Estimated reading time: 5 minutes

From payments, credit and lending to trade and supply chain finance, the entire financial services industry is being disrupted. Regulatory requirements, industry standards and the environmental, social, and governance (ESG) agenda have accelerated.

Economic and marketplace uncertainty, supply chain disruptions, and the pressure to meet changing customer demands have led to a turbulent situation for financial services.

Thankfully, innovation and new technologies are quickly progressing from industry trends to provide banks with real-world use cases that enhance how they do business. This is enabling them to reach new customer segments, remain agile enough to navigate new demands, reduce efforts to comply with regulations, and improve risk management.

The positive sentiment stems from financial institutions recognising that they are stronger when united. Collaboration through open finance and APIs is crucial for banks to future proof their business and combine best-of-breed industry expertise and financial services to support truly digital, frictionless cross border trade.

A new era of tech-driven trade finance

Paper documents and original signatures are costly, unsustainable, can be easily duplicated and are the main cause of friction in trading. The Model Law on Electronic Transferable Records (MLETR) provides a framework in terms of the digitisation of paper documentation, paving the way for digitised, real-time trade and settlement that enables banks to serve more customers through streamlined and efficient processes.

Now that the Electronic Trade Documents Act is officially an act of law in the UK, other markets are expected to quickly follow suit. This is hoped to have a significant impact on international trade by reducing friction, making it easier and cheaper for companies to buy and sell internationally and helping to reduce financing gaps for MSMEs.

By reducing barriers to entry, costs and friction in trade, and improving accessibility and availability of liquidity, companies can grow faster and increase their trading volumes. The success of digital trade will be supported by – and in turn encourage the increased adoption of – technologies such as AI, ML, the Internet of Things (IoT) and distributed ledger.

Improved access to digital data and technologies such as AI and ML enable banks to automate and improve processes such as credit decisions. Adopting digital identities can further reduce the processing time and costs for compliance in loan processing.

This is particularly advantageous for MSMEs, whose loan applications are often rejected in the Know Your Customer (KYC) or Anti Money Laundering (AML) phase because they lackthe necessary proof of identification or ‘institutional data’.

Additionally, distributed ledger technology and blockchain enable actors in the supply chain to exchange information securely and quickly. Documents become less prone to forgery and are more transparent, and smart contracts can be used to automate and process transactions in real time.

Utilising advanced data and AI-driven analysis provides banks with a holistic, on-demand and streamlined view of their customers and their business, which can be used to facilitate more personalised services to improve customer retention and acquisition.

This includes meeting the high demand for embedded, connected and automated finance through IoT, as well as supporting sustainability initiatives.

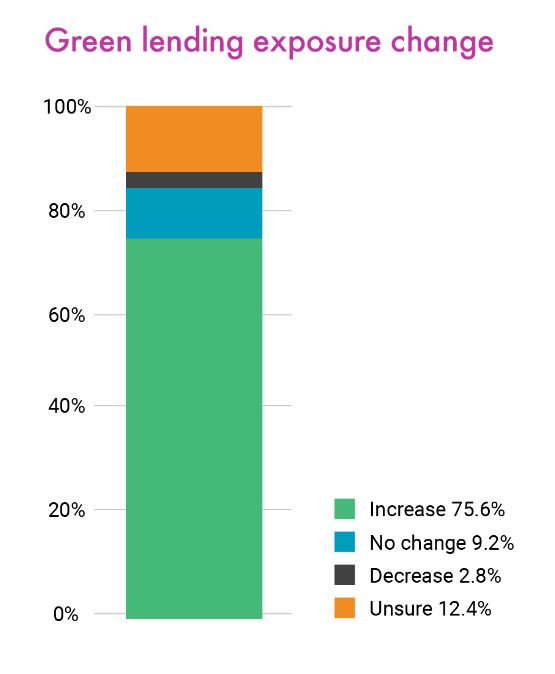

According to Finastra’s survey in collaboration with East & Partners, three out of four global banks plan to increase their exposure to green lending by more than 16% in the next 12-18 months or more.

Through increased product innovation and data analytics, banks can generate industry and regionally relevant ESG KPIs and use them to accurately assess the credentials of corporates. They can then provide incentivised trade finance or other loan offers to those that are considered “green” or “greening”.

Digitalisation through ecosystem play

For financial institutions to effectively support digital trade and remain competitive, industry collaboration is essential. Finastra’s research reveals three in four global banks are planning to connect with an average of three fintechs in the next 12-18 months. The largest proportion of respondents want to plug into a platform of integrated fintech solutions (56%), with only 6% preferring to build capabilities in-house.

A key starting point for banks is ensuring that middle and back-office processing systems are up-to-date and support the adoption of new processes, technologies and improved data access.

Collaborating with companies that offer cloud solutions and open ecosystems gives banks the agility required to digitally transform their operations and seamlessly implement technologies and third-party applications, such as for document compliance checking, AML and KYC compliance. In addition to acquiring the agility needed to swiftly adapt to new customer, industry, and regulatory requirements, partnerships contribute to enhanced scalability and decreased capital overheads, as well as a reduction in the time to value.

Despite our increasingly fragmented world, the international trade ecosystem is becoming more open, collaborative and transparent than ever before. Through open APIs and open finance, banks are able to embrace new technologies and connect previously disconnected “digital islands” to create a truly digital, sustainable and inclusive trade and supply chain finance industry that is well-equipped to adapt to future demands.