Over the last few years, the global payment landscape has changed radically.

With the use of cash in decline, and combined with increased knowledge of and confidence in digital payments, customers have changed their relationships with banks, and have increasingly turned to new market players.

The turbulence of the COVID-19 pandemic has further highlighted that the future lies in digital innovation, and in partnerships between newcomers and incumbent players.

Together, these will enable new cost-efficient business models. In this scenario, open banking not only represents an agent of change, but a “win-win” scenario for all.

A backdrop to innovation

In a period of blurred industry lines, the rise of disruptive innovations in financial services has required that regulators introduce legislative frameworks governing the secure development of these innovations.

Accordingly, the European Union (EU) has adopted the Directive 2015/2366 – also known as Payment Service Directive 2 (PSD2).

PSD2 encourages innovation, removes fragmentation, improves risk management, and ensures a “level playing field” through a Common European Data Space.

Simultaneously, in order to remain competitive against fintechs and Big Tech, banks have therefore needed to review their traditional business models and offerings, and transition towards new digital value-added services (VAS) that enable enhanced banking functionality and operations.

CBI, a public limited consortium company that comprises approximately 400 payment service providers (PSPs) – including shareholders and customers – has been providing value-added services to the banking sector for the last 20 years.

As such, CBI is considered a facilitator of change within the banking sector, enabling communications and operations between banks, corporates, citizens, and public administration.

This has been achieved through the establishment of collaborative ecosystems that comprise IT architectures, innovative functionalities, and common implementation guidelines to promote business potential and interoperability.

CBI, PwC findings

In 2021, in its role as a standard setter and facilitator of change, CBI partnered with PwC to publish the Global Open Banking Report.

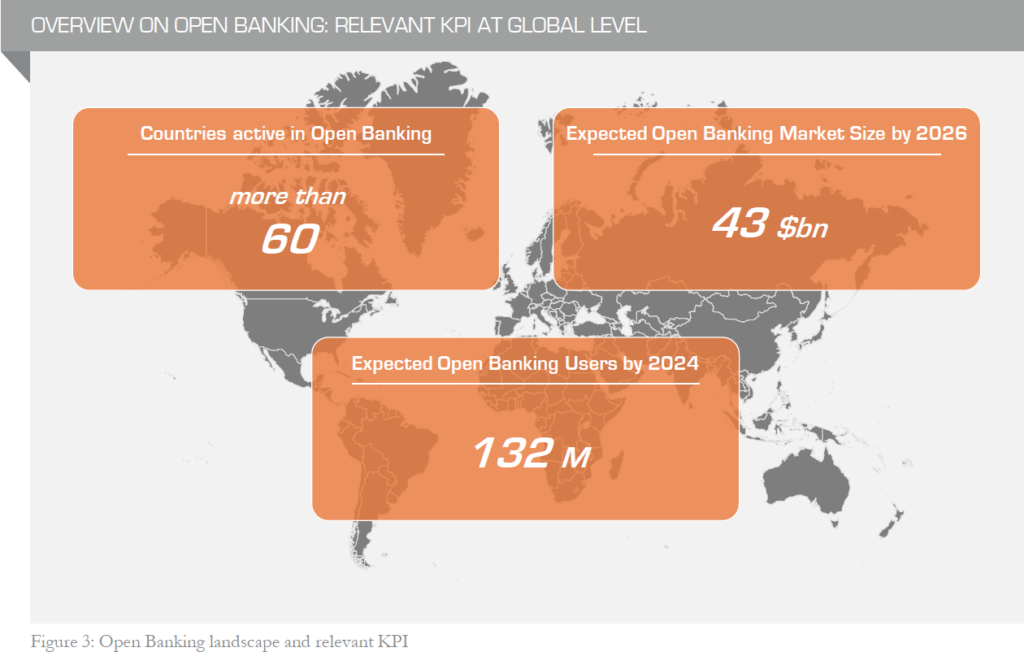

The report emphasises the growing importance of open banking, as currently adopted by approximately 60 countries, through either prescriptive, facilitative, or market-driven approaches.

The variety of such approaches depends on market location and, in some cases, on the absence of a defined regulatory framework.

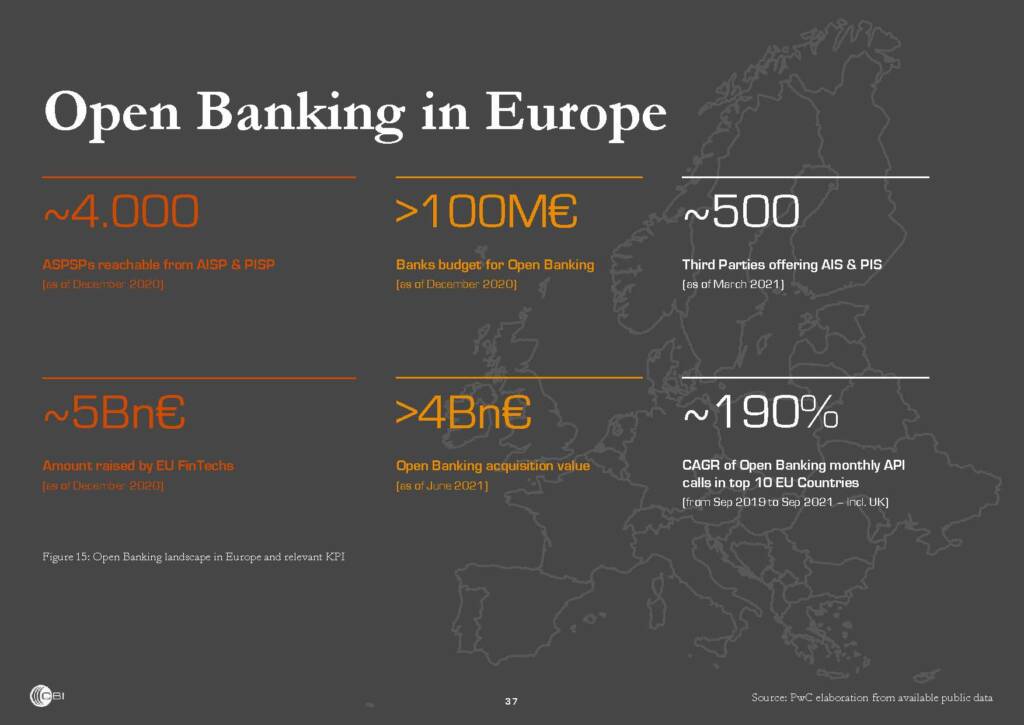

The same report highlights how, since 2019 – and as a consequence of the adoption of PSD2 – the number of third-party providers offering account information and payment initiation services in Europe (approximately 500) has risen by 300%.

Over the same period, we have also seen exponential growth (to almost 4,000) in the number of accounting servicing payment service providers (ASPSP).

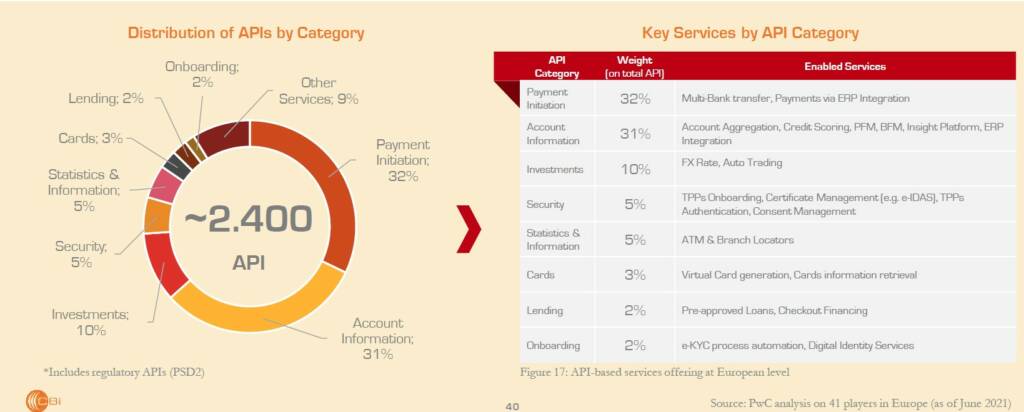

Moreover, a closer analysis of 41 market players reveals that 63% of the 2,400 total APIs rely on PSD2 data relating to account information (AIS) and payment initiation (PIS).

To a lesser extent (14%), services based on investment, loan, or insurance data are also beginning to emerge.

These results demonstrate how open banking is simultaneously opening doors to new market players, while stimulating competition in financial services and enriching bank offerings to customers.

Open banking: The view from Italy

After conducting a survey of Italian banks, CBI and PwC have found that the adoption of open banking services in Italy remains slower and lower than in other European areas (e.g. the Nordic countries).

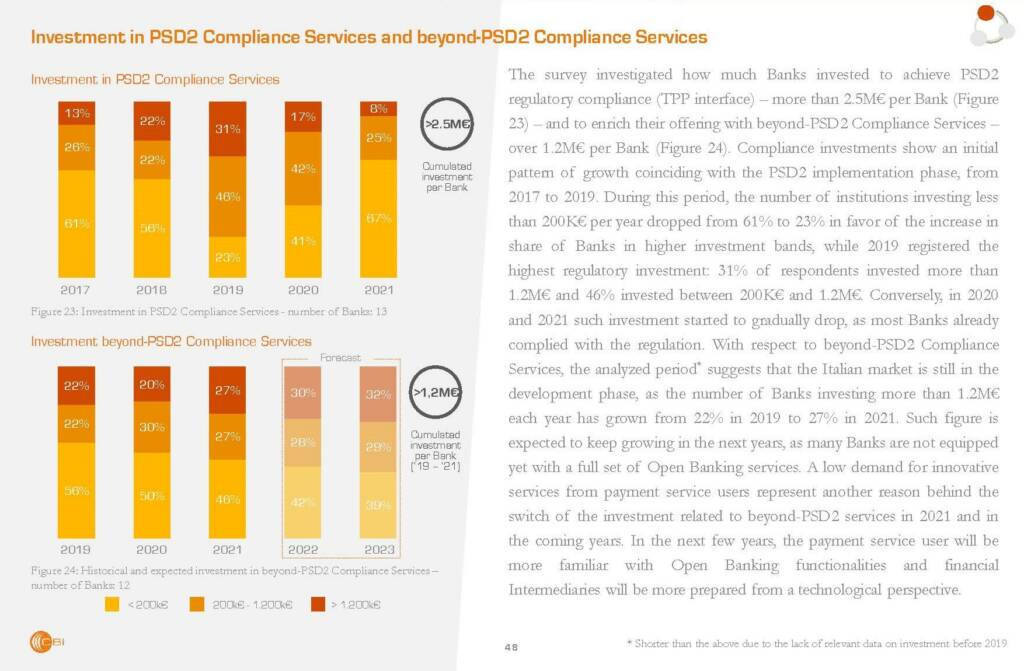

Over the last five years, despite significant investment to comply with PSD2 (over €2.5 million on average), the position of Italian banks has stood in sharp contrast to a growing number of financial institutions.

Over the last two years, for example, more than one in four financial institutions has invested in commercial open banking services (rising from 22% in 2019 to 27% in 2021).

Furthermore, the areas in which open banking services in national banks are currently concentrated, and the focus on development of future VAS, demonstrate that national banks have not yet captured the full potential of digitalisation, or its contribution to sustainable economic growth and value creation.

To this end, current open banking propositions and forecasts in the national context remain: account aggregation (55%), Check IBAN (45%), personal financial management (36%), instant payment (27%), and identity and digital onboarding services (18%).

Going forward, banks have identified the following VAS areas of strategic development: digital ID and onboarding services (64%) and Check IBAN (55%).

Through a collaborative ecosystem comprising innovative business models, established standards and IT infrastructure, CBI has effectively enabled banks to advance into a “network economy”.

In this economy, VAS stem from an increased number of interconnected users, and augmented functionality and interoperability among diverse sectors, which together deliver sustainability and circularity in an increasingly transactional economy.

CBI initiatives

A recent and significant step in fostering innovation in the banking sector is CBI Globe, which was launched in 2019.

This is an open banking ecosystem based on an API gateway that supports 80% of the domestic banking community (about 300 Banks in Italy) in achieving compliance with the revised PSD2.

In this regard, data on CBI Globe operativity registers overall 200 million API calls, enabling the business for approximately 180 third-party providers.

To further expand its scope, CBI has subsequently developed a new functionality allowing member PSPs to act as third-party providers, in addition to a range of innovative value-added open banking products.

These will simultaneously foster digitalisation and efficiency for both public administration and corporate customers (e.g. Check IBAN functionality), while enhancing shareholders’ competitiveness (e.g. through Smart Onboarding).

These steps have broken down technical barriers, allowing banks and PSPs to expand their traditional services and act as account information service providers (AISPs) and payment initiation service providers (PISP).

Both AISPs and PISPs can then interface with centralised third-party provider enablers, thereby reaching the entire Italian banking ecosystem and numerous international gateways.

CBI’s pioneering role in Italian open banking

As you can see, CBI retains a diverse range of coexisting roles and functions in open banking and open finance in Italy.

From standard setter to enabler of industry change, facilitator, and developer of collaborative open platforms, CBI is a focal point innovation in the Italian market.

Through banks’ newfound confidence in digitalisation – which goes beyond the “compliance phase” – CBI intends to leverage its expertise in promoting active innovation within banks and other financial intermediaries.

This can increase functionality and interoperability internationally, and will allow CBI to benefit from the ceaseless advantages that derive from the “network economy”.

To this end, CBI is developing a range of new and enhanced VAS, including:

- Check IBAN Cross-Border – Enabling verification of the validity of an IBAN, including ownership of IBAN in relation to a specific end-user identified in association with a fiscal or VAT code globally.

- Request-to-Pay XML CBI – Through specific operating rules, this allows creditors to claim funds from debtors for specific transactions via CBI network.

- Smart Onboarding – Enabling corporates to retrieve real-time banking and personal data related to end-users wishing to onboard a specific service offered by their company through the security of Strong Customer Authentication.

Other services currently in development or being enhanced to support open banking are Name Check, Invoice Financing Database, and Buy-Now-Pay-Later (BNPL).

Moreover, CBI has also entered into new partnerships in the field of open finance, which are aimed at supporting the financial ecosystem to act as an API Marketplace.

Realising the unfulfilled potential of open banking, CBI’s strategic direction remains that of investing in integrated and sustainable technological innovation and digital skills, which will further accelerate the transition of banks into true transaction operators.

Banks will then be fully equipped to respond more effectively to the new challenges of a continuously evolving transactional market, while creating sustainable value for customers.