Estimated reading time: 9 minutes

The number 13 is often synonymous with bad luck. It’s considered unlucky to have 13 friends around at a dinner party, many buildings don’t even have a 13th floor, and many avoid buying a house or getting married on the 13th of the month. This marks the 13th year of the publishing of the 2021 ICC Trade Register (reporting on 2020 data), the worlds most comprehensive record of trade finance data across 4 different trade products, representing 28% of global traditional trade finance flows. Did the figures represent bad luck, following what was, a golden streak of decreasing default rates, increasing trade finance volumes and a fairly upbeat trajectory for trade finance?

The 2021 ICC Trade Register reported the credit risk profiles of trade finance, supply chain finance and export finance transactions, looking at default rates, average maturities and expected losses for these trade products.

The report compiled data from 22 trade and export finance banks, some 38 million transactions representing USD $19.2 trillion exposures, and 28% of global traditional trade finance flows. We analysed the 52 page summary of the ICC Trade Register, here are the key findings:

1 – 2020 was an unprecedented year of disruption for global trade

COVID-19 dramatically triggered both demand and supply-side shocks for global trade, but more recently, other non-related events such as the blockage of the Suez Canal, attempts to diversify globally value chains as a result of geopolitical trade tensions and the increased focus on sustainable supply chains has most likely caused long-lasting changes to global trade.

Goods traded declined by 10% in 2020 versus 2019, with oil accounting for 34% of the decline. This was much lower than the predicted 11-30% ICC predictions, mainly due to unprecedented fiscal measures and monetary support put into place by governments around the world, as well as the resilience of the goods sector.

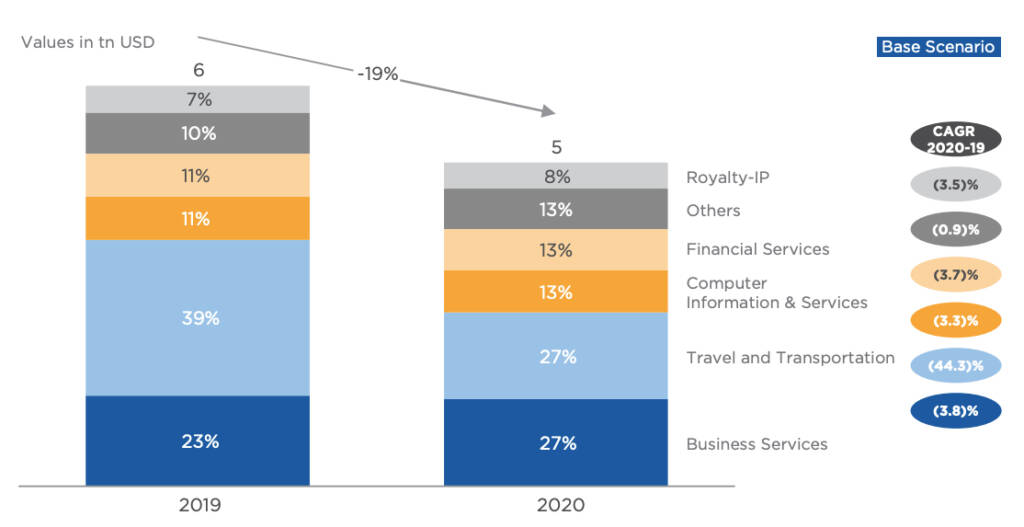

Source: ICC Trade Register 2021. BCG Trade Model 2021, DESA/ UNSD, United Nations Comtrade database, WTO, BCG Analysis

The above BCG Global Trade Model shows the drops in global trade services (which fell 19% in 2020 versus 2019), and as expected, the biggest losers being the travel and transportation sectors.

…and trade finance

Of course, trends in trade volumes impact trade finance. Revenue pools across trade finance products declined some 10% in 2020 as a result of declining trade volumes. Supply chain finance fared well, given the growth trajectory of this asset class, and the overwhelming government support in terms of shorter, credit insurance, effective supply chain finance programmes, and corporates continuing to help their suppliers throughout the pandemic, often dipping into their liquidity reserves.

- Documentary trade revenues fell 16%

- Trade loans and non-risk mitigating trade product revenues fell 13.5%

- Supply chain finance revenues fell 6%

Moving forwards, the report predicts that there will be an increase in margins as interest rates increase with inflation, and perceived risk might equate to increased pricing as governments wind down fiscal interventions for businesses.

2 – Positive trade growth outlook for 2021-2030

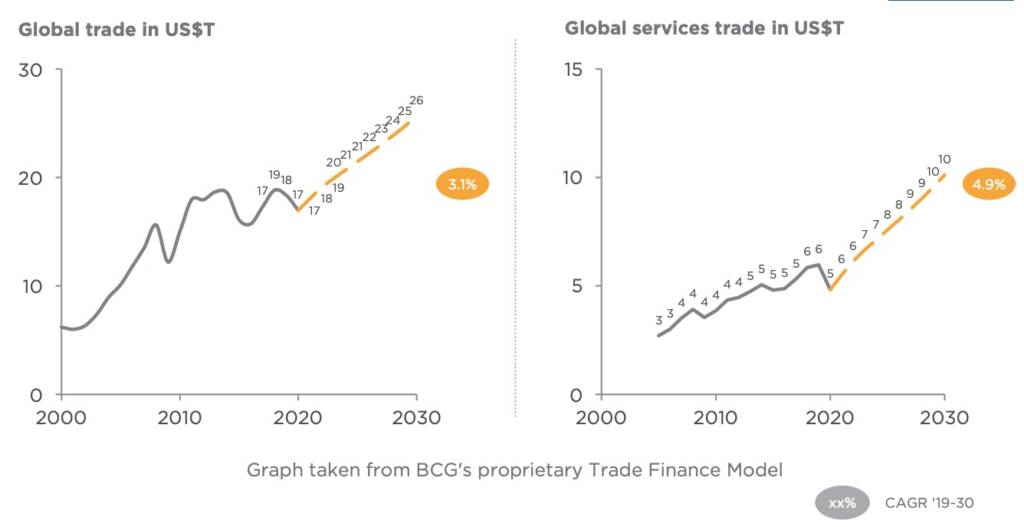

Assuming an equitable global recovery from the pandemic, free from vaccine nationalism and economies recovering at similar rates to one another, the report predicts that global trade volumes will recover to $18.1 trillion in 2021, and then exceeding 2019 levels the following year. The BCG Trade Model 2021, backed up by data from United Nations Comtrade, WTO, OECD, WEF and IHS TradeAlert data also predicts a compound annual growth rate (CAGR) of 3.1% for goods and services trade between 2019 and 2030.

Source: ICC Trade Register 2021. BCG Trade Model 2021, BCG Analysis, DESA/UNSD, United Nations Comtrade database, WTO, OECD, WEF, IHS, TradeAlert

3 – Cautious optimism for the rise in open account finance

An ongoing trend, the rise in supply chain finance, continues, as both a share of trade finance revenue pools and total revenue.

Reasons for the rise in supply chain finance:

- Forced overnight digitalisation highlights the constraints of traditional documentary trade (e.g. document checking of Letters of Credit)

- Reconsideration by businesses around how they can transact

- Corporate focus on achieving net-zero supply chains could encourage a shift towards newer SCF products

- Better business technologies around procure-to-pay, order-to-cash, e-invoicing

On the other hand, investor appetite remains a key unknown. With the high profile collapses and frauds within the SCF space over the past year, it’s no wonder reduced investor confidence in trade finance as an asset class could impede its growth. Furthermore, the potential tightening supply of trade credit insurance, which was apparent throughout the pandemic, could hinder the growth of this product.

4 – Digital trade is disrupting all trade finance products

Hang on, didn’t I say this last time? For the second year in a row, the ICC Trade Register highlighted the rise of Distributed Ledger Technology (DLT) based platforms and their movement towards maturity, as we indicated in our recent report with ICC and the WTO.

The exponential growth of DLT-based and non-DLT platforms, touted for their ability to provide real-time ownership transfer, a single source of the truth, guaranteeing the authenticity and executing smart contracts, has impacted the market heavily. BCG estimates that by 2025, some 10-15% of trade finance and 20-25% of SME trade finance will be conducted through digital platforms, as prices continue to fall and the suppliers’ cost to serve drops.

This all creates competition and a challenge for trade banks. The deconstruction of large financial institutions, from distribution, product supply, infrastructure and balance sheet, coupled with the rise of non-bank financial institutions (NBFIs), has shifted the focus on how banks should orchestrate their own ecosystems, partner with third parties or even a mixture of both.

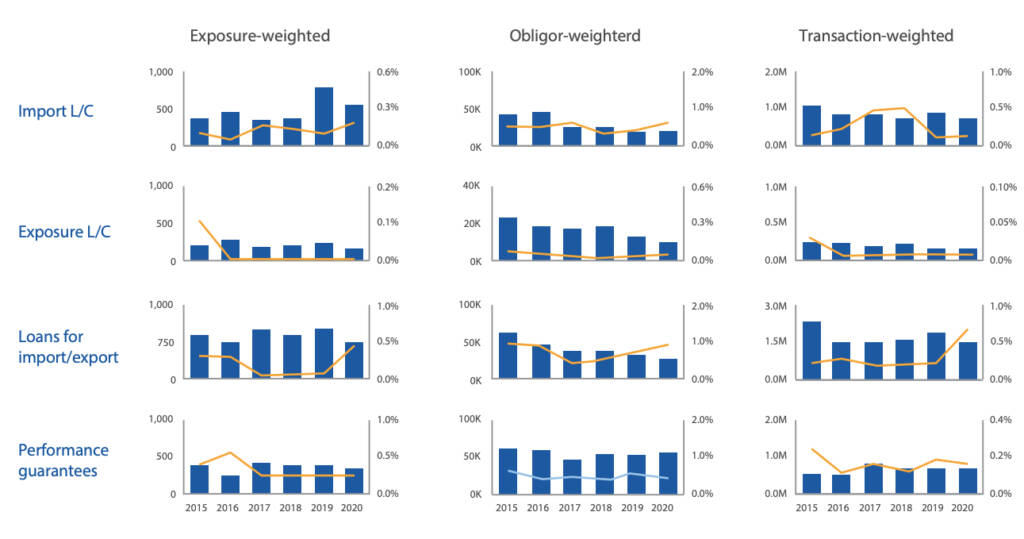

5 – Predictably, default rates spiked in 2020, but not by much

- Default rates for loans for import/export fared the worse, likely driven by the impact of the pandemic

- Preliminary analysis of SCF default rates shows a rise across all measures from 2019 to 2020, after relatively low default rates in 2019, but the default rates remain low in comparison to other trade finance products

In part due to the COVID-19 pandemic, but also due to other supply chain pressures, default rates increased across exposure-weighted, obligor-weighted and transaction weighted rates in 2020 versus the previous year.

“The ICC Trade Register has been key to developing regulators’ understanding of Trade Finance. Now, it is also a key contributor to the institutional investors’ education on this attractive asset class.” said Mencia Bobo, Global Head of Trade & Working Capital Solutions, Santander Corporate & Investment Banking, Santander.

Source: ICC Trade Register Report 2021

The above diagram shows the key findings in terms of default rates, taken from 22 contributing banks, 1.3 million obligors, representing € 199 billion exposure since 2008.

ICC Trade Register 2021 – Key highlights on default rates

Import Letters of Credit

Default rates for import letters of credit saw a downward trend from 2017 to 2019, but increasing to 5-year highs of 0.18% and 0.59% for exposure and obligor weighted rates between 2019 and 2020.

Export Letters of Credit

Default rates for loans for import/export increased from 2018 to 2019 and from 2019 to 2020, leading to 5-year peaks across all measures. The rise from 2019 to 2020 was generally steeper than from 2018 to 2019, likely driven by the impact of the pandemic

Performance Guarantees

Performance guarantees (including standby L/Cs) typically have the highest default rates of trade finance products, but the considerable jumps in default rates for loans for import/export discussed above meant that this was not the case for any weightings in 2020, and only for exposure weighted default rates in 2019. In fact, after some moderate increases from 2018 to 2019, default rates for performance guarantees went against trend, decreasing by all three weightings from 2019 to 2020.

Andrew Wilson, Global Policy Director, ICC, said: “This year’s ICC Trade Register provides substantial reassurance of the low-risk nature of trade as an asset class, while also demonstrating the immense value of a rich, data-driven and authoritative source at unprecedented times of uncertainty.”

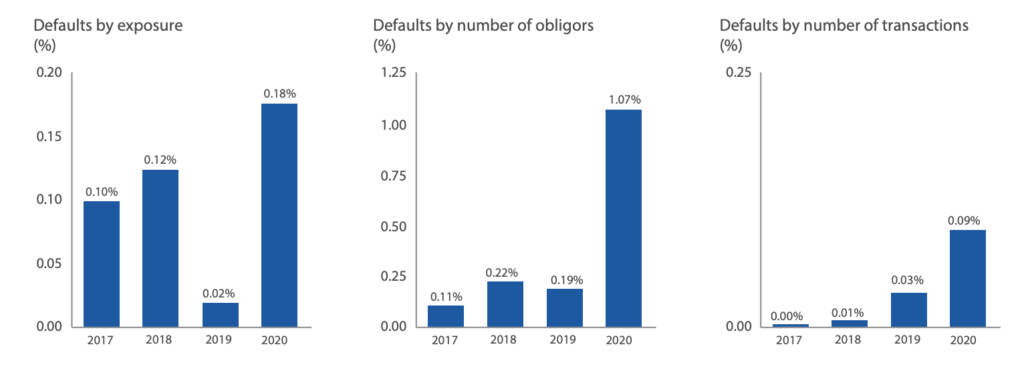

6 – Payables Finance defaults increase, although lower risk versus other trade finance products

Source: ICC Trade Register 2021

Since 2017, the ICC Trade Register has amalgamated SCF data, focusing on payables finance. Despite a smaller pool of data, the analysis shows that default rates of this product increased in terms of exposure, obligors and numbers of transactions. However, given the data size, some corporate supply chain defaults would likely skew these numbers.

The ICC Register contributors include:

Chair, ICC Trade Register Project

- Krishnan Ramadurai, Chair of ICC Trade Register Project. Global Head of Capital Management, Portfolio Management and Distribution, GTRF, H.S.B.C

Project Advisors, ICC Trade Register Project

- Henri d’Ambrières, Project Advisor, Medium-to-Long Term Trade Register, HDA Conseil

- Hugo Verschoren, Project Advisor, Short-Term Trade Register, goVer Trade Technologies Ltd, Belgium

- Christian Hausherr, Project Advisor, Supply Chain Finance, Deutsche Bank AG

Project Management, International Chamber of Commerce

- Andrew Wilson, Global Policy Director, ICC

- Tomasch Kubiak, Policy Advisor, ICC

Boston Consulting Group

- Sukand Ramachandran, Managing Director and Senior Partner

- Ravi Hanspal, Principal

- Patrick Bunker, Associate

- Nikhil Dangayach, Solution Lead, BCG Trade Model

Global Credit Data

- Richard Crecel, Executive Director

- Michaël Dhaenens, Data Operations Executive

You can download the executive summary of the 2021 ICC Trade Register report: Global risks in trade finance or order the full report here.