compliance.

The process of checking documentation against the defined trade rules can now happen in a matter of minutes using services that combine Optical Character Recognition (OCR), Machine Learning (ML) and Artificial Intelligence (AI). Previously this would have been measured in multiple hours or days.

We are also seeing fintech developments that started in other areas such as payments coming into the trade space, for instance entity or network relationships. Plus, most operations functions are seeing an increase in Robotic Process Automation (RPA) for routine and repetitive tasks.

HH: A broad consensus seems to have been achieved in the financial industry (and others) that Blockchain/DLT is a key technology to support digital data registry in global trade and trade finance to eventually replace paper-based records. It also appears people are in consensus about other maturing technologies (i.e. Internet of Things (IoT), Ubiquitous Networking 5G) profiting from DLT, v.v.

The understanding of the powers of convergence of these maturing technologies seems to have dramatically grown in 2019.

PX: A key highlight is the unified recognition of advancement in technology as the key driver to closing down the Global deficit estimated at US$1.5trillion. 2019 has seen a significant upward traction in the push for digitization of Trade & Supply Chain Finance as the general consensus within the Trade industry is that the old way of doing paper based business is no longer sustainable. There is almost no conference you will attend today that ‘’Digitization’’ is not mentioned as the future of Trade.

SE: Consortia continue to grow thereby laying down strong roots on which networks can grow and to which utilities (KYC/AML, track and trace, IoT etc.) can attach themselves. Blockchain offers the greatest long-term transformative potential.

AGL: Open account trade and supply chain financing applications, extracting the best of distributed ledger and cloud technologies have been proven to work well – this looks good for the future of SME exporter/ processes in EDEs as it potentially reduces their cost of trade.

Unfortunately, capacity building of advisory and information services for MSMEs, traceability and digital identity, regulatory and policy reform, expansion of 3G and 4G is advancing too slowly for demand.

Regtech – helping to simplify compliance?

DP: 2019 has been turbulent to say the least – from an industry perspective how has the regulation and compliance market tied in with this?

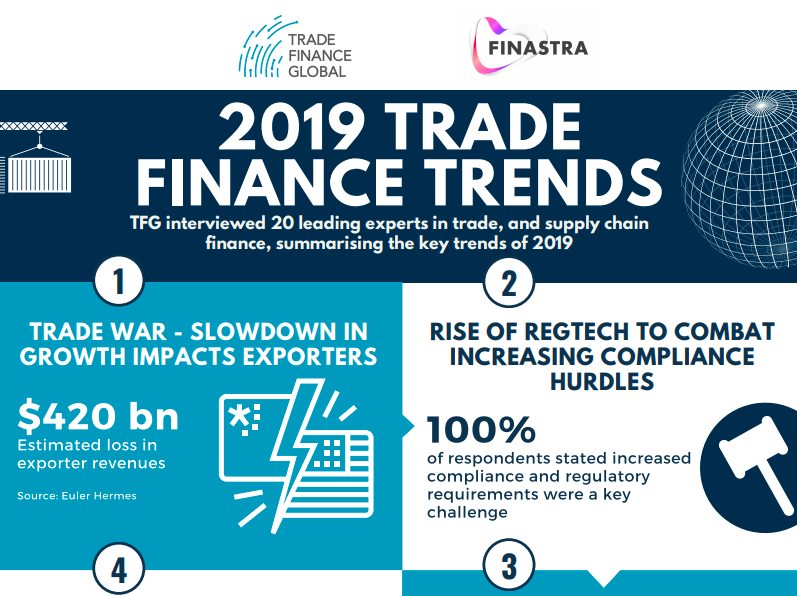

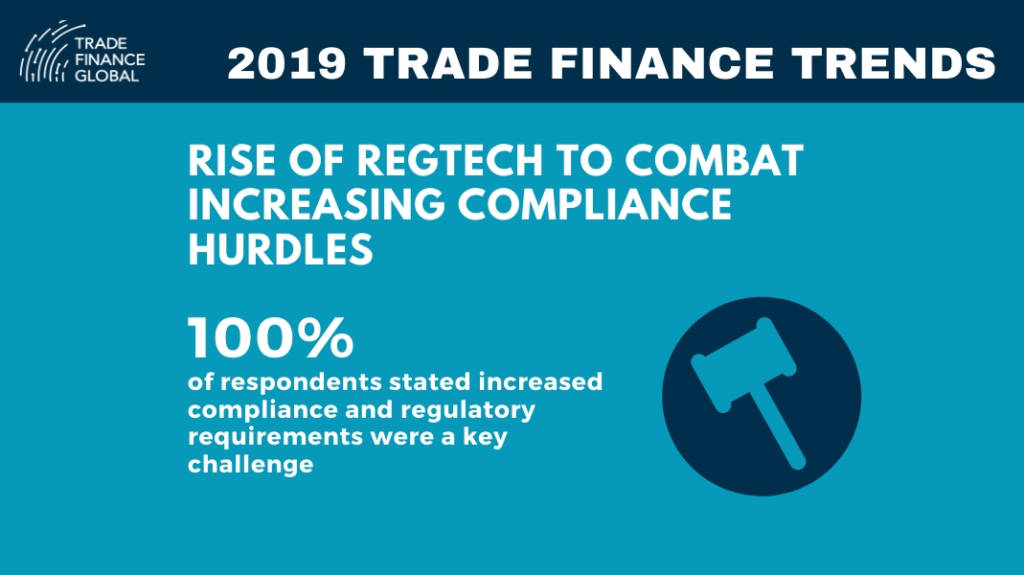

IM: Government policy continues to demand better due diligence, for instance related to Know Your Client (KYC) and Anti-Money Laundering (AML), for all the right reasons. Banks are looking to technology and big data to help address compliance to these regulations.

HH: The significance of compliance and regulation continued to grow in 2019, and the role of technology and its potential to alleviate regulatory overheads has been broadened. Appreciably, national law and policymakers became more visible and sensitized for the topic of digital policy adaption.

PJ: 2019 was another year of activity, with evolving KYC requirements remaining a challenge. There is increasing focus from regulators on data management – particularly data on-shoring requirements – and widespread adoption of real-time payment networks, which will ultimately benefit trade finance.

SE: Changes to Basle III continue to worry banks as trade may be penalised even more and lobbying is going on to raise awareness. The growth of credit insurance is impressive and ITFA is lobbying for better recognition. Sanctions have become more and more difficult for banks to administer and navigate as they become increasingly weaponised and dependent on what seems like a political whim. The AML/KYC burden has unfortunately not lessened.

AGL: Between the reduction in correspondent banks and national currency restrictions caused by indebtedness and imbalances in trade, there is a squeeze on the maximum volume of foreign trade transactions passing through banks. This has led to enterprises finding alternative non-bank solutions and a high reported gap between demand and supply of trade financing.

On a more promising note, At least four major pilot tests involving banks, donor guarantors, multi-national retail companies, technology providers and country sustainability partners were conducted successfully in 2019. These represent the first small steps that could, if expanded, incentivize improvements in trade and supply chain sustainability for thousands of supplier enterprises in EDEs.