Estimated reading time: 5 minutes

King Dollar

The COVID-19 pandemic caused global central banks to take emergency action to support the world’s economies; one such measure was the rapid cut in interest rates to record lows.

With the recovery well underway and, pandemic-era lockdowns soon ending, inflation began to rise. In April of 2021, headline Consumer Price Inflation (CPI) in the United States jumped from just above the Fed’s 2% target to 4.2%, a more-than 12-year high!

But just before this spike, inflation in the US caused Fed Chair Jerome Powell to seek to calm markets and the public by famously describing inflation as “transitory,” a moniker that was subsequently dropped by year-end as it was clear that inflation was, in fact, entrenched.

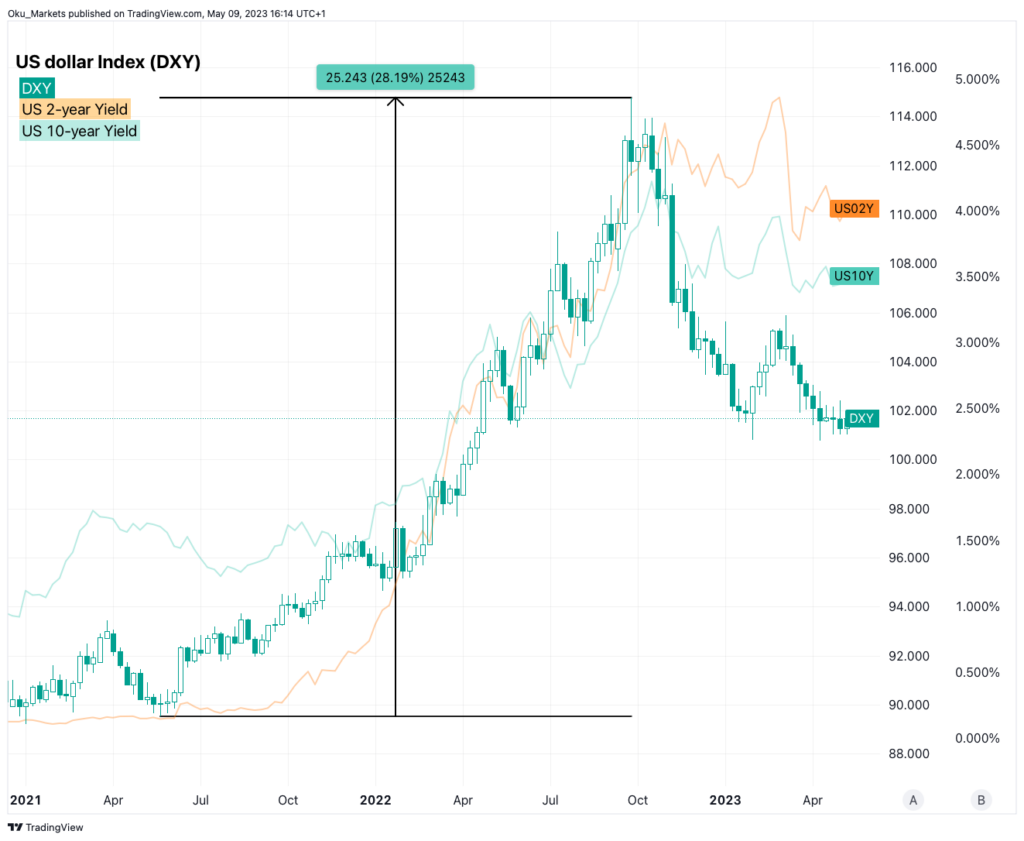

At this time, the US dollar was trading close to the bottom of the six-year trading range, which was about the average valuation across the prior twenty years; a period that took in the 2000 dot-com bubble, the 2008 global financial crisis, and the pandemic!

In mid-June 2021, when the Fed indicated the possibility of raising interest rates by 2023, the dollar started to appreciate in anticipation of potential future rate hikes. Additionally, US government bonds experienced an increase in value across the maturity curve.

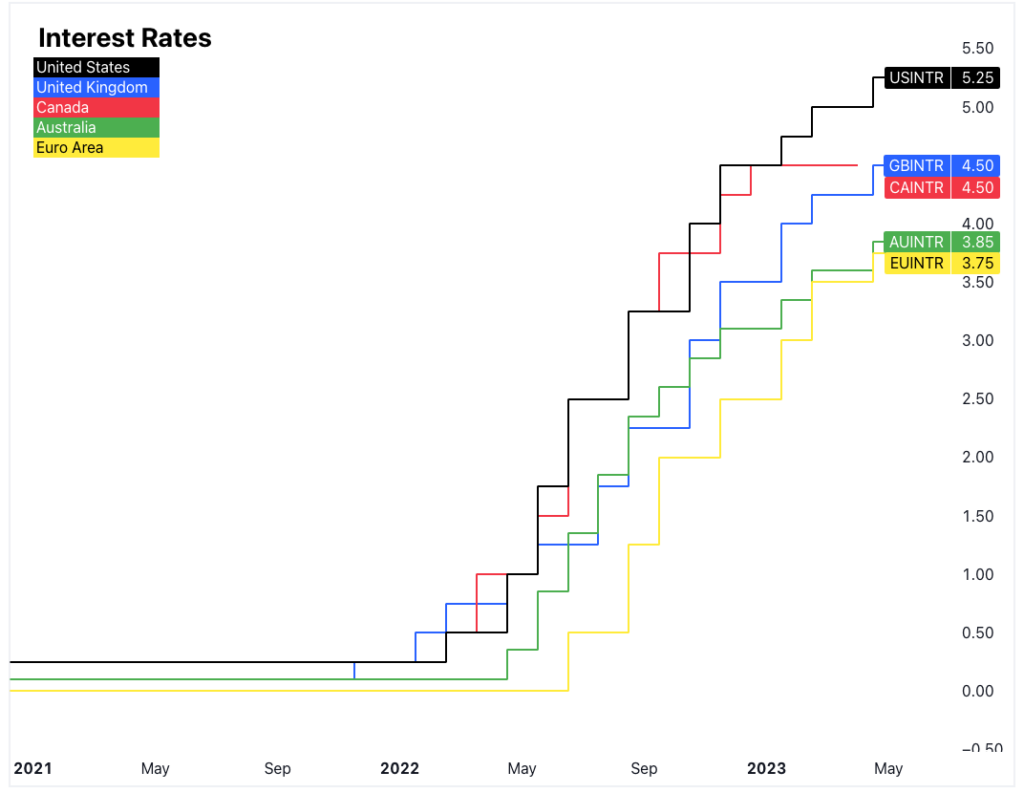

The Fed wasn’t the first major central bank to lift rates: the Bank of England (BoE) takes that crown, following hikes from Norway, New Zealand, and a few others. The Fed went aggressive, hiking in March 2022 by 25 basis points and then lifting by increments of 50 and 75 basis points until a slowdown in early 2023.

In February of 2022, Russia invaded Ukraine, causing a flight to safety in financial markets. The dollar was the primary beneficiary, gaining several per cent against most currencies. This uncertain geopolitical backdrop coupled with the Fed’s aggressive monetary tightening cycle pushed the dollar higher as far as its peak in late September 2022 after an impressive 28% increase when measured against a basket of currencies (the “DXY” US dollar Index).

Exporter advantage

The almost straight-line appreciation of the dollar against the British pound and the euro was a boon for those exporting to the US, or other countries and markets operating in US dollars. From Q3 of 2021, the euro fell against the dollar for five consecutive quarters; the pound experienced a similar fate, bar one period of very modest gains in Q4 2021, largely thanks to the BoE’s rate hike and the better-than-expected pathway through the latest COVID variant.

With each passing month of local currency declines and dollar gains, exported products became more attractive to overseas customers and, margins increased. Remember we saw a significant rush for overseas investors purchasing properties in the UK and Europe thanks to the dollar’s strength!

Peak dollar: is the party over?

The dollar certainly peaked in late 2022 and, has been losing value every month except February, when the Fed spooked markets with strong hawkish rhetoric that was ultimately dismissed by March. The dollar’s rise took the DXY up by $25, the pound down by more than 21%, or $0.30 (if we ignore the Liz Truss mini-budget calamity and associated plunge to record lows), and the euro down by about 20%, or $0.24.

The reversal of the dollar’s gains has thus far caused the pound to regain about $0.14, and the euro to erase about $0.12 of prior losses. Both the pound and euro have recovered by around 50% from the 2021-onward slide, which we know was inspired mostly by the Fed’s (more) aggressive interest rate hikes, plus the safe-haven demand for the dollar.

The May meeting of the US Federal Open Market Committee brought US interest rates to 5.25% and, many investors believe that the Fed will now hold rates before making an eventual cut. Of course, nobody truly knows – even the Fed policymakers, who are reacting to incoming data – but, if inflation in the US continues to ease – as we saw in the data released on 10 May –, there is a strong likelihood that the Fed is nearly done, if not already. This will very likely lead to further losses for the dollar.

Exporters be warned

Business is never easy and, whilst I’m sure that exporters haven’t been making money hand-over-fist because of a strong dollar, I’m positive it’s helped to a greater or lesser extent for most.

With stubbornly high inflation in the United Kingdom and sticky underlying inflation in Europe, the outlook for interest rates on this side of the Atlantic is more hawkish than in the US.

Diverging monetary policy drives exchange rates hard and, there is a real possibility that we could see further losses for the dollar, perhaps sending GBPUSD as high as $1.30 and EURUSD to or above $1.20 across the next 12 months.

The latest interest rate from the Bank of England came on 11 May and, the Monetary Policy Committee lifted Bank Rate for the twelfth straight meeting, adding a quarter-point (25bps) and taking rates to 4.5%. The BoE stressed that further interest rate rises could be required to curb inflation and, they upgraded their GDP forecasts, erasing a prior prediction of recession this year. The good news on economic output projections coupled with a hawkish BoE are arguably bullish for the pound.

Anybody that reads my daily or weekly FX newsletters will know that I urge caution and advise strongly against using FX forecasts for any decision-making. FX forecasts are famously inaccurate and, exchange rates are affected by an extensive array of factors. Understanding the changing dynamics and being aware of the possibility that the trend could continue should inform and support better decision-making by business leaders.

Exporting businesses should look at the pricing structure of long-term contracts, renewals, and business in tender. Stress-testing financial performance and risk management strategies against a weaker dollar is a straightforward way to assess the impact of a continued slide in the dollar’s value and, firms should look to review budgets in light of potential further dollar losses.

A qualified and experienced currency risk consultant will be able to review the performance of a firm’s FX risk management strategy and, make considered recommendations for managing exchange rate risk effectively in a trending market.