Estimated reading time: 6 minutes

The EU Carbon Border Adjustment Mechanism (CBAM) has sent shockwaves through global supply chains and trade flows. European importers were plunged into complicated new carbon reporting requirements ahead of the deadline on 31 January, 2024.

Meanwhile, manufacturers outside the EU are suddenly receiving mounting requests from their customers for carbon data. They’re told they must calculate their emissions using specific methodologies, under rules set by a jurisdiction that’s not their own.

And this is only the beginning — we’re just in the preparatory phase for the world’s first carbon border tariff.

How can commodity traders and manufacturers prepare? How can banks ensure clients don’t get caught out by CBAM disruptions? Here we share our top lessons from helping EU importers get their first reports done:

Lesson 1: Who owns the CBAM hot potato?

CBAM is a customs and tax issue. It’s also a data project. And a procurement challenge. Plus, for many sustainability teams, it’s a gift: a bold policy to accelerate supply-chain climate goals.

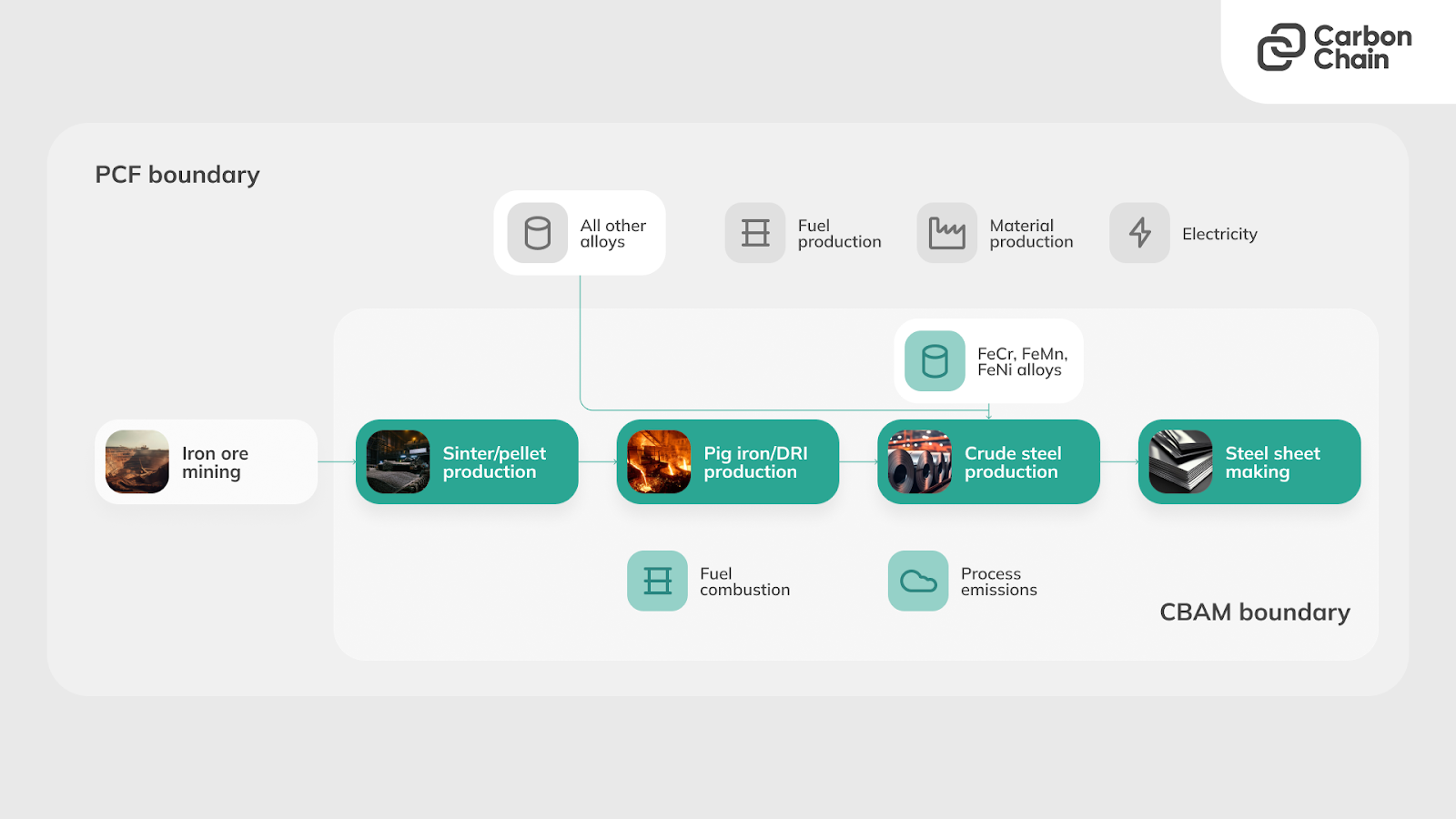

Typically, it’s the customs and VAT teams who will own the import data management, with sustainability and/or purchasing teams owning the engagement with their suppliers.

Forward-thinking importers are quickly getting the right teams resourced to prepare for long-term CBAM success, and partnering with software providers to automate as much of the process as possible.

Lesson 2: Technical issues caused delays – but CBAM isn’t stopping

Throughout January, importers encountered various validation errors and logic issues when trying to submit their declarations on the EU’s CBAM reporting platform.

Luckily, by working with our clients and engaging with the European Commission, CarbonChain was able to identify and support the patching of many of these issues – and all our customers successfully submitted their first CBAM report on time.

The European Commission worked tirelessly on fixes. But, when technical issues still persisted 48 hours before the submission deadline, they allowed affected importers to request a month’s extension.

Once these teething errors are resolved, it will be full steam ahead with the next deadlines (30 April, 31 July 31, 31 October 31), and there’s no room for complacency. Importers who don’t comply could face penalties of €10-50 per tonne of non-reported emissions.

Lesson 3: Registration was harder than expected

Each EU country had its own requirements for gaining access to the CBAM Transitional Registry. That’s because importers (or indirect customs representatives) had to register in their own country with a so-called National Competent Authority (NCA).

Each NCA operated differently. This caused issues for importers with operations in multiple jurisdictions or with inconsistent ownership structures across tax and customs – as is the case with many commodity traders.

However, NCAs were very supportive. Many hosted webinars, improved access guidance on their websites and provided quick responses over email to support declarants. This bodes well for CBAM in the long term. National-level support will be critical as requirements evolve.

Lesson 4: Indirect customs representatives need help

Many importers of goods into the EU are not actually based in the EU, such as Swiss and UK-registered companies. In those cases, their indirect customs representatives were required to take on the CBAM reporting obligation and submit CBAM reports. It’s also the indirect customs reps, as the declarant, who will be liable for penalties for non-compliance.

That’s a significant burden for those reps. Many handle diverse products and CBAM requirements for multiple clients. Tricky conversations with importers are underway as reps figure out what this means for their contractual obligations.

To keep their goods moving, it’s crucial for importers to maintain smooth relations with these representatives, providing timely information, including data from suppliers.

Lesson 5: CBAM costs will be passed along

Like other kinds of economic impacts, CBAM is set to have knock-on effects along the supply chain, through price hikes or tightening purse strings.

Indirect customs reps are looking to pass on CBAM costs and penalty payments. In turn, importers are set to pass on those costs to suppliers.

Some importers will even stop working with suppliers whose product emissions look too expensive under the coming carbon tariff from 2026, or who fail to report their emissions and thereby expose the importer to penalties.

Lesson 6: XML trumps manual entry

Importers can choose how to submit their declaration: as an XML file or manual data entry. Many opted for the XML file option to:

- Allow for automation, saving time and resources;

- Avoid silly errors;

- Enable seamless integration of supplier data.

Steelforce resolved all their data automatically into an XML, meaning they could rapidly complete the CBAM declaration without risks of errors from manual input:

“Steelforce Group entities import numerous CN Codes of steel products from a multitude of countries of origin and valued suppliers. Manually inputting this data into the EU Transitional Registry would have taken significant time and would leave us prone to making manual input errors. Using CarbonChain’s software removed this burden and provided complete control over our CBAM declarations.”

– Oxana Dyupina, Compliance Officer at SteelForce Group

Lesson 7: Data qualities vary – and suppliers are wary

It’s been encouraging to see the volume of data shared by suppliers for this first reporting deadline. However, the quality of that data varies significantly:

- Some supplier installations provided perfectly-completed and quality-checked EU installation communication templates;

- Others didn’t use the template at all (so missed out on aspects of information);

- Others reported using existing product carbon footprints (which are not the same as CBAM emissions reports);

- Many suppliers are still wary of sharing any data, waiting for mandatory verification to come into force, to ensure they’re being compared fairly against their peers.

There’s now just a matter of months left to get things in order. The first two reports can only be corrected until 31 July 2024, and the 4th report (due 31 October 31, 2024) needs to include the correct primary supplier data.

It’s very hard for a declarant to know whether the installation data they receive is actually CBAM-compliant; the European Commission details specific emissions monitoring methodologies which require a high level of carbon accounting expertise.

To overcome this challenge, a number of steel and aluminium traders are using CarbonChain’s platform to map out and assess the quality of supplier data, and they’re rolling out plans to help suppliers implement the right methodology.

Lesson 8: The supplier engagement challenge is huge

For the first three reports, importers can use default carbon intensity values provided by the European Commission, instead of actual emissions data from their suppliers.

But what companies are now recognising is the sheer scale and complexities of obtaining this data from their supply chains:

- How can I convince my suppliers to share this data?

- How will I collect this data from suppliers in a streamlined way?

- How will I know if the data is compliant?

- How can I support installations to produce compliant data when I know nothing about carbon accounting?

- What data do I need from my own manufacturing sites?

The barrier of entry for carbon accounting is high, coupled with the added strain on procurement processes and supplier relationships. We encourage companies to get in touch or explore CarbonChain’s resources for guidance.

Make CBAM work for you

The first chapter of CBAM highlights the importance of internal collaboration, tech adaptation, and supplier engagement. This regulatory mechanism isn’t just about compliance; it’s designed to drive a more sustainable, transparent economy.

There will be winners and losers, as some companies act last-minute and struggle, while others strategically prepare to make CBAM work for them. We’ve seen major traders and their facilities use CBAM as a catalyst to do full product carbon footprinting of all the goods they buy and sell and find ways to reduce emissions to gain a competitive edge.