In a global emergency, international trade may slow but it must not stop. Even as COVID-19 reveals the shortcomings of a paper-based trade system, financial institutions (FIs) are finding ways to keep trade circulating. How are they doing it?

The International Chamber of Commerce (ICC), International Trade & Forfaiting Association (ITFA) and BAFT today shared some of the ad hoc practices being implemented by FIs under the COVID-19 pandemic.

The paper was authored by members of the ICC Digitalisation Working Group. These include: Alisa DiCaprio (r3), David Bischof (ICC), Sean Edwards (ITFA), Stacey Facter (BAFT), Alexander Goulandris (essDocs), David Meynell, and Michael Vrontamitis (Standard Chartered).

The document collates common practices undertaken by global banks in the COVID-19 emergency situation and shares some guidance. This is not a “best practices” document and many of the practices described are being improved already. Rather it is a practical reference document with information about measures put in place to continue the flow of trade and trade finance when paper transfer has become difficult or impossible. The COVID-19 pandemic has disrupted shipping, in-person interactions, and travel. As such, alternative procedures are required to settle trade finance transactions. Data was sourced from 2020 data from ICC, ITFA and BAFT members.

We should be cautious about a ‘rapid response’ approach

“We expect that many of the ‘rapid response’ quasi-digital solutions in place today will be reexamined and likely withdrawn post-crisis. However, if lessons are learned, this experience will positively change how banking and trade finance is originated, transacted and settled.”

ICC Digitisation Working Group

The experience of rapid digitisation should not go to waste. Both FIs and corporates will need to re-engineer business processes following COVID-19. And we strongly believe that governments will be an enabler for this. ICC has created tools, such as the Digital Trade Roadmap, to promote this long-term digitisation.

Paper; the Achilles heel of financial services

The problem being faced today is rooted in trade’s single most persistent vulnerability: paper. Paper is the financial sector’s Achilles heel. The disruption was always going to happen, the only question was, when.

David Meynell, Managing Director at TradeLC Advisory told TFG: “Organisations have moved efficiently and effectively to overcome the chasm caused by the non-movement of paper, and we may now be finally viewing the catalyst that will encourage full digitalisation.”

Preliminary ICC data shows that financial institutions already feel they are being impacted. More than 60% of respondents to the recent COVID-19 supplement to the Trade Survey expect their trade flows to decline by at least 20% in 2020.

To help combat the practicalities of trade finance in a COVID-19 environment, many banks indicated that they were taking their own measures to relax internal rules on original documentation. However, only 29% of respondents report that their local regulators have provided support to help facilitate ongoing trade. Without significant regulatory support, the effectiveness of individual banks’ measures will be limited.

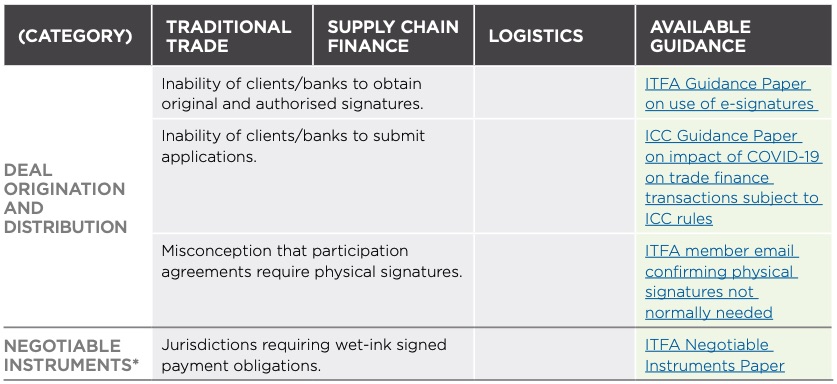

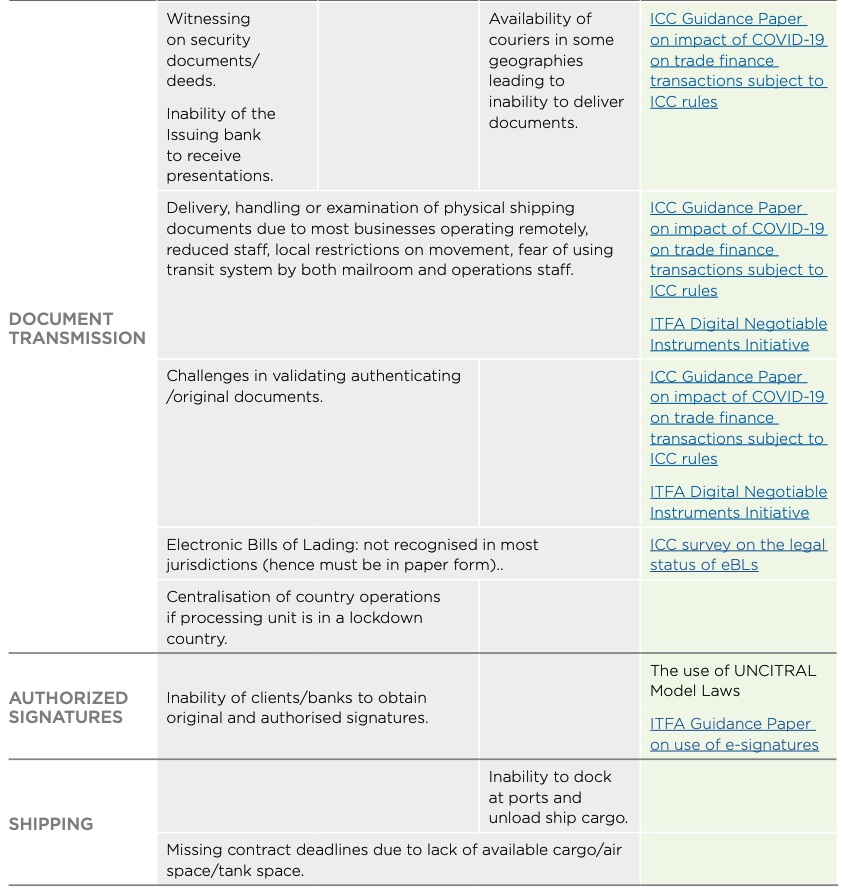

The pandemic introduces or exacerbates challenges to five parts of the trade finance process. Respondents report immediate and significant issues with:

- deal origination and distribution

- negotiable instruments

- document transmission

- authorised signatures; and

- shipping

The specific difficulties FIs face in these five areas are detailed in Table 1. They largely reflect three common hurdles introduced by the pandemic: lack of staff, inability to print and delays in/inability to deliver. According to anecdotal evidence, in April 2020 most banks report having between 75-90% of operational staff working from home. Where available, column 5 includes existing guidance. The papers referred to have been produced in response to requests by bank members of various trade associations.

Michael Vrontamitis, Head of Trade, Europe and Americas at Standard Chartered Bank, told TFG: “In our pursuit of trade digitisation to ease the flow of goods, enable cost savings and improve working capital through trade finance, we never imagined that the inability to connect ‘digital islands’ would be a health concern for the millions of people that need to process the billions of physical pieces of paper in trade. While we have seen digital ‘hacks’ to get us through, this comes with increased risk. Post crises it is going to be critical governments, companies and industry actors to enable the system to be natively digital.”

The difficulties faced by banks are a function of the nature of trade. Many of the issues impacting banks in fact originate with the client and then affect multiple stakeholders—including shipping companies, customs and others. This highlights the fact that bank-based solutions alone cannot solve the problem.

Key Reference Points and available guidance

ITFA Guidance On Digitally Signing Master Participation Agreements

ICC Guidance on The legal status of electronic bills of lading

Common practices rapidly evolved

According to the paper, FIs responded quickly to the supply chain disruptions of COVID-19. As of April 2020, 71% of respondents to an ICC survey report implementation of COVID- 19-related measures to support customers. These measures support customers even as FIs themselves are disrupted in their business practices. The depth of FI disruption is illustrated by anecdotal evidence from BAFT’s Trade Finance Committees calls. FIs report that most have 75%-90% of operational employees on mandatory work from home. The others are placed on rotating shifts in order to receive, print and ship physical documents that remain a key part of trade finance flows.

The ad hoc practices banks have put in place fall into four categories:

- Expanded existing digital channels

- Electronic documents

- Electronic signatures

- New business processes and controls

Stacey Facter, Senior Vice President of Trade Products, BAFT told TFG “The COVID-19 crisis has highlighted the importance of moving trade finance from paper to digital solutions. As digital trade is the fastest growing means for individuals around the world to exchange goods and services, BAFT is pleased to have co-authored an essential industry paper meant to keep trade flowing despite these unprecedented disruptions. As many financial institutions are facing similar challenges, we are certain this joint endeavor will suggest various interim practical solutions to implement today.”

Trend 1 – eSignatures

The first trend is an evolution in the practices related to electronic signatures. For those transactions that were nearing completion at the outset of the lockdown period, the objective was to find immediately implementable solutions that were within the grasp of workers with limited hardware, software and IT skills. As email was generally available to most people, “signature by attached email” was widely used. Within a relatively short period, greater familiarity with digital signatures/certificates led to a greater use of these as they are, broadly, more robust and secure. The next phase in this evolution is a more intense examination of, on the one hand, the legal requirements to ensure the optimum legal solution e.g. qualified legal signatures under the European eIDAS4 regulations and a wish to integrate these tools into more holistic Enterprise Resource Management processes with as little human intervention as possible.

Trend 2 – Electronic documents

The second is in the practices related to electronic documents. This is moving forward most easily in geographies where local authorities have issued official guidance. Guidance is necessary because legislation allowing for digital documentation is considerably less advanced than that related to electronic signatures. It must also deal with formalities at both a legal and practical level. Electronic documents sit at the uncomfortable intersection of 19th century legislation and unsophisticated 21st century operators. In contrast to electronic signatures, which many countries in the world at least nominally accept, progress on electronic documentation lags considerably.

Sean Edwards, Secretary General of ITFA, added: “Harnessing the efforts of three associations meant that we were able to play to our strengths and produce a really useful and practical paper. For ITFA, this allowed us to showcase two recent initiatives. Firstly, our guidance on the use of e-signatures which we produced very quickly after the onset of the lockdown and which has been well received and widely implemented but represents only the first step in the journey to embed electronic signatures into trade documentation. By contrast, our digital negotiable instruments paper has been worked on for some time and sets out the potential for a real step change in trade finance combining trusted instruments which have been around for century with the best cutting-edge technology.”

Alexander Goulandris, CEO of essDOCS, told TFG: “It is imperative that we engage with governments to catch-up with the needs of the industry, by recognising electronic documents: the UNCITRAL Model Law on Electronic Transferable Records, if widely adopted, is a simple, immediately available route for ensuring that electronic bills of lading, bills of exchange and promissory notes are the functional equivalent of their paper counterparts and will solve the cross-border trade challenges faced today. In the meantime, contractual solutions, which are readily available and are seeing increasing adoption in recent months, provide an immediate path to paperless for the international trade community which needs solutions now.”

Trend 3 – digital solutions and platforms

A third trend is in the rollout of digital solutions. Where existing digital platforms are in place, FIs report scaling them up. We expect that this is what 53% of ICC survey respondents mean when they report rolling out new digital solutions in response to COVID-19. There is increased focus on the more rapid adoption of blockchain, the digitisation of documentation and automated processing and handling software and platforms.

The risks of deploying a rapid response to digital solutions

The paper also described that the. rapid deployment of digital solutions introduces new risks into the existing trade processes, as survey respondents concurred. There is, therefore, a critical role in mitigants and official guidance when it comes to diverting away from customary business practices.

Mitigants and controls include:

- Call back mechanisms (bank teams actively calling corporates)

- Relevant clauses added to, or modified in, documentary credits or transactional documentation to protect the parties

- PDF documents accompanied by authenticated SWIFT messages

- Alternative arrangements with transacting parties when documents cannot be delivered

Alisa DiCaprio, Head of Trade & Supply Chain at R3 told TFG, “One of the key lessons is that rapid response scaling up of digital products was only done under exceptions from normal process. This underscores the importance of blockchain solutions for long term digital infrastructure. It scales, it digitizes, and it connects networks together.”

A changed face of trade finance forever?

So why weren’t there digital measures put in place already? There are three answers: cost, complexity and networks.

First, cost of both implementation and onboarding. While pre-existing digital measures like DocuSign or other platforms can be expanded, such products are not free of cost. Additionally, the use of digital platforms often involves training staff and customers how to use them. This often is phased in, as immediate implementation has the risks described above.

Second, some parties will require paper originals. In a trade transaction there are many counterparties and if a single one requires the original to be on paper for regulatory or legal reasons, then the process has to be, at a minimum, partially paper from origin. Understanding which clients and counterparties will require paper originals is a lengthy process.

Third, a trade transaction often interacts with insurance. If insurance is required, it should be noted that many underwriters are heavily paper based. Any successful long-term digital solution must be able to connect networks without require a centralised operator.

This paper has been published on ICC, ITFA and BAFT’s websites. Full guidance from the ICC Digitalisation Working Group can be found here.