Eurozone inflation hit a record high in December 2021, as soaring energy prices continue to put pressure on consumers, highlighting the risks of the green energy transition.

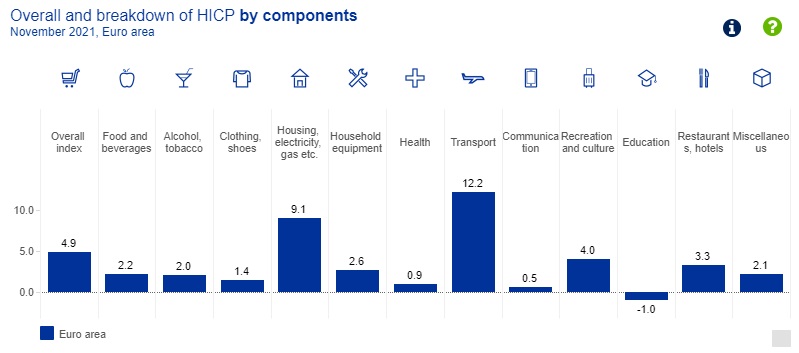

New data from Eurostat, part of the European Commission (EC), show that Europe’s harmonised index of consumer prices (HICP) hit 5% in December 2021 year-on-year.

This represents the HICP’s highest reading since the euro was introduced in 1999, and an increase from 4.9% recorded in November 2021.

Among the factors believed to be driving the eurozone’s record inflation is rising energy prices, particularly those affected by natural gas.

Energy prices in the 19 countries that share the euro increased 26% in December compared with a year earlier.

Isabel Schnabel, member of the executive board at the European Central Bank (ECB), said that rising gas prices have a “direct and immediate impact” on wholesale electricity prices in the European Union (EU).

Speaking this weekend at an event on ‘Climate and the Financial System’ at the American Finance Association, Schnabel said that such price hikes have led to an increase in short-run marginal costs for gas-fired power plants.

Counting the cost of high gas prices

In November 2021, wholesale electricity prices in the eurozone hit €196 per megawatt hour, nearly four times higher than the average from during the two years before the outbreak of the pandemic.

As a result, energy price inflation as a sub-index of the HICP reached a historical high in November last year, with gas and electricity jointly accounting for more than a third of the total increase.

Consequently, energy has been the prime factor behind the sharp rise in overall consumer price inflation in the eurozone.

Between April and December 2021, energy contributed, on average, more than 50% to HICP inflation.

Policy choices – supporting the vulnerable and supporting green transition

Schnabel went on to say that energy price inflation poses significant challenges to policymakers, both in government and central banks.

In the context of the green energy transition, Schnabel acknowledged that “carbon taxes tend to be regressive”, since the lowest-income households spend the largest proportion of their income on fuel and electricity.

And with record energy price inflation comes record pain for those households.

In 2020, for example, 8% of the EU population, or 36 million people, said that they were unable to keep their home adequately warm, according to a survey referenced by Schnabel.

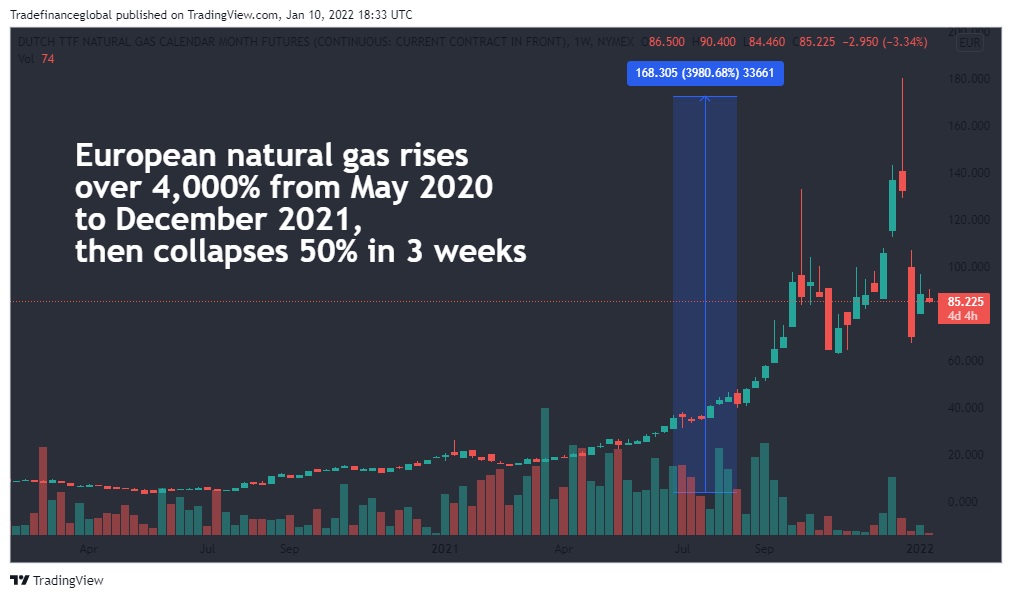

This figure is now undoubtedly much higher, given that wholesale European gas prices (TTF) have increased over 4,000% from May 2020 to December 2021, even though they have dropped around 50% in the last three weeks.

On the fiscal side, Schnabel welcomed energy cost-cutting measures from European governments such as tax cuts, price caps, and rebates to safeguard vulnerable households.

However, she also said that such measures shouldn’t come at the expense of delivering a green energy transition.

“Energy poverty is a serious threat to the cohesion of our society and to the support for climate-related policies,” she said.

“Compensation measures are therefore important, but such measures need to be designed in a way that does not reduce the incentives to lower carbon emissions.

“It would be a serious mistake if governments, faced with rising energy prices, backtrack from their commitment to reduce emissions.

“Governments should also not slow down the pace of the transition or delay the phasing out of fossil fuel subsidies.”

Policy solutions

Among the policy options to promote green energy while shielding the vulnerable, Schanbel voiced her support for two proposals put forward by the European Commission.

“One is the introduction of the Social Climate Fund, which aims to address the social impact of higher energy prices resulting from the proposed broadening of the scope of the emissions trading system (ETS),” she said.

“The other is the proposed system for EU countries to jointly procure strategic reserves of gas that can be released in the event of supply shortages.”

The procurement of strategic reserves would seem to be an obvious choice to ease supply constraints, particularly ahead of Europe’s cold winters.

At present, as Schnabel noted, the capacity utilisation of gas storage facilities in Europe is just under two-thirds, or almost 20% below seasonal norms.

Moreover, late last year, the EU had to tap into its strategic reserves due to supply issues with Russia, its largest supplier, which provided 49% of extra-EU net gas imports in 2020.

In October last year, Russian President Vladimir Putin promised to increase gas shipments to Europe, but two months later, the opposite happened.

Since December 21, the Yamal-Europe pipeline, controlled by Russia’s state-owned Gazprom, has been flowing in reverse, i.e. it has been shipping gas back to Russia from Europe.

Due to high prices, analysts and Gazprom said that European traders had stopped bidding for wholesale gas delivered via the Yamal-Europe pipeline, and were relying instead on reserve stockpiles, according to a report from Reuters.

The geopolitical dimension of Europe’s gas crisis

Further supply issues could also be about to hit Europe’s natural gas market due to geopolitical tensions between Russia and the west.

For several months, EU countries have been warning of a build-up of Russian forces on the eastern border of Ukraine, which has led to negotiations between the US and Russia in Geneva, which started yesterday.

Additionally, the EU is also caught in a stand-off with Belarusian president and Kremlin ally Alexander Lukashenko.

Accused of trafficking migrants from the Middle East into Europe via the Poland-Belarus border, the EU has imposed sanctions on Lukashenko, who in November hit back with threats to cut off the continent’s gas supply.

“They [western countries] want to create a provocation, to pit our border guards and theirs against each other,” he said.

“Let them scream and squeak. We are warning Europe, and they threaten us to shut off the border after all.

“And what if we cut off natural gas supplies?”

Green transition and upside risks to inflation

With such uncertainty ahead, it is no wonder that Schnabel admits that a green energy transition, if pursued at its current pace, will pose “upside risks” to medium-term inflation in the EU.

In the past, central banks have tended to “look through” energy shocks, she said, since they are normally due to temporary supply-side shocks that warrant no deviation from a 2% inflation target.

However, such supply-side shocks have never been combined with the wholesale replacement of fossil fuels as an energy source, as is the current long-term goal for the EU.

“Potentially protracted supply and demand imbalances related to ‘transition fuels’, such as gas, as well as the fact that carbon prices are likely to rise further, and to extend to more economic sectors, mean that the contribution of energy and electricity prices to consumer price inflation could be above its historical norm in the medium-term,” said Schnabel.

“The energy transition therefore poses measurable upside risks to our baseline projection of inflation over the medium-term.”

At the ECB’s Governing Council meeting in December, Schnabel said that such risks were one factor in deciding on a step-by-step reduction in the pace of asset purchases over the coming quarters.