Estimated reading time: 5 minutes

Despite the attention brought to the trade finance gap in recent years, it still continues to grow. A recent Asian Development Bank (ADB) report shows that the gap has now widened to $2.5 trillion.

Despite best efforts, the status quo is clearly not addressing the gaps sufficiently. The wider industry needs to come up with new and creative solutions in response. No one option will succeed by itself, but it is becoming increasingly clear that trade credit insurance has an important role to play in helping to close the gap further.

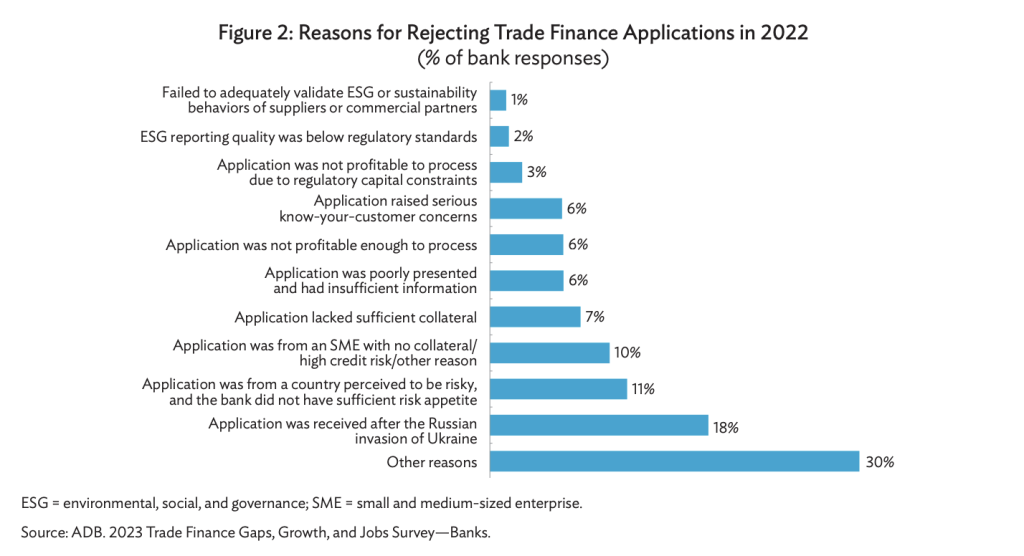

In the report, ADB rightly mentions that the lack of availability of (sufficient) collateral is a cause of rejection of trade finance applications. Figure 2 shows that in 28% of cases, insufficient collateral plays a role – whether directly or as a result of the risk perception of the financial institution in question. A further 9% of rejections are caused by cost/capital considerations.

The question remains, how does trade credit insurance help in three vital topics: collateral, risk appetite, and cost?

1. Collateral

Credit insurance helps narrow the trade finance gap by providing security (the policy) based on its unrivalled ability to mitigate risk. ICISA’s trade credit (re)insurance members hold credit ratings of at least A- (S&P or equivalent). This credit rating takes the place of that of the buyers when a covered financial institution finances invoices.

Banks are not equipped to assess large numbers of (sometimes very small) risks. On the other hand, this is the credit insurance community’s core competency. Insurers are aided by large internal databases of information (supplemented with third-party information) on diverse buyers. Underwriting processes are flexible and efficient incorporating automated, semi-automated and (as an exception) manual processes to make decisions.

2. Risk appetite

Unfamiliarity with risks tends to lead to higher pricing. Credit insurance companies are familiar with the great majority of risks (whether corporate or country risk). This allows them to price more accurately and show a higher acceptance rate than a local/national bank.

It stands to reason that a Malaysian bank is less familiar with Colombian corporates and/or country risk than an internationally active credit insurance company with a presence in Malaysia as well as Colombia. This familiarity also enables the credit insurers to have a greater appetite for risks.

Cover may therefore be easier to find from trade credit insurance markets than financial institutions with less experience of these markets and risks.

Familiarity with, and confidence in the credit insurance policy as collateral is another important form of risk appetite. This form of collateral is ubiquitous in the OECD area and becoming ever more common in Latin America, Southern Africa and parts of Asia.

The credit insurance community has become active in spreading the word in parts of the (developing) world, where trade credit insurance is not as well.

You may note that in our upcoming Trade Credit Insurance week (online in the week of 2 October), there are items on the development of the product in Sub-Saharan Africa, and one on the further development of trade credit insurance in Asia, reflecting the demand for more information about – and in – these markets

3. Cost

The high-investment grade nature of the insurers has a beneficial effect for the banks’ cost of capital, as well as the resulting price to be paid by the financed entity, thus narrowing the trade gap.

Notable reforms

ICISA is a supporter of the Digital Standards Initiative of the International Chamber of Commerce (https://www.dsi.iccwbo.org/) through membership in the Industry Advisory Board. We firmly believe that setting international standards for digital/paperless trade will have a beneficial effect on trade volumes as well as transparency of the entire process.

Apart from lowering the cost of trade, digitalisation reduces many of the barriers to entry that SMEs and startups in developing countries face. Importantly, it also enhances options for financial crime prevention, including more reliable information as part of Know Your Customer and other compliance procedures.

Related to this, a key concern for many across the industry in addressing financing gaps is the reliability of the rule of law across the world. It is important that key institutions, such as courts, are reliable, predictable and free from corruption.

This is not a simple issue to fix, but if we are serious about addressing the trade finance gap it is one of the most important, along with the availability and reliability of business information.

Identifying and supporting civil society organisations across the world which are working on this topic may be a good starting point.

Top challenges

I support ADB’s list of recommendations and would like to expand on the first and most important one: the creation of additional capacity.

Firstly, giving appropriate recognition to trade credit insurance as a credit risk mitigation tool (providing collateral) would help to broaden awareness of the product and its benefits. This additional risk mitigation mechanism has been proven to increase the financing capacity in multiple jurisdictions.

Secondly, it must be acknowledged that distribution mechanisms in countries needing the most economic development are poor. Even when banks are present in communities outside of the capital and major trading localities, they often lack the financial insight necessary to market and assess much-needed financing.

Rejection of a facility based on poor presentation of the credit application should be a call to action to educate the distribution network and applicants. This will ensure that applications are presented in a way which addresses the key questions any financier will have and can then form an opinion of.

Finally, focusing on banks only solves part of the issue. And this cannot be a one-size-fits-all solution, given the complexity of global trade. In particular, I believe more attention should be paid to the factoring community and the positive impact they can (and already do) have. Factors are traditionally better equipped to serve smaller, less sophisticated clients.

{kind=link}