Part 2 of 3. Debt sustainability in African countries in a huge concern, with recent IMF ratings plunging for both Zambia and Ethiopia. Off the back of this drop in creditworthiness, TFG spoke to Robert Besseling, partner at Exx Africa, in a 3 part report on Africa’s debt sustainability.

Debt sustainability in Africa

Debt sustainability has deteriorated in several countries in the region

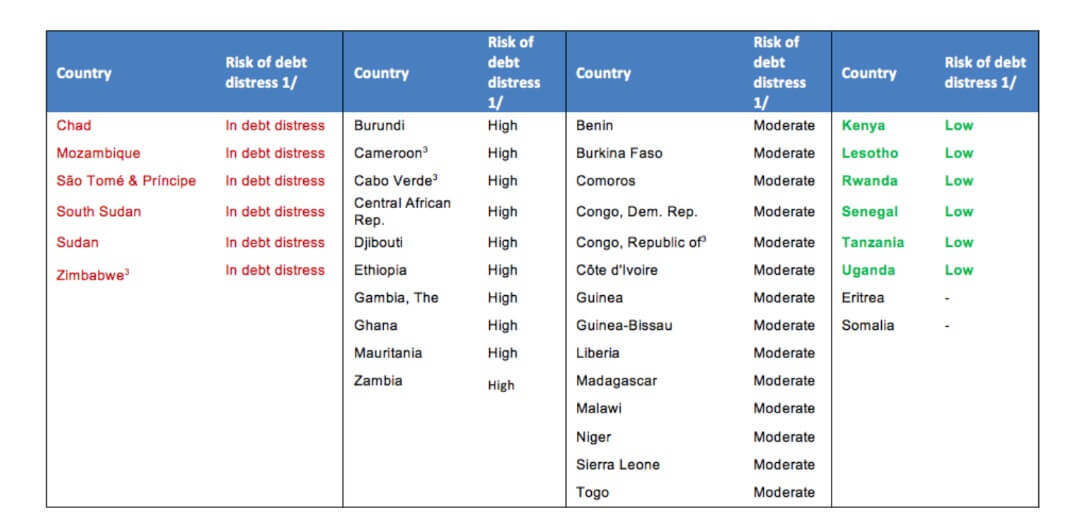

Six countries were classified as in debt distress in August 2018 in the IMF list of Low-Income Countries (LIC) DSAs for PRGT-Eligible Countries. Earlier this year, the IMF ratings for Zambia and Ethiopia were changed from moderate to “high risk of debt distress”. Zambia’s Eurobonds have lost 10% in August, more than any of the 75 countries in the Bloomberg Barclays emerging markets USD sovereign bond index. Zambia’s creditworthiness has been downgraded twice in the past month. S&P Global Ratings recently cut the foreign-currency rating to B-, six steps into junk territory. Just before that, Moody’s Investors Service lowered its assessment of Zambia to Caa1.

The IMF has put Zambia’s quest for a support facility on hold due to the country’s inability to service its debt obligation. Ethiopia’s economy is expected to expand 8.5% in 2018/19 fiscal year, however public sector borrowing, inflation, and external imbalances will remain a source of macroeconomic risk.

1/ As of August 01, 2018 and based on the most recently published data, 6 countries are in debt distress

3/ PRGT-eligible IDA-blend countries

The joint World Bank-IMF Debt Sustainability Framework (DSF) was introduced in April 2005 to help guide countries and donors in mobilizing the financing of Low-Income Countries (LICs)’ development needs, while reducing the chances of an excessive build-up of debt in the future. The DSF analyses both external and public sector debt and is periodically reviewed.

Exx Africa: Countries at highest risk of debt distress in two-year outlook

- Burundi: The shortage of aid and foreign funding, on which the economy heavily relies, will continue to hurt the budget balance. Growth is forecast at under 1.0% for this year and domestic tax collection and modest revenues from coffee and tea exports are not enough to boost the economy, despite steady growth in export sectors.

- Congo Republic: The country’s fiscal strength is very low, with large fiscal deficits. Output has contracted and low revenues from low oil prices have put debt servicing under pressure. Corruption is a major constraint with public debt to GDP ratio forecasted at over 100% for 2018. Growth is forecasted at under 2.0% for this year and the fiscal deficit is set to widen further over the next two years.

- Mauritania: A drop in commodity prices has led to a high fiscal deficit. The government has used external borrowing to finance its budget deficit. Growth is forecasted to decrease this year and the upcoming 2019 elections can also increase public spending and undermine growth.

- Sierra Leone: The IMF has frozen its loan facility of over $230 million due to government mismanagement and corruption. The new government is looking at measures to generate revenue and diversify the economy as growth forecast for this year remains at the same level of 2017. Public debt is forecasted to increase for the next three consecutive years.

- Zambia: Estimated 2018 Q1 figures showed that growth deteriorated to 2.6% from 3.3% in 2017 Q1. Non-concessional debt is more than 50% and foreign exchange earnings are insufficient for debt service obligations. How to tackle the debt crisis will be reflected in the budget for 2019. There are serious concerns over Zambia’s lack of disclosure of PPG debt.

Download Report Here