Estimated reading time: 8 minutes

In the third quarter of 2021, Egypt’s import bill increased by 34% compared with the same period a year earlier, and the country’s current account deficit widened.

Egypt currently enjoys sufficient foreign exchange reserves. However, the Egyptian authorities are taking various steps to limit the impact of global events on the country’s economic performance.

These global events include the increase in commodity prices and escalating conflict between Ukraine and Russia, which will impact food imports.

The measures taken by the Egyptian government aim to control the importation of goods, protect local industries, restrict the importation of poor quality and low standard products, and reduce foreign currency spending.

In addition, this month, the Egyptian government activated the pre-registration of shipments to control import operations through the National Single Window for Foreign Trade Facilitation (Nafeza), its new customs facilitation platform.

Nafeza operates in accordance with international standards on trade-related procedures and customs requirements for the clearance of goods, thereby converting Egypt into “One Logistical Area”.

Central Bank of Egypt announces new rules for importers

On February 13 this year, the Central Bank of Egypt (CBE) announced that Egyptian banks will no longer accept documentary collections to finance imports. Instead, importers will be required to open letters of credit to import goods.

The CBE added that Egyptian banks can only accept documentary collections for goods already shipped before February 22, 2022.

The CBE decision provided exemptions for specific activities and commodities from the requirement of opening letters of credits for import operations, including the following:

- Intragroup sales (sales between the branches and subsidiaries of foreign companies and their headquarters) are exempt from the CBE’s new ruling. Therefore, banks are authorised to accept documentary collections for these transactions.

- Imports of goods worth up to $5,000 (or the equivalent in any other foreign currency) will be exempt from the requirement to open letters of credit.

Shipments delivered via express post are exempted from the requirement of opening letters of credit. - The CBE exempted imports of medicines, vaccines, and the active ingredients required to manufacture them locally. Furthermore, imports of strategic and essential commodities – including tea, meat and poultry products, fish, wheat, oil, milk powder, baby formula, fava beans, lentils, butter, and corn – are not subject to the new requirements.

The main differences between documentary collections and letters of credit in international trade

To understand the implications of the CBE’s new import rules on foreign trade operations, one should understand the main differences between letters of credit and documentary collections as payment methods in international trade.

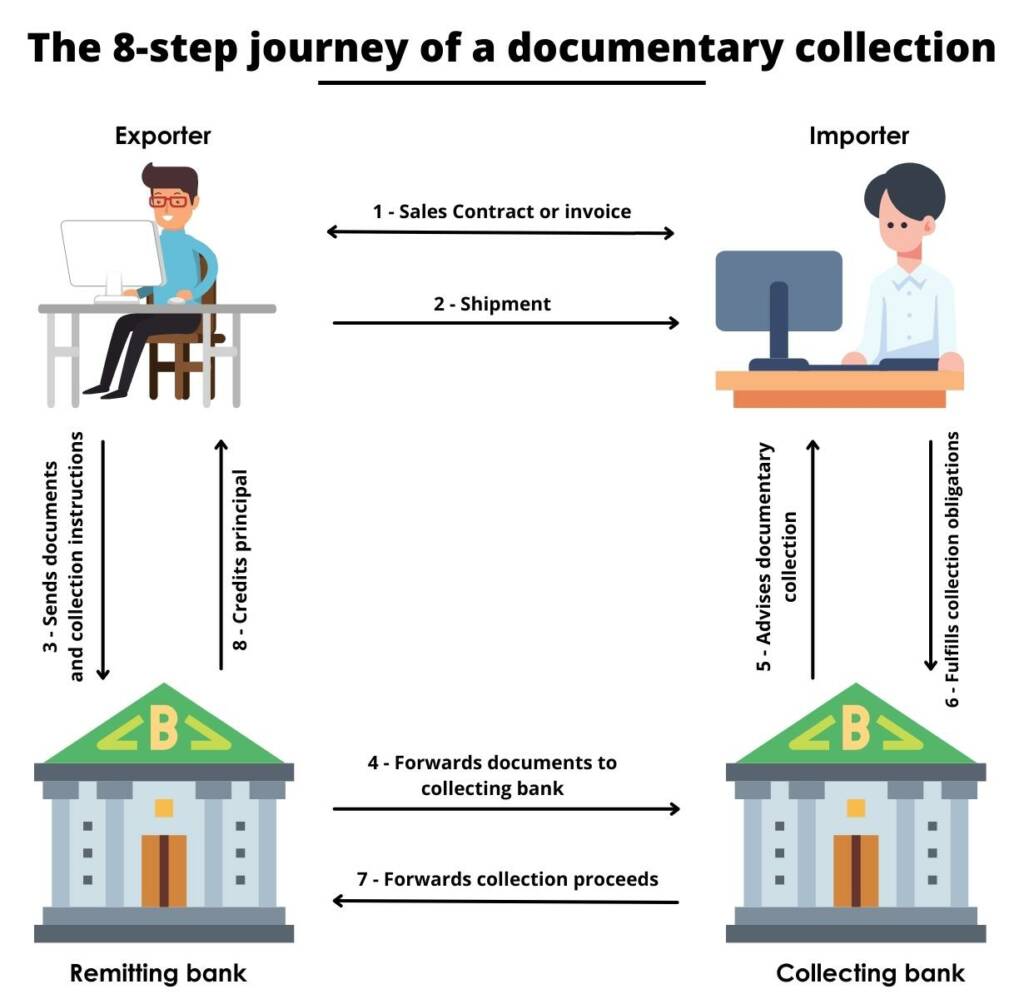

A documentary collection is a trade finance tool in which an exporter’s bank forwards documents to an importer’s bank and collects payment for the shipped goods.

Under documentary collections, importers typically pay for the goods after the shipment of the goods.

But it is also possible to make a partial advance payment under documentary collections. Figure (1) shows a simple presentation of a documentary collection.

A documentary collection is usually issued following an exporter’s request from his bank, known as the exporter’s bank or the remitting bank.

The exporter gives the bank instructions to forward trade-related documents to the importer’s bank.

The exporter’s bank then forwards these documents to the importer’s bank, requesting them to deliver them against payment.

The importer bank – also known as the collecting bank – informs the importer about the documents and hands them to the importer upon receipt of the dues.

Two payment options are available under the documentary collections: Documents Against Payment (D/P) and Documents Against Acceptance (D/A).

Once the importer’s bank has been paid, or the importer has accepted a time draft, the bank releases the documents to the importer. The importer then uses the documents to collect the merchandise.

Figure (1): Documentary collection in international trade

The position of banks in the documentary collection is limited, since they do not check the documents or guarantee payment.

Moreover, the bank does not cover credit or country risk under documentary collections.

If the importer and exporter have a good relationship, and if there is great confidence that there will not be any breach of trust, documentary collections are considered a more convenient and cheaper option than letters of credit.

Letter of credit process

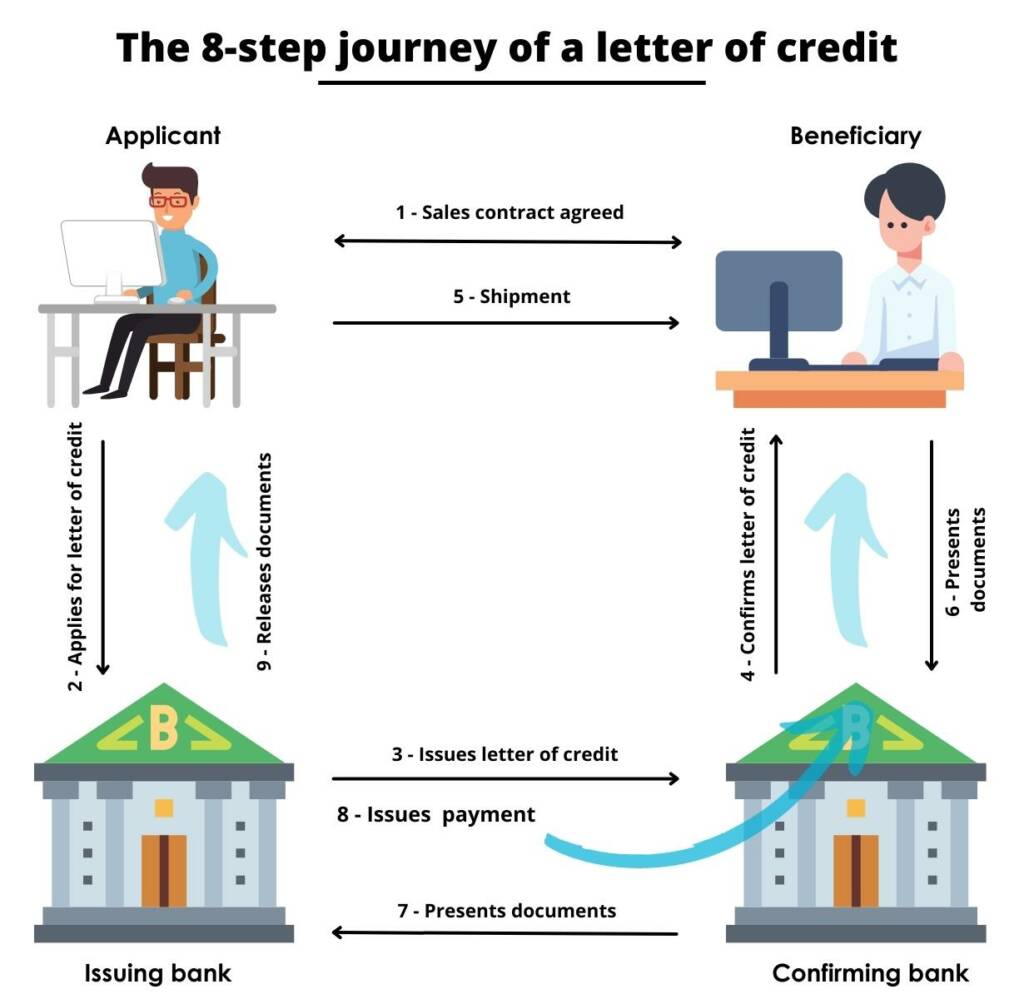

A letter of credit is a document issued by the importer’s bank that guarantees the exporter will receive payment on time and for the correct amount if the exporter presents documents that comply with the terms of the letter of credit.

Figure (2) shows a simple presentation on how letters of credit work in international trade.

First, the importer applies to their bank to open a letter of credit in favour of the exporter.

Then, the importer’s bank drafts the letter of credit using the sales agreement terms and conditions, and transmits it to the exporter’s bank to communicate it to the exporter.

In turn, the exporter ships the goods in the manner provided for in the letter of credit and submits the required documents to their bank.

Banks usually review presented documents to ensure they comply with the letter of credit terms before approving payment.

If any of the documents presented under the letter of credit contain the slightest error or omission, the importer bank may refuse to make payment.

Thus, to avoid payment delays and extra fees, the documents required by a letter of credit should be prepared by trained professionals.

Figure (2): Letters of credit use in international trade

The importer’s bank usually seeks collateral from the importer in the form of pledged securities or cash in exchange for issuing a letter of credit.

Letters of credit generally provide a higher level of security in international transactions, as the responsibility of remitting payment to the exporter lies with the importer’s bank.

Bankers charge the importer high fees for issuing a letter of credit. The charges often reflect the amount of risk the bank assumes in relation to the transaction.

Letters of credit are more useful when the importer’s country is in a state of political or economic instability and has controls on foreign exchange availability.

Letters of credit are also recommended for use in higher-risk situations, when the importer’s credit is unacceptable, when dealing with a new or less-established trade relationship, or when extended payment terms are requested.

Table (1): Summary of the main differences between documentary collections and letters of credit

| Parameter of comparison | Documentary collections | Letters of credit |

| Instructing party | Exporter | Importer |

| Issuing bank | Exporter’s bank | Importer’s bank |

| Examination of documents | Banks do not check or examine documents. | Banks examine the presented documents and may reject payments if the documents are not complying with the letter of credit terms. |

| Issuing bank obligations | Banks do not guarantee payment to the exporter in case of default by the importer. | Banks undertake to pay the export if the documents presented comply with the letter of credit terms. |

| Preferable usage | Preferred when the exporter and importer have a good relationship, and there is great confidence that there will be no breach of trust. | Preferred when the reliability of the contracting parties cannot be readily and easily determined. |

| Requirement for collateral or cash cover | Not required by banks. | Banks typically require a pledge of securities or cash as collateral for issuing a letter of credit. |

| Charges Incurred | The charges incurred for the exporter are generally low compared to letters of credit costs. | The charges incurred for the importer by the issuing bank are generally high and measured as a percentage of the letter of credit amount. |

| Level of security | Provides a relatively low level of security as banks do not guarantee payment to the exporter. | Provides a high level of security in international trade as letters of credit help exporters minimise the importer’s credit and country risks. |

Impact of the new import rules on the Egyptian business community and banking sector

Trade and industry organisations in Egypt have raised objections to the CBE’s new import rules.

The Egyptian trade lobbies believe that new CBE import rules will drive up costs for several industries, negatively impact the country’s economic activity, and will cause difficulties for traders.

In addition, traders indicated that the new CBE rules will prevent them from benefiting from their well-established relationships with foreign exporters, which enabled them to import commodities at a relatively low cost and suitable payment terms through documentary collections.

Under documentary collection, importers usually receive the shipment documents once they pay the value of the goods or accept a draft.

However, under a letter of credit, the importer will have to wait for about one month on average to receive the shipment documents.

This will lead to a longer working capital cycle, which may negatively impact the importer’s profitability and return on investment.

Business groups and traders have further indicated that the new import regulations will harm the competitiveness of the Egyptian exports, worsen the effect of the global supply crisis, and raise production costs, which could increase the prices of goods in the local market.

Additionally, the difficulties facing SMEs in obtaining finance to open letters of credit could lead to some of them having to exit the market.

In response, the Egyptian authorities have encouraged business entities to comply with the new requirements and not to create further instability by resisting them.

The CBE has instructed Egyptian banks to support companies involved in commodities importation by:

- Lowering the fees of issuing letters of credit to match those of documentary collections for each client.

- Raising credit limits for existing customers and setting limits for new customers depending on their previous import volumes through documentary collections.

- Executing customers’ requests to open letters of credit to all customers as quickly as possible.

Based on the above initiatives, Egyptian banks are required to establish necessary credit lines and SWIFT relationship management application (RMA) with more correspondent banks worldwide, to satisfy the increasing demand for issuing letters of credit by importers in different regions.

Furthermore, Egyptian banks may currently suffer a lack of professionally trained staff to execute the growing number of letters of credit that clients will need in reaction to the new import rules, and this could pose challenges for trading business going forward.