The International Chamber of Commerce’s (ICC) 11th annual Global Survey on Trade Finance reveals that despite banks being optimistic about the evolving nature of trade finance, the industry-wide challenges and disruption as a result of the COVID-19 pandemic push trade and trade finance into a state of global uncertainty. Trade Finance Global are proud media partners of this year’s Global Survey. Here are the key findings and what this means for the near- to mid-term.

Listen to this podcast on Spotify, Apple Podcasts, Podbean, Podtail, ListenNotes, TuneIn, PodChaser

Of the 346 respondents in 86 countries, the Global Survey, conducted by the ICC, included insights on current trends shaping trade finance, as well as a supplementary COVID-19 Survey, issued a few weeks into the pandemic.

7 Key findings of the Global Survey and the COVID-19 Survey

1. Trade is here to stay… (but not as we thought)

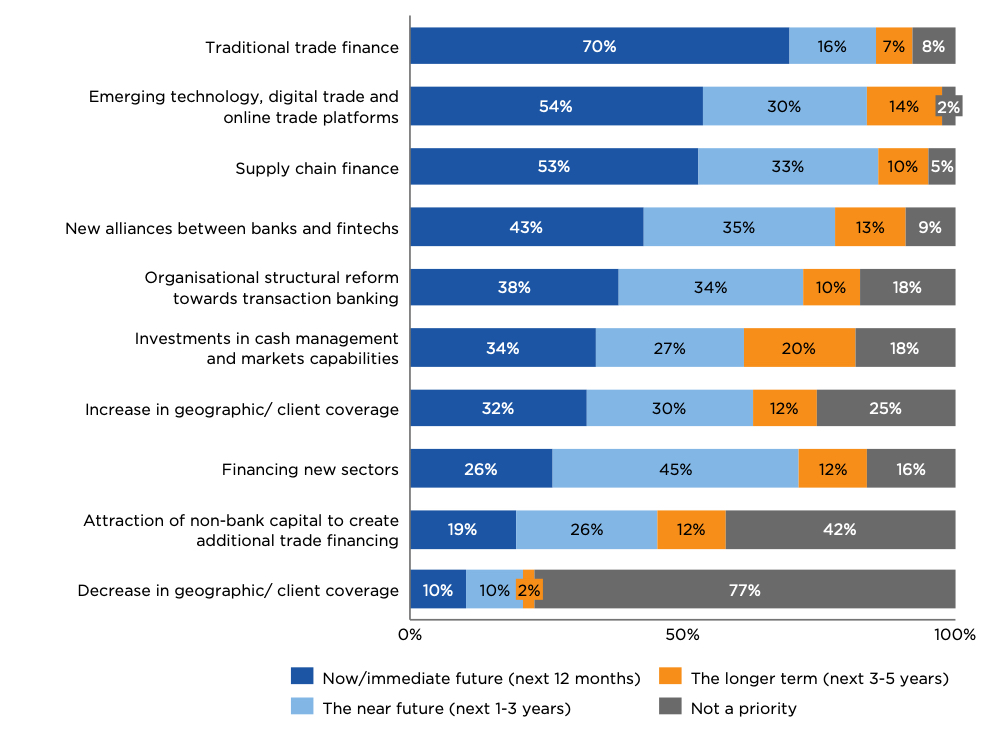

Banks around the world are looking to expand their trade finance business – this includes traditional trade finance (TTF) and the various techniques of supply chain finance (SCF) – through various means, including gaining new clients, offering new products, expanding geographically, and increasing digital offerings. In particular, 86% of respondents said that supply chain finance was either an immediate or near-future priority, while 84% answered the same for digital.

Please indicate what you consider to be the priority areas of development and strategic focus for your bank

Chart 1: Please indicate what you consider to be the priority areas of development and strategic focus for your bank. Source: ICC Global Survey on Trade Finance 2020

However, concern persists about regulatory and compliance-related obstacles to growing trade finance businesses. These include anti-money laundering (AML) and Know Your Customer (KYC) requirements, and the challenges arising from requirements linked to countering the financing of terrorism (CFT), as well as those related to international sanction regulations.

Industry practitioners and leaders fully support the policy and regulatory objectives, as well as the overarching need to protect the global financial system from abuse. The issues flagged, however, relate to consequences of regulation that are believed to be unintended, and that directly affect access to trade financing – thus inevitably curtailing trade and impacting economic inclusion and international development.

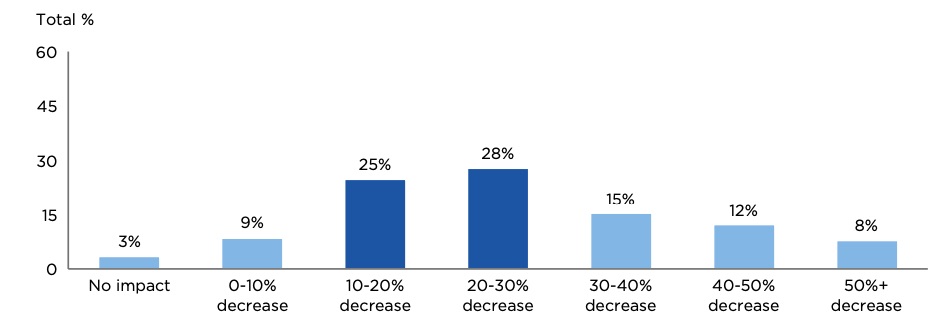

2. Banks are forecasting up to 30% decrease in trade and trade finance due to the COVID-19

Banks from all geographies are already noticing the impact of COVID-19 on

trade flows, with most reporting a 0-10% decrease in Q1 2020. Banks expect an even more significant decline in trade flows for the full year, with the majority expecting at least a 20–30% decline from original forecasts, which broadly aligns with both WTO and BCG scenarios.

What does your bank anticipate to be the COVID-19 impact on 2020 trade flows?

Encouragingly, the majority of banks are helping their customers who have been affected by COVID-19, using various measures including extending financing terms and providing more convenient digital (or partly digital) solutions. Some banks have also relaxed their internal policies on original documentation rules, which hopefully is a sign of things to come as the current crisis catalyses and accelerates a significant reduction (perhaps ultimately the elimination) of paper in trade and trade finance transactions. Leading trade banks have come together under the auspices of the Banking Commission Digitalisation Working Group to issue a paper sharing practices adopted in order to enable trade to flow despite pandemic-related difficulties in accessing hard-copies of trade documentation.

Read more: ICC Digitisation Group publishes digital rapid response measures taken by banks under COVID-19

Most banks have not yet seen meaningful support from local authorities to

facilitate ongoing trade on digital terms. Requirements persist for original documentation in trade transactions, perhaps unsurprisingly given the speed with which COVID-19 has transformed the commercial landscape.

The early part of the COVID-19 crisis did not have a systemic impact on the availability of trade financing which, by all reports, remained consistent. However, careful market monitoring by ICC, the WTO, and other key players now suggests emerging system-wide difficulties with USD liquidity, targeted deployment and far tighter controls on trade financing. Deteriorations in credit quality linked to coming bankruptcies are expected to generate a wave of adverse consequences for trade and trade financing. Encouragingly, according to the vast majority of reports, industry standards and practice around the financing of trade have been robust and respected through the crisis to date.

Article: Atradius Exclusive: The Asian insolvency storm – trade credit insurance overview

3. Place your bets on Supply Chain Finance

Trade banks, particularly those serving global customers, are broadly adopting supply chain finance platforms and expect further growth in this space. However, there is an ongoing divide between global and non-global banks, with 64% of global banks offering SCF platforms, compared to just 13% of local banks and 38% of regional banks.

This divide is set to continue: global banks expect significant growth in the next five years from SCF, with one-third expecting over 50% growth. In contrast, the majority of local banks expect only 0–15% growth over the same period, which is notable given clear market trends that continue to reflect growth in open account trade as well as in SCF techniques such as payables finance. This significant difference in expected growth rates may reflect differing views around the evolution of the market, or they may be an illustration of limited appetite, expertise or capacity among local banks to significantly advance their SCF propositions.

Respondents indicate lingering concerns regarding regulation and the ability of smaller banks to enter SCF due to challenges with technology build (e.g. high costs and lack of internal capabilities), although smaller players have overcome these through partnerships and white labelling solutions.

4. Only 67% of banks gave a sustainability strategy, yet the urgency has never been of greater imperative

All banks are increasingly recognising the imperative to develop a sustainability strategy, with 67% of respondents stating that they have one. This urgency has primarily been fuelled by concerns related to reputational risk and by fast-growing client expectations.

There is strong agreement that the environment and climate change should be priorities, with the majority of banks already integrating sustainability risks into credit risk management procedures for clients and conducting sustainability- related due diligence.

There is a clear desire, however, for more formal guidelines for banks in this area, with 84% of respondents saying they would welcome ICC support in providing sustainability guidelines (read here). The nascent state of these matters, coupled with the wide range of levels of progress on sustainability issues across jurisdictions, including among central banks, adds complexity and urgency to efforts to advance a sustainability agenda globally.

Article: Innovative trade financing and risk mitigation can accelerate sustainable development

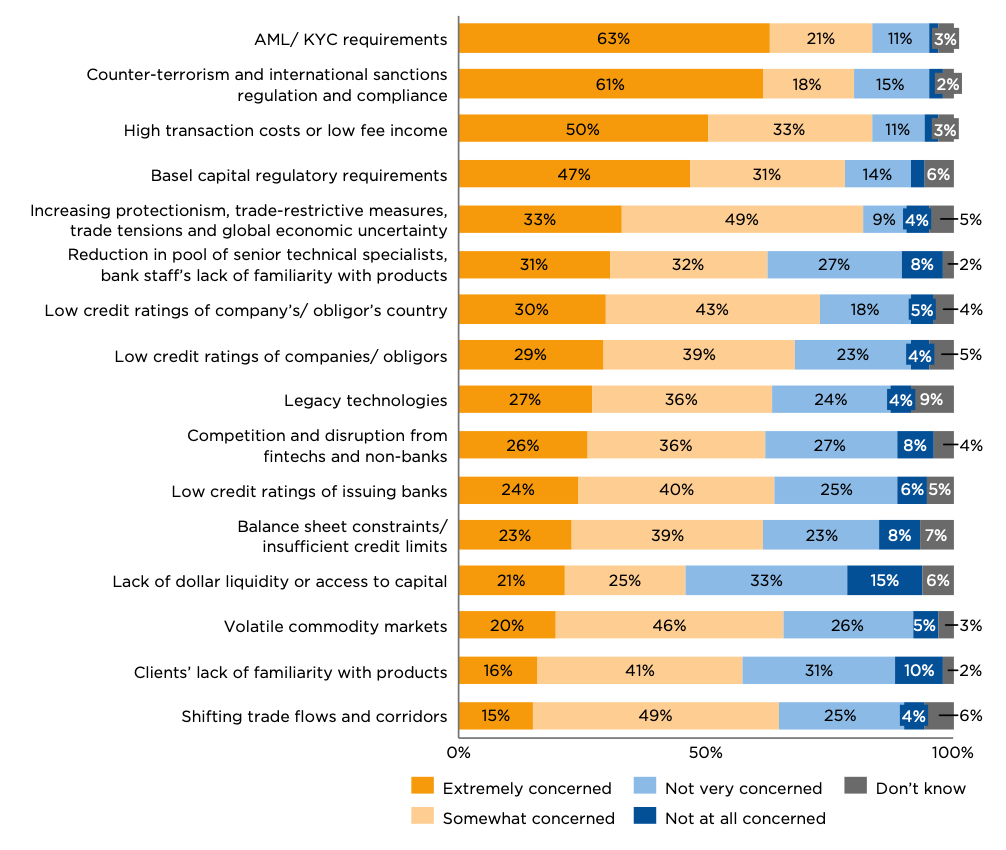

5. Regulation and compliance is still a significant concern

Survey respondents continue to express concern regarding the impacts of existing regulation and compliance policies, with Survey respondents continue to express concern regarding the impacts of existing regulation and compliance policies, with 56% indicating ‘significant concern’ regarding regulatory requirements.

The majority of banks expect customer risk due diligence (including sustainability risks) and increased minimum capital requirements to become areas of increased regulatory focus in the coming years.

Industry stakeholders have reacted positively to the visibility of the BIS

in terms of capital requirements as a short-term response to COVID-19; the imperative to balance regulatory efficacy with the risk-aligned treatment of trade finance continues to be an area of focus.

How concerned is your bank about the following potential obstacles?

Chart 3: How concerned is your bank about the following potential obstacles? Source: ICC Global Survey on Trade Finance 2020

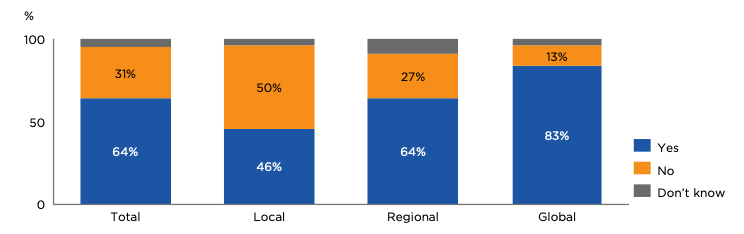

6. The Global / Local Digital Divide (and importance of digitisation)

While digitisation is widely seen as one of the most important trends to shape trade and trade finance in the coming years, there is a clear divide: while 83% of global banks have a digital strategy, only 46% of local banks report having one.

Does your bank have a digital strategy for trade finance?

Chart 4: Does your bank have a digital strategy for trade finance? Source: ICC Global Survey on Trade Finance 2020

This divide exists not only in technology adoption, but also in whether digitisation is considered useful and can reduce costs. While 59% of global banks indicate that digitisation would provide a significant benefit to their operations, just 25% of local and 32% regional banks indicate the same. Furthermore, 90% of global banks expect a reduction in their cost base from the implementation of digital solutions, but only 55% of non- global banks say the same.

The sharp contrast in expected benefits from digitisation between global

banks and regional/ local institutions is instructive, as is the significant difference in benefits expected through cost reduction versus more general, positive business impact. The chasm between global banks and others in recognising a compelling business case tied to digitisation risks driving further consolidation and concentration in trade financing among banks.

Video Interview: ICC SOS – Save Lives. Save Livelihoods. Save Our SMEs

7. The gap widens – financial inclusion

73% of survey respondents feel that there is a shortage in servicing the needs of the global market, and the majority believe that there is a role

for governments and export credit/ multilateral agencies to help close this gap.

Most banks reject only a small percentage of trade finance applications, with 62% rejecting between 0–10% of applications in 2019. Micro, small and medium-sized enterprises (MSMEs), and those from Africa and Central/ Eastern Europe, are disproportionately rejected – consistent with the findings from the previous three editions of the Global Survey. The most common reasons cited for rejection are KYC concerns and low- quality applications.

Digital trade is widely seen as a key enabler to help banks close the trade finance gap, with 55% of survey respondents positioning themselves to service more MSMEs using technology solutions. The challenge is to ensure enough local banks – that often serve these MSMEs – are sufficiently digitally enabled to make it commercially viable to serve the MSME client segment.

To read the full 2020 ICC Global Survey on Trade Finance, please click below.