- Access finance

- Case studies

-

Informing today's market

Financing tomorrow's trade

Soft commodities trader

Due to increased sales, a soft commodity trader required a receivables purchase facility for one of their large customers - purchased from Africa and sold to the US.

Metals trader

Purchasing commodities from Africa, the US, and Europe and selling to Europe, a metals trader required a receivables finance facility for a book of their receivables/customers.

Energy trading group

An energy group, selling mainly into Europe, desired a receivables purchase facility to discount names, where they had increased sales and concentration.

Clothing company

Rather than waiting 90 days until payment was made, the company wanted to pay suppliers on the day that the title to goods transferred to them, meaning it could expand its range of suppliers and receive supplier discounts.

Get Trade Finance

Informing Today’s Market, Financing tomorrow’s Trade.

-

- Case studies

Home / Introduction to Payments /

Payment Infrastructure and Support

Access trade, receivables and supply chain finance

We assist companies to access trade and receivables finance through our relationships with 270+ banks, funds and alternative finance houses.

Get startedContent

What are payment systems and how do they work?

Payment systems are simply the various methods and processes that allow individuals, businesses, and financial institutions to transfer money or other forms of value between each other.

While they are simple in concept, the inner workings of these systems can be complex and typically involve a series of steps that enable the sender to initiate a transaction and the recipient to receive the funds.

The basic process of a payment system involves three key players:

- a payer: the person or organisation initiating the payment

- a payee: the intended recipient of the payment

- a payment intermediary: the entity that facilitates the transfer of funds between the payer and the payee

Payment systems can take many forms, including traditional cash, cheques, and bank transfers, or newer digital payment technologies like mobile payments, online transfers, and cryptocurrencies. They generally work by processing and verifying the transaction details, such as the payer’s account information, the amount to be transferred, and the payee’s account information.

The payment intermediary then facilitates funds transfer by directly debiting and crediting the respective accounts or leveraging an intermediary clearinghouse’s services to perform similar functions.

While the exact mechanics of such systems will vary depending on the specific type of payment, plus the regulations and infrastructure available in the regions, the fundamental principles remain the same: facilitate the transfer of funds between different parties securely and efficiently.

How are payments regulated?

Payment systems are typically regulated by a combination of government bodies, industry organisations, and self-regulatory bodies.

Like all international transactions, the regulatory nuances will vary from region to region, but they generally all exist to help protect consumers and businesses from fraud and other risks.

In many countries, central banks play a crucial role in regulating payment systems. For example, the United States Federal Reserve oversees America’s payment system, while across the Eurozone, the European Central Bank bears this responsibility. These central banks may set rules and standards for payment systems, monitor their performance, and intervene if necessary to address issues or mitigate risks.

In addition to central banks, other regulatory bodies may also play a role in regulating payments.

For example, in the US, the Consumer Financial Protection Bureau (CFPB) enforces consumer protection laws related to payments. At the same time, in the European Union, the European Banking Authority (EBA) is responsible for ensuring payment systems’ safety and soundness.

Industry organisations and self-regulatory bodies may also help to regulate payment systems.

In the US, the National Automated Clearing House Association (NACHA) sets rules and standards for the automated clearing house (ACH) system, while the Payment Card Industry Security Standards Council (PCI SSC) sets standards for the security of credit and debit card payments.

Regardless of their form, these regulatory bodies face the complex challenge of balancing the need for innovation and efficiency with the need for safety and security to ensure that payment systems operate fairly and transparently for all stakeholders.

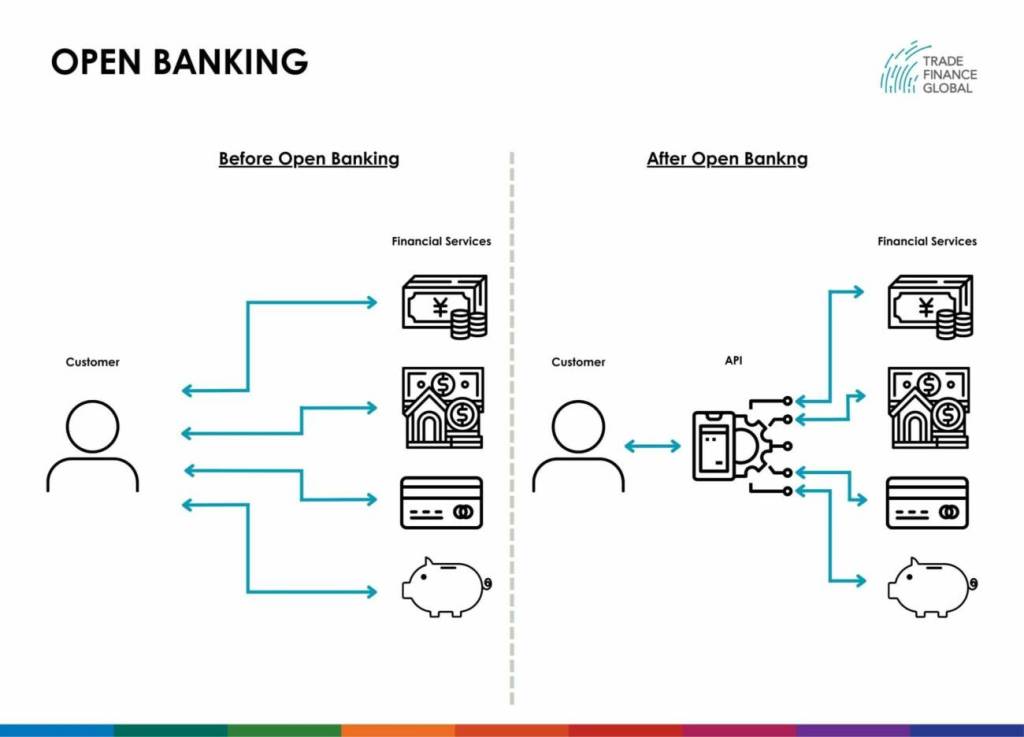

What is open banking?

Open banking is a financial industry term that refers to a set of practices and regulations that enable third-party financial service providers to access bank customer data (with the customer’s consent) and initiate transactions on their behalf.

At its core, open banking is about creating more competition and innovation in the financial industry by opening up access to financial data and services.

This allows customers to benefit from more personalised financial services, improved access to credit and investment options, and better rates on loans and other financial products.

Open banking typically relies on Application Programming Interfaces (APIs), which are sets of programming instructions that allow different software applications to communicate with each other. APIs allow third-party providers to securely access customer data and initiate transactions.

This modernised approach to banking has already been implemented in various forms worldwide.

In the EU, for example, the Payment Services Directive 2 (PSD2) requires banks to allow third-party providers to access customer data and initiate transactions, subject to particular security and privacy requirements.

In the UK, the Open Banking Implementation Entity was established to promote open banking and develop standards for APIs and data sharing.

Open banking has already begun transforming the financial industry by promoting competition and innovation, improving access to financial services, and empowering customers to take control of their financial lives.

But like many innovations, it also raises some significant concerns, particularly around privacy, security, and data protection, which must be carefully considered and addressed to ensure that open banking benefits customers and the broader economy.

Open Banking Diagram

Types of payment mechanisms

Individuals, businesses, and financial institutions can use various types of payments to transfer funds or other forms of value.

Some, such as cash, are relatively simple and have been around for hundreds of years, while others, like cryptocurrencies or central bank digital currencies (CBDCs), are relatively new innovations.

Some of the most common payment mechanisms include:

- Cash: Physical currency, coins, or banknotes that can be exchanged for goods and services.

- Cheques: Written orders to a bank or financial institution to pay a specified amount to the person or entity named on the cheque.

- Bank transfers: Electronic funds transfers between bank accounts, which can be initiated through online banking platforms, wire transfers, or other means.

- Credit and debit cards: Payment cards enabling customers to make purchases and withdrawals using funds from their bank accounts or credit lines.

- Mobile payments: Payments made through mobile devices, often using digital wallets or other mobile apps that link to bank accounts or credit cards.

- Cryptocurrencies: Digital currencies that use encryption techniques to secure transactions and control the creation of new units.

- Central bank digital currencies (CBDCs): Digital versions of a country’s flat currency issued and backed by the central bank.

- Electronic wallets (e-wallets): Digital wallets that store payment information and can be used to make purchases or transfer funds.

- Peer-to-peer (P2P) payments: Transactions between individuals or businesses, often facilitated through digital platforms or apps.

- Prepaid cards: Payment cards loaded with specific funds, which can be used to make purchases or withdrawals until the balance is depleted.

These are just a few examples of the many payment methods available today. As the financial industry evolves, new payment methods and technologies will likely emerge, creating new opportunities and challenges for consumers, businesses, and regulators.

Publishing partners

- Payments Resources

- All Payments Topics

- Podcasts

- Videos

- Conferences