Today, the OECD released their International Trade Statistics report for Q2 2023. The report offers an insight into the global trade landscape, highlighting significant shifts and trends. With a decline in G20 merchandise trade and a marked slowdown in services trade, the report paints a complex picture of international commerce.

From the contraction in North American trade to the growth in certain European sectors, the world of international trade proves yet again, to be ever-changing and exciting.

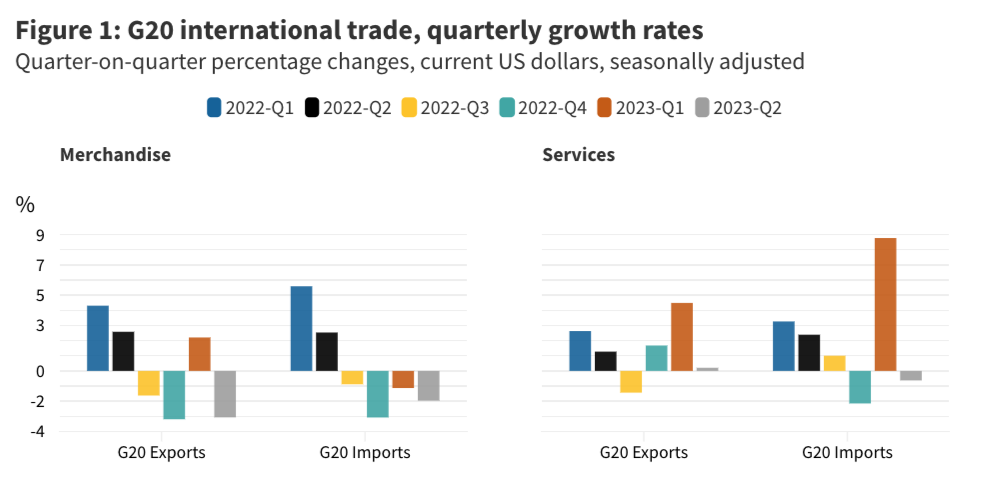

G20 merchandise trade decline

The G20 merchandise trade saw a contraction in Q2 2023, with both exports and imports falling by 3.1% and 2.0%, respectively. This decline is attributed to subdued global demand and decreasing commodity prices, particularly in the energy sector.

North America experienced a significant reduction in trade, with the United States witnessing a 5.7% contraction in exports and 2.0% in imports. Canada’s exports fell by 3.7%, while imports remained flat.

Source: OECD

In the European Union, Germany and Italy saw a decrease in merchandise exports, while France experienced growth, driven by the transport equipment sector, especially aeronautics. The United Kingdom’s exports increased by 2.1%, reflecting strong sales in machinery and transport equipment.

East Asia faced a sharp contraction in merchandise trade, with China’s exports dropping by 5.7% due to lower consumer electronics sales. Japan and Korea saw a marked decrease in imports, down by 8.1% and 7.9% respectively, mainly due to reduced energy import expenses.

Services trade slowdown

Preliminary estimates indicate a marked slowdown in G20 services trade in Q2 2023. Exports and imports are estimated to have grown at 0.2% and minus 0.6% respectively, following the strong growth recorded in Q1 2023. The United States saw a 1.0% growth in services exports, while imports decreased by 1.3%, primarily due to lower expenditure on transport and travel.

In Canada, travel and business services boosted exports, while Germany experienced a decline in exports driven by travel and business services. The United Kingdom’s services exports decreased by 1.0%, while imports rose by 2.9% due to higher purchases of financial, intellectual property, and business services.

Australia and Korea saw a significant expansion in services trade, with travel, finance, and ICT driving up exports in Korea. Japan’s services imports dropped by 4.2%, reflecting lower expenditures on business services.

Country-specific insights

- United States: The decline in merchandise trade was significant, with falling energy prices contributing to reduced trade in value terms.

- United Kingdom: The UK saw an increase in exports by 2.1%, reflecting strong sales of machinery and transport equipment.

- China: China’s exports dropped sharply by 5.7%, partly due to lower consumer electronics sales.

- Australia and Indonesia: Falling commodity prices pushed down exports in these countries.

- France: France’s growth in exports was driven by transport equipment, particularly aeronautics.

The Q2 2023 report on international trade statistics by the OECD paints a picture of a global trade environment facing challenges and shifts. The decline in merchandise trade across the G20 nations reflects broader economic trends, including subdued global demand and fluctuating commodity prices.

The services sector also experienced a slowdown, with varying impacts across different countries and industries. While some nations like Australia and Korea saw growth, others faced contractions, reflecting the complex and multifaceted nature of international trade.

What’s next for international trade?

This report highlights certain trends in international trade for 2023. Looking at the data, it is good to ask questions about the environment for the rest of the year.

How will the continued fluctuation in energy prices impact global trade in the coming quarters, and what strategies can countries adopt to mitigate these effects?

What are the underlying factors contributing to the slowdown in services trade, and how can countries leverage opportunities in this sector?

What are the implications of regional variations, and how can they inform international trade policies and agreements?