The most important IT investments of companies, banks, and financial institutions are in collaboration with business partners, digital transformation, big data, and analytics, as well as artificial intelligence and machine learning. This places their joint digital processes in focus.

So let us take a look at the core processes in global trade finance. Players in supply chains want to use modern digital networks to transform traditional processes and integrate financing and risk hedging into digital, fast, and transparent processes. Credit granting is part of such processes.

Credit granting is found with corporates, banks, and financial institutions and requires sufficient up-to-date data in credit risk assessment and credit limit decisions. Data inventories that provide indications of default risks are therefore of paramount importance. Nevertheless, collaboration of the best data service providers are the foundation for a successful credit risk based automated straight through process for credit limit decisions and risk monitoring. Claims to use big data and modern methods of artificial intelligence and machine learning as well as data analytics often cannot be met adequately with only their own data and methods.

A digital transformation is therefore not only relevant to internal technical solutions for the improvement of in-house processes, but also in cooperation with business partners like credit rating agencies, trade credit insurances and ECAs. Sophisticated measurements of default risks and risk hedging with trade credit insurances and ECAs reduce potential defaults. The procedure of cooperation with these business partners can lead to a higher benefit than the generation of results from the respective developments of non-experts.

Digital and automated processes relieve people in credit risk management of tedious and time-consuming routine work, which a machine can do very well. This relief gives our specialists in risk analysis and decision-making processes more time to make better use of their skills. The IT support leads to a modern implementation of management by exception in risk analysis and credit limit decisions.

Integrated processes

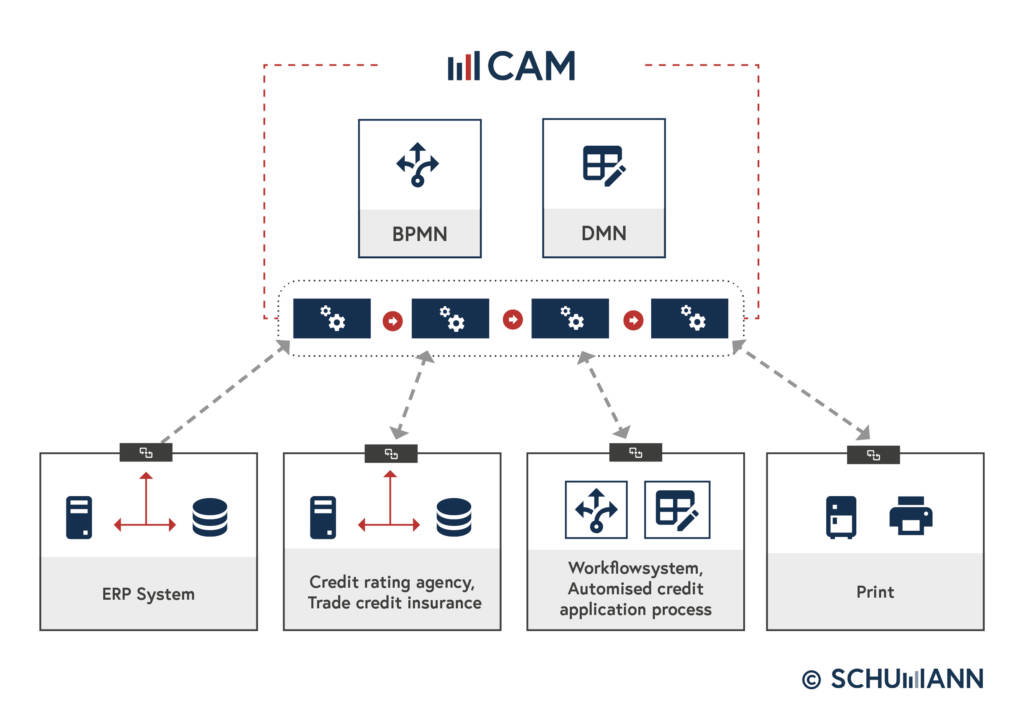

IT solutions for credit risk management and credit limit decisions should enable process integration with data providers.

The need to implement fast and integrated processes requires a modern implementation of enterprise integration layer connections to internal administration systems as well as application programming interfaces (APIs) to business partners. Process chains are controlled and interlinked on the basis of triggers and parameters. A deep understanding of the processes by all business partners is a crucial prerequisite for superior processes with excellent results.

A technically supported straight-through process in banks and financial institutions begins with the customer e.g. in an online portal. This is where access to credit granting processes is initiated. Onboarding procedures can be streamlined by technically integrating master data checks, KYC (AML/CTF) and fraud protection processes as well as by automatically evaluating credit application data.

Experience shows that standard software solutions with the capability to easily configure and adjust processes according to the credit policy and regulations meet business requirements best. Modern workflow management and flexible decision-making machines (Business Process Model Notation BPMN and Decision Model and Notation DMN engines) support superior systems of market leaders. Especially in times of crisis, it is important to adjust own credit risk policy and immediately set up the processes accordingly.

Data analytics

Data analytics require sufficient data sources for specific workflows and decisions. Own databases, such as results of the financial data analysis or payment experiences related to credit customers, as well as data from credit rating agencies and trade credit insurances must be made available automatically at the time of the required use. API gateway technologies can allocate access to the best data source.

Artificial Intelligence is used by data providers such as credit rating agencies and trade credit insurances but also by other sources for KYC (AML/CTF) or fraud detection. The users of credit risk management solutions and credit limit decision machines can directly use the valuable information from these partners. In addition, scientific scoring methods can be applied for data analysis on own databases related to customers, such as payment experiences, balance sheet analysis, liquidity forecasts, and portfolio risk analysis to complete comprehensive analytics.

Best possible technical process integration of credit risk analysis and hedging through insurance requires a deep knowledge of scoring and AI methods for determining rating values and default probabilities of data suppliers. Credit rating agencies and credit insurers/ECA in particular have a large amount of relevant data at their disposal, which is a necessary prerequisite for the scientifically correct methods used. The combination of the analysis results with the data analyses of corporates, banks, and financial institutions allows clear distinctions to be made between buyers with strong credit ratings and those at risk of default or insolvency.

“Business partners will become closer through digital connections and process chain integration with partner systems”

In export financing, SCHUMANN has unique financial data analysis procedures recognised by credit insurers/ECAs such as Euler Hermes, which are used to support financing decisions. These are particularly advantageous in portal solutions for export credit financing, as processes can be handled digitally, faster and with their quality assured.

Scalability of Global Trade Finance

The potential of the straight-through processes in supply chains is evident from a scalability of the business perspective. IT-supported processes and automation allows fast limit decisions which are both compliant with rules, and reliable. Therefore, workflow and decision engines and IT-supported approval processes can be used to gain market leadership. Entering new market segments, such as SME, require particularly automated and efficient processes to ensure best customer experiences with low costs for each risk and limit decision.

Consequently, business partners will become closer through digital connections and process chain integration with partner systems. Business volumes can be controlled much better in digital and automated business partner networks, independent of time and personnel restrictions. In the international export business digital platforms support the transparency of process steps for each partner in the supply chain, financing, and risk hedging, e.g. through ECA.

The future assessment is that technological business partner networks with digital connectivity and portal technology are the key driver of growth in global trade. Standardisation initiatives such as the ICC Digital Trade Standards Initiative (DSI) will facilitate technical interoperability in business partner networks and portals and therefore lead in the same direction of supporting innovative digitalisation for global business.