Euro Exim’s Compliance and Operations Head Graham Bright spoke to TFG on their decision to join other global Ripple participants for the first project, namely using the xCurrent service where institutions are able to instantly settle cross-border payments with end-to-end tracking and visibility.

Euro Exim Bank – Explained

International trade has never been more active and trade finance continues to play a strategic role in the flow and movement of goods and services. Following our most recent article on Euro Exim’s move into cross-border payments using Ripple’s xCurrent and xRapid products, we spoke to their Head of Compliance and Operations, Graham Bright.

We deal with extremely diverse products, with unique deals each with its own challenges. Additionally, the trade arena is fraught with problems of fraud, missing goods, fake documents and intent to avoid payment. We are always mindful of an ability to pay and intent to pay, with instruments requiring settlement up to one year later. And as the bank may have responsibility to pay according to the very tight terms of any agreement, risk avoidance is the key as banks remain reluctant to handle even small transactions. This puts unprecedented pressure on bona-fide customers to lodge excessive collateral in escrow, pay large up-front fees, thereby deeply affecting cash flow in the case of small suppliers unfamiliar with a letter of credit process and their ability to complete in international markets.

We had already created a cloud-based blockchain enabled trade finance application, so it was a quick decision to join other global Ripple participants for the first project, namely using the xCurrent service where institutions are able to instantly settle cross-border payments with end-to-end tracking and visibility.

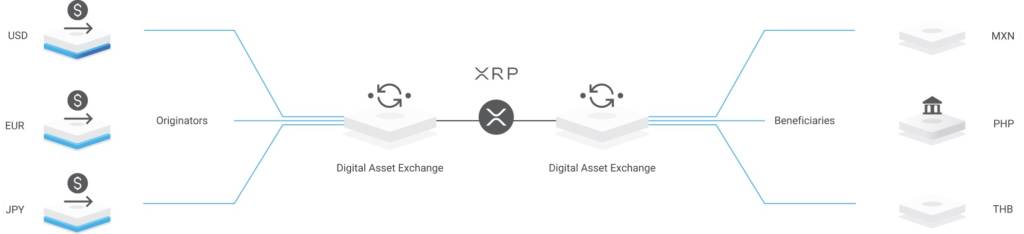

Euro Exim Bank are now working closely with technical resources at Ripple, and have successfully implemented the xRapid system for customers requiring low value remittances in currencies and jurisdictions typically subject to large exchange costs, costly liquidity and delivery time and acceptance issues. Using underlying XRP digital assets (not mined or subjected to wild price fluctuation) through registered exchanges which minimise liquidity costs, local recipients may be paid in local currency, assisting the secure flow of money and reduce cash flow restrictions.

Touted as the ‘technology of trust’, blockchain/DLT is an ideal mechanism to transfer assets and payments in real-time, establish immutable ownership of money, goods or information. Through blockchain technologies with its ability to safely store, and impossibility to add remove or change information without detection.

With digitally issued and verified identification securely held, financial fraud and risk should be significantly reduced and the risks of anonymity eliminated, seriously impacting if not eradicating the opportunity for fraudsters to operate in these once lucrative markets.

The consortiums offer innovative facilities to optimise open account trade finance through options in supply factoring, payment commitment and receivables financing. As an associated business sector we are reviewing their offerings with plans to further understand and collaborate with their capabilities and technologies. We are interested to expand our services, especially where API’s and standard approaches to data sharing and definitions of data formats can be easily integrated into our systems, providing a seamless experience for our clients with cost-effective efficient delivery of services. Fast implementation and access to new markets are key positives for us and these initiatives are prime examples of how the trade space is increasingly reactive with ideas that are becoming tangible deliverables for the benefit of the industry in short time frames.

The nirvana of fully borderless trade is becoming more difficult to achieve. In the past, nation states created incentivising agreements and economic conditions to promote free movement of trade. Today, over 400 regional trade agreements exist, however, governmental self-interest, diverse political influence and a surge in regional nationalism continues to change and challenge the trade landscape. Dissenting protectionist voices are increasingly heard across once friendly alliances, and with tighter financial controls and de-risking, smaller international suppliers in more remote jurisdictions are being marginalised in favour of protectionism favouring local, higher priced providers.

As a neutral organisation, we facilitate global trade and work with trusted suppliers across the globe providing services in the most economic, compliant and equitable way. This means serving buyers across the globe with efficient delivery of trade instruments, with associated borderless frictionless real-time payment mechanisms.

Global payments look set to be a $2-trillion industry by 2020, but is still hampered by high fees, best rate setting, risk of fraud, speed, regulation, multiple banking relationships and cashflow impact. DLT is envisioned to resolve these issues and again offer cost efficiencies, speed and immutability concerning each transaction.

Regarding global trade, 2017 WTO members’ merchandise exports totalled US$ 17.43 trillion with the top three nations accounting for exports totalling almost US$ 5,300 billion. For this immense complex global market, built on centuries of traditional practice, the benefits of DLT will build digitized trust across the entire trade ecosystem, principally with corporates, banks, service providers, regulators, insurers and shippers.

We believe that use of DLT will further evolve to be the de-facto delivery mechanism for the better visibility, transparency, trust, security and accessibility of digitized trade documents, with significant cost savings or even cost elimination in some cases.

We have already progressed beyond proof of concept.

Our proof of concept is already complete. We are happy to report that Euro Exim Bank have already started instructing global payments using the Ripple xCurrent DLT platform. Our next steps are to make trade finance instruments available via the same delivery mechanism, enriching payment instructions with the underlying Letter of Credit information, and extend our low-liquidity real-time xRapid capabilities.