Saudia Arabia, the world’s second-largest oil producer behind the USA, made headlines this week as reports surfaced that its economy had expanded by 11.8% in the second quarter of 2022, a massive pace largely fueled by high oil prices.

While the country may not produce the most oil, it is able to extract and refine oil much cheaper than the rest of the world. Production costs from Saudi Arabia’s oil fields run at about $2.80 per barrel, compared to the USA’s average production costs of $30-40 per barrel.

For those on the outside looking in, the oil industry can seem very complex and full of price swings, cartels, and political pressure.

To help understand some of what is going on, let’s take a look behind the oil derricks and examine some key cycles that drive decision-making in the industry and the primary factors that impact prices.

Cycles in the oil industry

The oil industry is generally impacted by two predominant cycles:

1) the oil investment and production cycle and

2) the political cycle

Drilling for oil is a complex and costly process with large capital expenditure requirements and long time delays between the initial investment and any significant payoffs.

While the many variations of oil and drilling technology create a wide range of costs and timelines, in general, analysts can expect the oil investment and production cycle to last for a minimum of 8-10 years.

This means that industry decision-makers must rely on a series of long-term – and thus largely unreliable – forecasts.

To add to the uncertainty, oil is also heavily dependent on political cycles, which tend to last 2-4 years for most western nations.

Given that oil production is heavily dependent on the policy decisions laid out by a nation’s political regime, political cycles play a heavy role in the industry. In addition to this, the length of political cycles does not neatly line up with production cycles, creating yet more uncertainty.

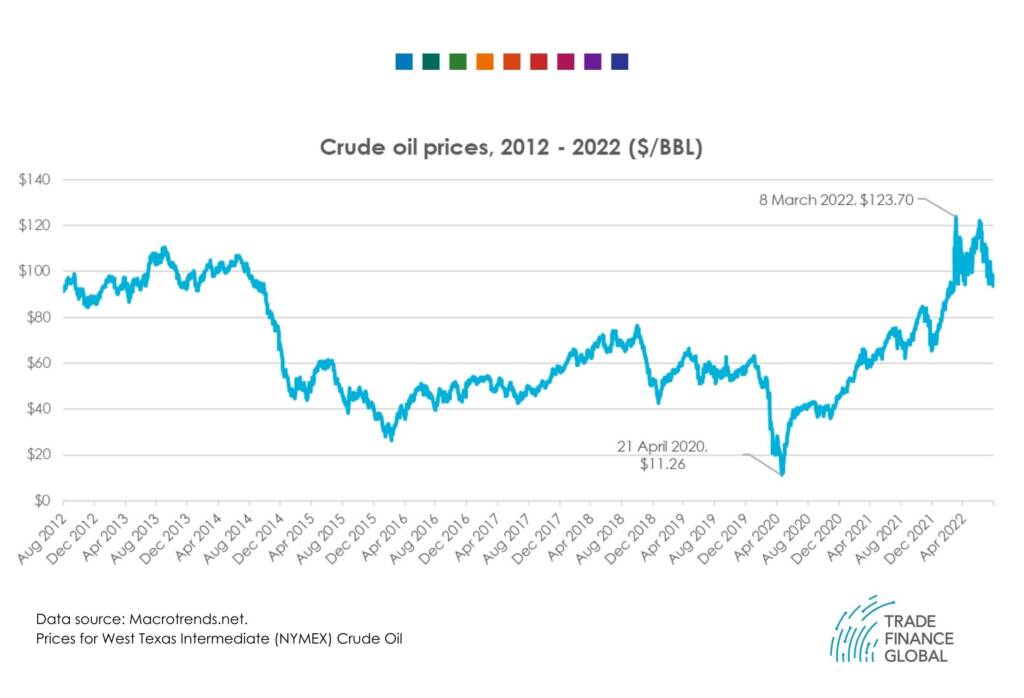

To better illustrate this, imagine a drilling company that established operations in the Canadian tar sands ten years ago in August 2012.

In this company’s relatively short existence, it will have had to adjust to:

- The introduction of a provincial carbon tax imposed by Alberta’s New Democratic Party (NDP) provincial government in 2015

- The introduction of Canada’s federal Greenhouse Gas Pollution Pricing Act (GHGPPA) in 2018 under the Trudeau government

- The repeal of Alberta’s provincial carbon tax under the United Conservative provincial government in 2019

- The Obama administration’s vetoing of the Keystone XL (KXL) pipeline (a proposed pipeline project linking the Alberta tar sands to refineries in the USA)

- The Trump administration’s revival of the KXL pipeline

- The Biden administration’s blocking of critical permits for KXL, which led to the project’s ultimate cancellation in 2021.

- A global pandemic and associated economic shutdowns that saw oil demand plummet and prices fall to $11.26 per barrel in 2020.

- A Russian invasion of Ukraine and ensuing economic sanctions that slashed oil supply, spurred an energy crisis, and sent oil prices soaring to $123.70 per barrel in 2022.

Considering this, it’s pretty safe to say that the company’s 2012 10-year forecast will have differed quite a bit from its 2022 reality.

As ESG rhetoric is heating up in 2022, today’s analysts have even more uncertainties to contend with when making predictions for the next ten years.

Fortunately, these analysts can base their models on the three main drivers of oil price movements.

Three biggest drivers of oil prices

In aggregate, there are three primary and interconnected price drivers in the oil and gas industry: supply and demand, financial speculation, and geopolitical or meteorological events.

- Supply and demand

Actual shifts in supply and demand are the largest real driver of oil prices.

Ceterus peribus, a rise in the amount of oil available on the market (supply) will lead to a price decrease while a rise in the amount of oil that people consume (demand) will lead to a price increase.

During the early months of the pandemic-induced economic shutdowns, people were hardly travelling or driving their cars. This slashed the demand for oil and led to the massive price drops that occurred in March and April 2020.

In contrast, OECD decisions to reduce collective oil production coupled with the economic sanctions against Russia have limited the amount of oil available on the market. This reduced supply has driven the price back above $100 per barrel.

- Financial speculation

Like many commodities, oil is traded on global markets. Anytime markets like this exist, financial speculators emerge to capitalise on expected price changes.

While this financial speculation is often based on robust analyses and decades of wisdom, at its core, it still remains little more than an informed guess about the future.

Price movements may emerge simply because a critical mass of speculators believe that something tangible will happen, even if it never does.

In some cases, this can even lead to a short-term self-fulfilling prophecy for oil prices.

If enough speculators believe that oil prices will increase, they are likely to purchase enough oil futures to create the very increase that they are speculating about to begin with.

While this may only happen in extreme examples, it paints the picture that not all oil price movements are based in reality – but some variation can be attributed to the expectation of some hypothetical future reality that may never come to fruition.

- Geopolitical or meteorological events

The third primary driver of oil prices, which is very closely tied to the first two, is geopolitical or metrological events.

The conflict in Ukraine is a top-of-mind example of a geopolitical situation wreaking havoc on oil prices.

Other examples of this could include an unseasonably cold winter which leads to added heating requirements and increased demand for energy sources like oil.

Weather patterns can also impact the supply side of oil production, particularly for offshore drilling rigs during periods of intense coastal weather and tropical storms.

The interplay between these factors

Thinking through some of these examples it becomes clear how geopolitical or meteorological events will create supply and demand changes.

However, these events, once they begin to materialise, can also have an impact on financial speculation.

For example, the geopolitical event of a military buildup on the Russia-Ukraine border in January 2022, led to financial speculation about how an invasion would impact the actual global supply and demand of oil.

In January it was speculation; on February 24 it was a geopolitical event; now we are beginning to experience the real supply and demand impacts of the invasion.

These, combined with countless other factors in the macroeconomic landscape, have helped set today’s oil price.

The current state of the world is creating an economic boom for oil-producing regions like Saudi Arabia, but these market conditions will not last forever.

As the various cycles continue on their respective courses and these three factors continue to change and interact in complex ways, the prices will change yet again.

Such is the boom and bust cycle of the oil industry.