Banks play a crucial role in facilitating trade flows by providing funds to sellers against documents and by reducing counterparty risk. Presently these “back-end” trade finance processes require large teams reviewing paper documents. These processes have been adversely impacted because of restrictions in workplace (such as social distancing and teleworking) that have been imposed due to the outbreak of COVID-19 virus.

The disruptions may lead to the seller/ beneficiary missing deadlines for document submission and the credit expiring, or the bank missing its deadlines regarding notification of non–complying presentation after examination of the documents submitted by the beneficiary.

A seller/ beneficiary to a documentary credit (letter of credit, standby or guarantee) has to meet two deadlines:

- last day of shipment (pre-shipment phase)

- last day of presentation of documents as mentioned in the documentary credit (post shipment phase). It is in this phase that discretionary power vests with the bank to reject delayed or incomplete presentation even if the delay or incomplete submission are caused by force majeure events beyond the control of the (such as courier companies refusing booking or delivery) beyond the control of the presenter.

Similarly, under UCP 600, banks have to meet the deadline of notifying discrepancies or rejecting the presentation not later than 5 days following the date on which presentation is made.

How are the rights and obligations of the parties to a credit affected on account of missed deadlines caused by these force majeure events?

To answer this question, one needs to refer to the practice rules promulgated by the International Chamber of Commerce (ICC).

Practice rules in documentary trade

The practice rules referred to in this article are

Presently, almost all documentary credits are issued as letters of credit, subject to UCP 600. Except ISP 98, each of the practice rules contains an article regarding force majeure events.

Force Majeure – What are the key issues?

- What are force majeure events? Which is the authority that can declare an event as force majeure?

- What are the specific credit processes that are directly impacted due to force majeure events?

- Force majeure events and rules regarding expired credit or delayed presentation under (1) UCP 600, (2) ISP 98, (3) URDG 758

- Differences, if any, between UCP 600, ISP 98 and URDG 758 with regard to the issuing/nominated bank’s obligations and rights, where there is delayed presentation or delayed examination caused by force majeure disruption

- Remedy available with beneficiary

Force Majeure events and proclamation authority

In March 2020, the ICC released a document stipulating the standard definition of the force majeure clause.

According to this definition, “Force Majeure” means the occurrence of an event or circumstance (“Force Majeure Event”) that prevents or impedes a party from performing one or more of its contractual obligations under the contract, if and to the extent that the party affected by the impediment (“the Affected Party”) proves:

- that such impediment is beyond its reasonable control;

- that it could not reasonably have been foreseen at the time of the conclusion of the contract;

- that the effects of the impediment could not reasonably have been avoided or overcome by the Affected Party.

The ICC cannot pronounce an event as a force majeure event. According to the ICC, a court or tribunal with jurisdiction, or a government or regulatory authority has to make a decision as to declaring whether an event of force majeure.

For example, at the time of the outbreak of the COVID-19 outbreak, the China Council for Promotion of International trade (CCPIT) issued many ‘force majeure certificates’ to businesses affected by the virus, in a bid to exempt those businesses from fulfilling their contractual obligations, without breach of contract consequences.

UCP 600 and Force Majeure

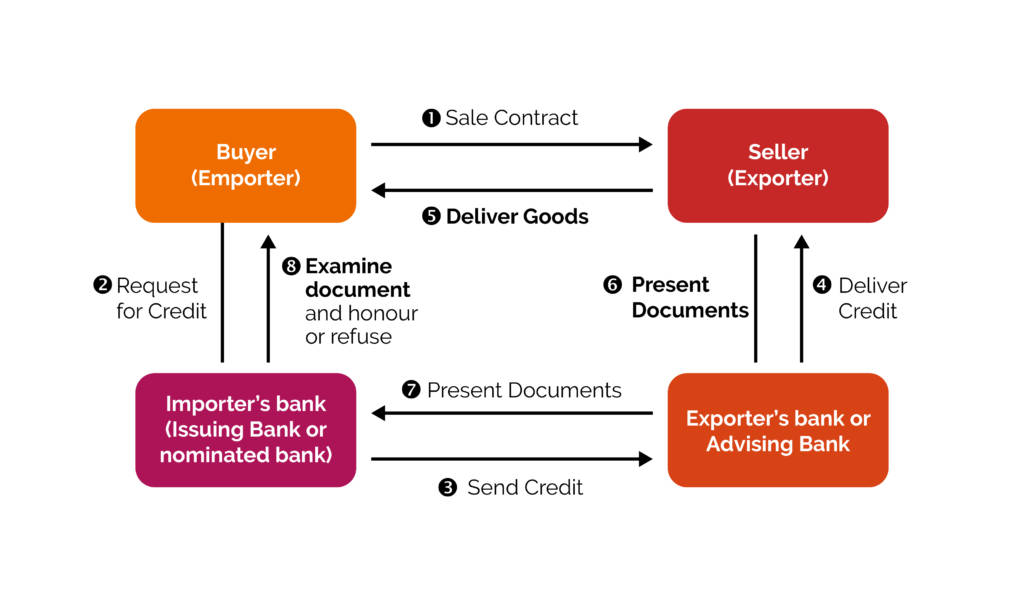

The normal LC process flow can be diagrammatically represented as follows:

The processes outlined in bold above are time-dependent processes which could be affected on account of force majeure events

- The delivery of goods is subject to a last shipment date

- The presentation of documents by seller should be made within 21 days of the day of shipment

- Examination of documents by issuing bank should be done within 5 days following the day of presentation.

In cases of force majeure interruptions, presentation and examination might get delayed thereby affecting the decisions of the beneficiary’s bank and issuing/nominated bank on account of expired credit or delayed presentation.

Rules concerning expired credit or delayed presentation on account of force majeure

- UCP 600 Article 36 – A bank assumes no liability or responsibility for the consequences arising out of interruptions of its business by Acts of God, riots, civil commotions, insurrections, wars, acts of terrorism, or by strikes or lockouts or any other causes beyond its control. Upon resumption of business, a bank will not honour or negotiate under a credit that expired during such interruption of its business

- UCP 600 Article 35 – A bank assumes no liability for the consequences arising out of the delay in delivery of documents when such documents are sent as per the instructions in the credit.

If the nominated bank determines that a presentation is complying and forwards the documents to issuing bank, the issuing bank must honour, even if the documents are lost in transit.

- URC 522 Article 15 – This article is similar to Article 36 of UCP 600 mentioned above.

- URDG 758 Article 26 – If the presentation cannot be made because of force majeure reasons and the guarantee expires during the period the presentation is prevented, the expiry date shall be extended by a period of 30 days from the date of the original expiry date. If the force majeure event still persists at the end of the 30 day extension, the guarantee expires and no claim is possible.

- ISP Rule 3 (14) – The ISP does not have any force majeure clause. However, it does have a general clause which states that if a bank is closed on the last business day for presentation for any reason and presentation is not made because of closure, then the last day for presentation is automatically extended to 30 calendar days after reopening.

Some scenarios under UCP 600 arising out of force majeure disruptions

- Force majeure at issuing bank location and credit expired during interruption

Bank may refuse to honour (Article 36) - Force majeure at nominated bank location and credit expired during interruption

Bank may refuse to honour (Article 36) - Force majeure at nominated bank location and presentation made direct to the issuing bank which is open for business

Credit available with nominated bank is also available with issuing bank (Article 6a). Thus the issuing bank should honour, if the presentation is timely and complying. - Presentation made within validity of LC but bank delayed notifying to presenter/beneficiary and force majeure interruptions occurred after the expiry of the 5 day notice period leading to closure.

Issuing bank must honour as it failed to notify within the period of 5 days. The bank cannot claim non-complying presentation, on account of the delay in notifying (UCP 16-f) - LC permits multiple drawings within stipulated periods. Seller fails to draw one instalment because of force majeure events

Bank will not honour subsequent drawings (article 32). - Shipment could not be made within the last shipment date due to force majeure causes. Documents presented on day when bank is closed for reasons other than force majeure

The expiry date or the last date of presentation will be extended to the following banking day, but the latest shipment date cannot be extended (Article 29c) - Nominated bank hands documents over to courier but courier cannot deliver anywhere in the destination country.

Nominated bank is covered by UCP 600 article 35 and it is not responsible for delay. The issuing bank should provide alternative options for delivery. - Nominated bank hands over documents to courier named in the credit. Courier can deliver into destination country but not to the specific address.

Nominated bank is not responsible and is covered under Article 35. The issuing bank should provide alternative options for delivery

Similar scenarios exist for demand guarantees.

Position under ISP 98

ISP98 does not contain a rule specifically titled ‘Force Majeure’ or events beyond the control of the bank. It provides a general rule, in 3.14, titled “Closure on a Business Day and Authorisation of another Reasonable Place for Presentation”:

- If on the last business day for presentation, the place for presentation stated in the standby is for any reason closed and presentation is not timely made because of closure, then the last day for presentation is automatically extended to the day occurring thirty (calendar) days after the place for presentation re-opens for business, unless the standby states otherwise.

- Upon or in anticipation of the closure of the place of presentation, an issuer may authorise another reasonable place for presentation in the standby or in a communication received by the beneficiary. If it does so, then:

- presentation must be made at that reasonable place;

- if the communication is received fewer than thirty calendar days before the last day for presentation and for that reason presentation is not timely made, the last day for presentation is automatically extended to the day occurring thirty calendar days after the last day for presentation.

Regarding the various scenarios discussed above, the beneficiary stands in a very favourable position under ISP 98, compared to the provisions of UCP 600.

Risk mitigation by the beneficiary

The beneficiary may be able to avoid adverse repercussions discussed above by seeking insertion of a clause aligned with Rule 3.14 of ISP 98.

e-UCP and definition of Force Majeure

The e-UCP permits the presentation of both paper and electronic documents. Thus, besides the events mentioned in Article 36 of UCP 600, other terms such as data processing system, software or communication networks have been added, for alignment with electronic documents and presentation.

Force majeure events and responsibility of banks are dealt with in article e14 of e-UCP

According to this, a bank assumes no liability or responsibility for the consequences arising out of the interruption of its business, including but not limited to its inability to access a data processing system, or a failure of equipment, software or communications network, caused by Acts of God, riots, civil commotions, insurrections, wars, acts of terrorism, cyberattacks, or by any strikes or lockouts or any other causes, including failure of equipment, software or communications networks, beyond its control.

Timely presentation of documents under e-UCP rules

The chief concern for the beneficiary is the timely presentation of the documents. Unarguably, as compared to paper documents, the beneficiary stands a far better chance of timely submission of electronic documents, provided that the documents are available in electronic form.

Computer systems are becoming increasingly reliable and robust. Every day, transactions worth trillions of dollars are undertaken through a global giant network of computers without a glitch. In such situations, the electronic presentation of documents enables the beneficiary to comply with the deadline related to the timely presentation, provided that all the documents are available in electronic form. The credit should be subject to the e-UCP rules (latest version) and there should be an electronic address to which the presentation can be made.

In a force majeure situation, there is less chance of the electronic address is inaccessible, as compared to a physical location of the issuing/nominated bank, which may be closed or to which documents cannot be mailed because courier services are not available. The electronic presentation does away with several such constraints.

Further business continuity plans of the bank will enable the beneficiary to present to an alternative electronic address.

ARTICLE: Negotiable Instruments are going through a makeover – the who, what, where, why

Non-availability of all documents in electronic form

Where some documents are not available in electronic form, the beneficiary has to provide a certificate of completion, in case all documents are not delivered at the same time. If a force majeure event occurs before physical documents or certificate of completion are submitted and the LC has expired, the bank may refuse to honour, as per e-UCP 14.

URBPO 750

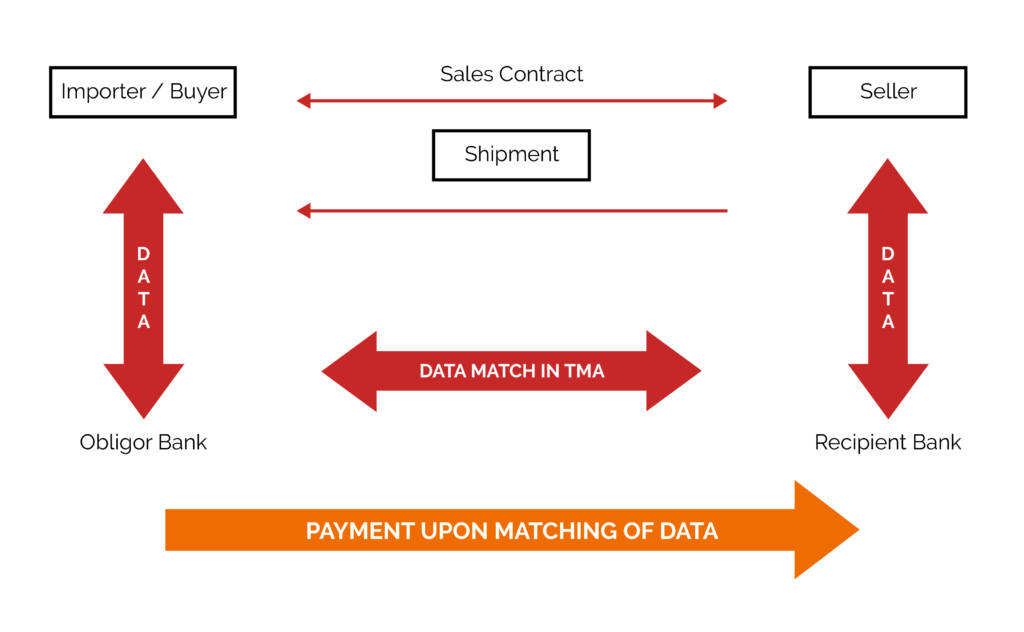

The Uniform Rules for Bank Payment obligations (URBPO) present an alternative payment mechanism based on matching of data as against the matching of documents in the UCP or e-UCP rules.

A bank payment obligation is an irrevocable undertaking from one bank called the obligor bank (buyer’s bank) to pay a recipient bank an agreed sum of money at a future date based on the matching of data or upon acceptance of data mismatch (Article 3 of URBPO)

Video: Tackling digital trade challenges and cMatch – Can we make trade paperless? (essDOCS)

No document delivery requirement

Under a BPO, there is no electronic presentation of documents, as required in other ICC rules. The obligor bank should pay when

- Data has been uploaded in a bank to bank transaction matching system, based on a prior agreement between the seller and buyer regarding the relevant data

- The transaction matching system identifies a “data match” or there is agreement between buyer and seller that payment can be made despite data mismatch

The BPO process flow chart is as below

Force Majeure and URBPO

Article 13 of URBPO 750 defines force majeure events, similar to the definition in e-UCP. Accordingly, failure of equipment, software and communication are included in the list of force majeure events.

However, there is a significant difference between the rights and obligations of the obligor bank, as compared to the rights and obligations of the issuer bank under UCP/e-UCP rules. Under URBPO, after the resumption of business, the obligor bank remains liable for any liability that expired during the force majeure period.

It is clear that going completely digital is the way forward towards the resolution of the problems mentioned above. In recognition of the urgent imperative, the ICC has recommended a two-pronged approach.

- As a temporary measure, the ICC has urged Governments to void any legal requirement for a hard copy of documents. The main documents that fall in the category of the mandatory hard copy are transport documents and bills of exchange.

- Adopt legal frameworks to establish the equivalence of electronic records and paper records. As part of this, the ICC has recommended adoption of the UNCITRAL Model Law on Electronic Transferable Records.

This article was written by a member of TFG’s 2020 International Trade Professionals Programme. Find out more here.

Disclaimer: The views that have been expressed on this page are that of the author, which may or may not be in line with their company, Trade Finance Global or London Institute of Banking and Finance’s view.