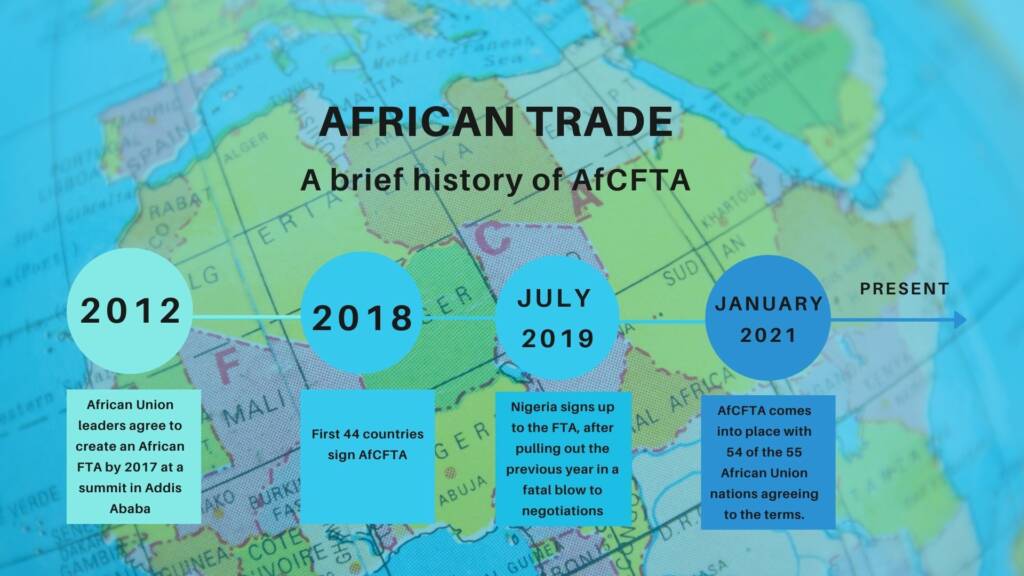

The Africa Continental Free Trade Area Agreement is a 50-year vision of the African Union to support exclusive development across the continent. The objective is to boost intra-Africa trade by providing comprehensive and mutually beneficial trade agreement among the member states. African countries only conduct 16 percent of their trade between each other as opposed to the 65% intra-European and 58 percent intra-Asian trade figures. In 2018, intra-African trade was US$159.1 billion, representing 16.1 percent of total African trade. AfCFTA targets areas across investment, trade in goods and services, intellectual property rights, and competition policy.

Africa covers a wealth of natural resources which are unevenly distributed, hence the need for trade among countries. Based on some studies, the African population is expected to grow in excess of 2.5 billion by the year 2050. AfCFTA brings together 55 member states of the African union, covering a market of more than 1.2 billion people and a gross domestic product of more than US$3.4 trillion.

With the signing of the agreement, African countries can now trade freely between themselves. They can freely import goods they cannot produce or where demand is high, they can also export goods that are in excess. The barriers may be broken and borders open for trade, but companies need accessible financing to meet demands and boost trade. Factoring appears at this level as a financial instrument to boost intra-African trade.

Factoring is an important tool for expanding and facilitating African trade and particularly for the extension of support to SMEs. Many SMEs waste time waiting for their buyers to pay their invoices. Factoring steps in as a vehicle to facilitate companies who are struggling with limited cash flow to perform or stay in business, increasing efficiency and turnover. Factoring is a popular way to grow a business and generate cash-flow, but this function remains underutilised in Africa for several reasons, the most frustrating being unawareness.

Factoring will allow African businesses to trade more competitively through the use of open account, such as import-export factoring, confirming, or cross-border factoring rather than Letters of Credit and other traditional financing options. Afreximbank is actively promoting intra-African trade and has identified factoring as one of the instruments supporting SMEs who are integral to the supply chains and who require supply chain financing.

There can be no question that the COVID-19 pandemic has been both a public health and economic tragedy. Wide ranging predictions have been made as to when the economy will get back to normal. We can barely determine what is normal. This new way of life has reduced physical contact and we cannot determine for how long such restrictions will last. With the massive impact the pandemic is having on African economies, maximising continental trade will be very helpful to African countries. This economic crash has been driven by a mandatory cessation of business in Africa, which has fundamentally shrunk national economies. SMEs are the most affected by this crisis, in a pattern mirrored across the globe.

AfCFTA has appeared when such an agreement is most needed. It is essential for Africa to adopt a continental and regional collaborative trade policy and mechanism. With the signing of AfCFTA, African states will be able to sustain and assist each other to grow and get back on track.

Due to AfCFTA’s implementation, the need for receivables finance will greatly increase as trade barriers will be reduced and firms will have access to a wider market. Africa will be strategically placed to grow its factoring volumes by simply leveraging the existing extra-territorial trade networks. With AfCFTA, Africa seems to be able to benefit not just from trade diversion but also trade creation. The removal of barriers and reduction in rates will lead to increased imports from other African countries, thereby creating alternatives to products commonly sourced or imported from the rest of the world.

Factoring will provide a great rebound to the economy and will favour companies that are bold enough to capitalise on this emerging trend and new business opportunities. Factoring institutions should see this economic situation as an opportunity to finance SMEs through the collateralisation of their receivables. SMEs were hardest hit by the pandemic, with huge numbers going out of business. The resilient ones and those returning to business need financing to meet their greater demand for liquidity. This pinpoints why factoring and supply chain finance is more important than ever.

“SMEs were hardest hit by the pandemic, the resilient need financing to meet their greater demand for liquidity.”

Factoring serves as a cost-effective way for companies to outsource their ledger while freeing up time to better manage their businesses and be more competitive. Companies striving to improve their business via post-pandemic engagement investment must implement strong control measures and try to avoid fraud of any sort. We can rightly say that AfCFTA will be a gamechanger for member states.

Intra-Africa trade deals need technology for moving money on mobile and digital platforms to support traders in the African continent. AfCFTA comes with a series of challenges, one of which is payment methods for the transactions carried out by member countries. For example, the MANSA project, a pan-African customer due diligence repository for financial institutions, corporate entities, and SMEs, was developed to address the perceived risk of doing business in Africa. It hopes to avoid the long transaction process converting to a third currency, such as US dollars, before effecting a trade deal.

There is also a need for a fast, reliable, and secured payment systems – this is where the Pan African Payment Settlement System (PAPSS) comes in. Led by Afreximbank, PAPSS is the first digital payment system to facilitate trade in the continent. African traders face challenges such as inadequate payment infrastructure and payment platforms, which sometimes delay trade transactions. PAPSS connects SMEs to a larger market and accelerates payments while addressing market challenges. This system will save the continent more than US$5bn in payment transaction costs per annum, usually lost in the conversion of trade currencies between African countries to dollars before sealing a deal.

The PAPSS will make it possible for African companies to clear and settle intra-African trade transactions in their local currencies, increase liquidity, and facilitate instant payment.

To conclude, I believe AfCFTA is a great opportunity for Africa to create and integrate a market of more than one billion people, bring about development and reduce the continent’s dependence. Afreximbank leads this project by providing support towards intra-Africa trade using factoring as a pillar and solution to accelerate trade while providing working capital to SMEs, which constitutes the majority of the economic ecosystem of these countries and our future.

Download this article as a PDF