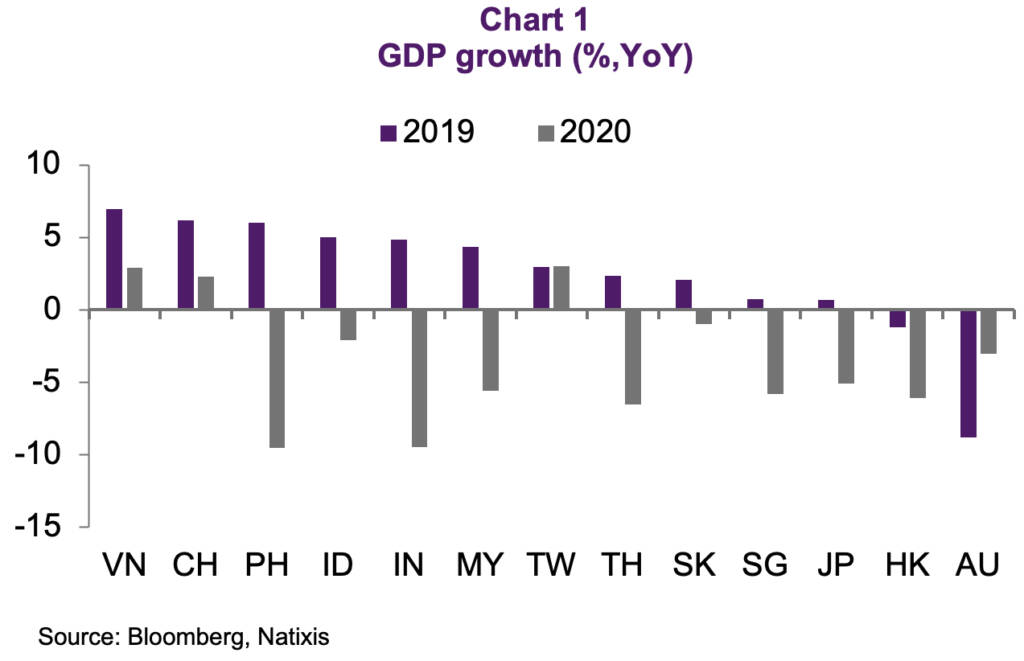

2020 was a terrible year for Asia but for some less than for others. A number of countries managed to grow positively notwithstanding the pandemic, with Mainland China as the most obvious example but not the only one. Taiwan grew above potential and Vietnam grew positively. The rest of Asia really had a hard time, especially India as well as India and the Philippines, due to the much wider spread of the pandemic and the limited fiscal and monetary space. Small open economies, such as Singapore and Hong Kong also suffered immensely due to their reliance on people to people movement (Chart 1).

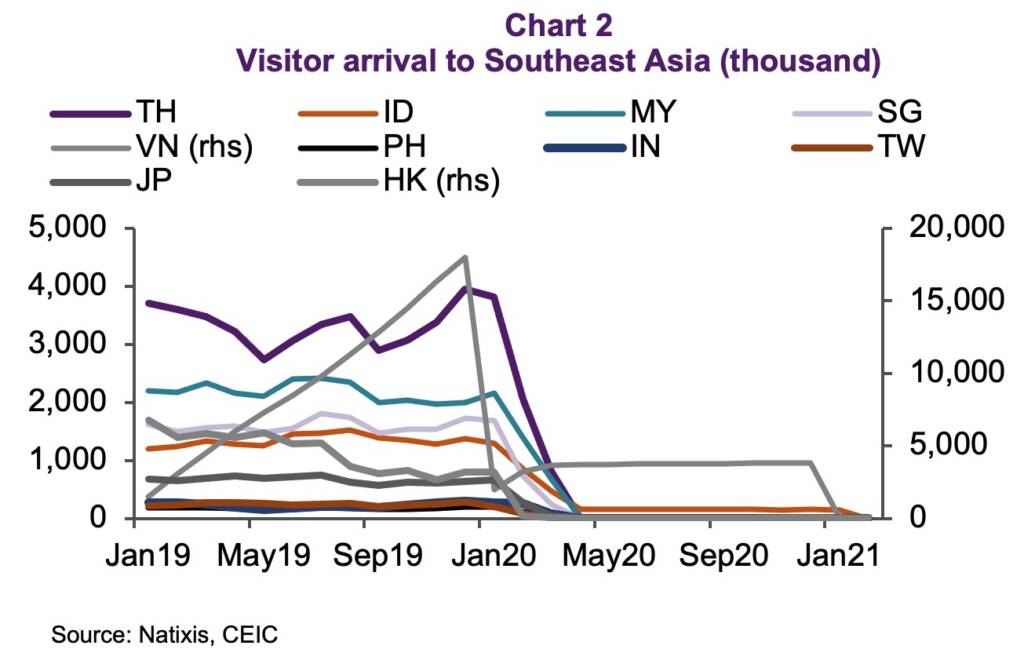

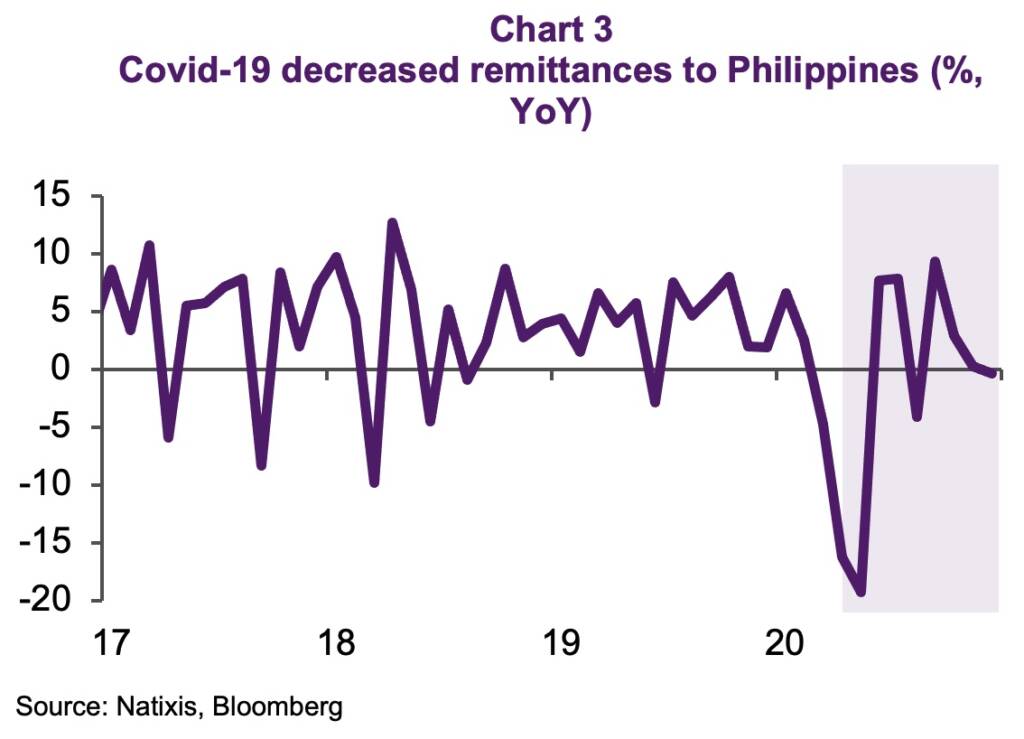

A number of lessons can be learned from this very different economic impact of the pandemic across Asian economies. The first is that a strong domestic demand does help. This is clearly the case in China. Secondly, sectoral specialization is also important. For example, the South Korean and Taiwanese economies were supported by their ITC-oriented export structure, as opposed to economies dependent on the export of services, whether tourism like Hong Kong, Singapore, or Thailand (Chart 2) or remittances, like the Philippines (Chart 3). Thirdly, countries with current account deficits do not have as much room to support the economy without risking an increase in the external cost of funding. This is the case of India, Indonesia, and the Philippines.

Finally, the fiscal and monetary policy reaction to the pandemic which not only depends on the authorities’ willingness to mitigate Covid-19’s economic impact, but also the policy space they may have to do so. In fact, the economies most affected, the Philippines, India, and Indonesia, are also the ones with the least fiscal support (Chart 4). Part of that reason is the tendency to be fiscally prudent given weak revenue generation and unwillingness to raise the debt burden significantly as the deficit already widens through revenue decline, leaving less space for large expenditure increase. Furthermore, economies that have sizeable domestic savings such as Japan and Singapore have deployed much more capital.

Beyond fiscal support, monetary policy easing has been rather aggressive in Asia through not just policy rate cuts but also moving into quantitative easing (QE). In fact, Australia followed Japan in introducing yield curve control as quantitative targets for purchases of assets and the latter is true for South Korea. As for emerging economies, India, Indonesia, and the Philippines, all introduced quantitative easing, to varying degrees. While the Bank of Thailand did not introduce QE, it did create funds to purchase corporate bonds to shore up financial markets. Except for China, funding costs declined across Asia as risk appetite returned. Still, real monetary conditions remain tight across Asia as growth, and thereby inflation weakened much more than the easing of rates.

In 2021 a number of roadblocks to growth are being cleared, starting with better domestic mobility. Global mobility is still very much constrained which means that small open economies like Hong Kong and Singapore will continue to suffer in relative terms. Of course, nowhere is as normalized domestically as in Mainland China, Taiwan, and Vietnam, which explains their much better economic performance so far. Besides, emerging Asian economies, especially the worst performing ones in 2020 due to the favorable base effect, have already started to stage a recovery on improved financial conditions, led by a softening USD and low rates globally.

That said, the recovery in 2021 is not without risks, most of which may linger beyond 2021 and probably get accentuated over time.

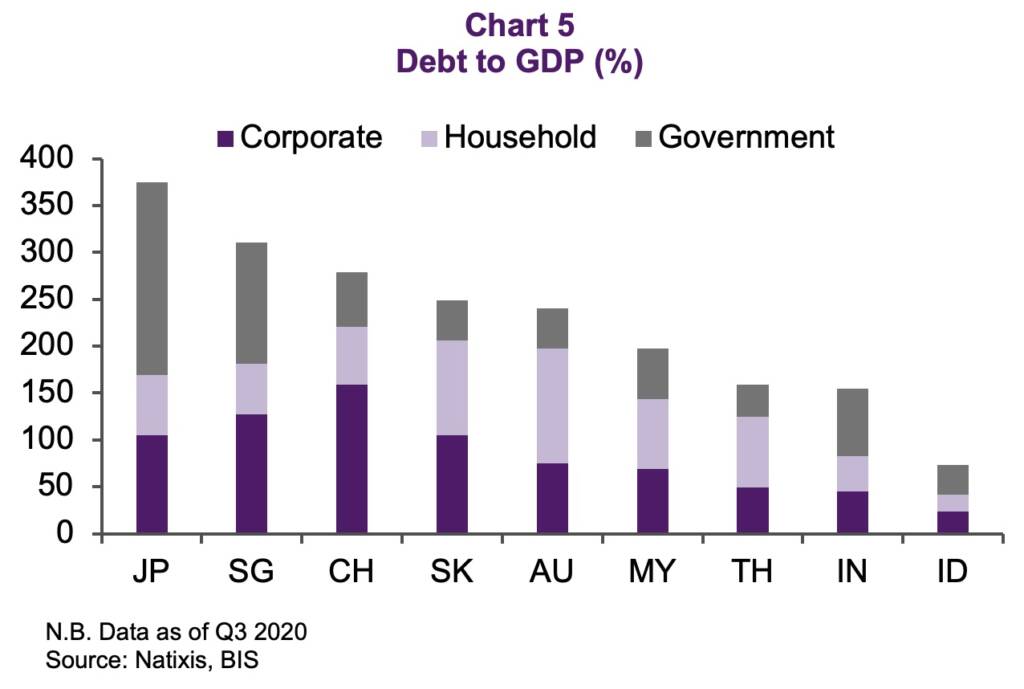

The most obvious one is debt but there are also more structural matters such as aging. Most Asian economies have swiftly offset suppression measures with direct and discretionary stimuli but revenue has continued to weaken whether at the company, household, or government level. In the same vein, debt has continued to pile albeit to a lesser extent than in developed markets. Correspondingly, on the private sector side, companies shed headcount and reduced investment as revenue and profitability stalled. That has helped with the adjustment process by lowering costs but still leave the stock of debt elevated. On the household side, given limited income support by governments, Asian households have taken up more debt with falling income growth. South Korea stands out, given its already very high household debt (Chart 5). The increasingly high debt levels imply that monetary support will remain necessary to keep interest payments sustainable. On the household side, higher debt levels in places with already high debt load such as Australia, South Korea, and Thailand mean that the propensity to consume in the future is also dampened by high-interest expense payment – a key risk to our recovery prospect.

For lowly indebted economies such as Indonesia, India, and the Philippines, the worry is less about the debt stock, especially household debt, than about income sources. To cope with weaker earnings, households, and corporates reduced consumption and investment significantly and more than the rest of Asia, helping with the national balance sheet. That said, given the already relatively low living standards and GDP per capita, this coping mechanism is unsustainable and these economies need to raise income sources to grow consumption and investment. The second important challenge is accelerated aging, due to Covid-19 and related uncertainties. Dampening growth momentum puts pressure on already weak pension systems that are further eroded during the pandemic as countries dip into savings to offset income. Covid-19 has not helped as fertility rates fell further for countries such as Mainland China and South Korea, exacerbating existing trends. The working-age population in Hong Kong, Japan, Mainland China, Singapore, South Korea, Taiwan, and Thailand peaked in 2015 and will gradually decline at an accelerating rate in the coming decades (Chart 6). By 2050, the elderly population in these countries is expected to increase to 27% from 7% in 1995.)

Notwithstanding this important risk in post-Covid’s Asia, there is a silver lining, namely increasing regional trade integration. One important example of this trend is RCEP, which links ASEAN, China, South Korea, and Japan, into a trade deal. Still, it is important to note that the Regional Comprehensive Economic Partnership (RCEP) negotiations have been dragging for eight years and that the final agreement has been watered down in terms of key liberalization measures. Not only was the geographical coverage bigger when the negotiations started but the scope in terms of liberalization was also larger. Furthermore, when RCEP started as a response to the Trans-Pacific Partnership (TPP), the US-China strategic competition was just starting while it is now pooling RCEP members in different directions today. The best example is recent trade frictions between China and Australia but there could be many others. In the same vein, increasingly pervasive US sanctions against China targets will not help to make RCEP a success.

Against the backdrop of rather negative structural trends, except for regional integration, we have to be mindful of a number of key risks. The first and most obvious is a setback in the current narrative that the pandemic should come to an end by year-end, thanks to a flurry of vaccines. The low – but still important – the probability of a setback would constitute a huge shock for Asian economies as the fast recovery that we are expecting for 2021 would probably not materialize. This is more of the case for economies that have run out of fiscal and monetary space. The second is geopolitical. in fact, before Covid-19, the key risk to the global economy was the US-China tensions and rising deglobalization threatening regional stability and growth. The election of Joseph Biden, who is seen as less hawkish than President Trump, is unlikely to change the strategic competition between the US and China. Already, Biden said that he was not repealing the Phase 1 tariffs and other tariffs until a comprehensive review. His rhetoric is also seen as rather hawkish in recent days on China. And in the final days of his term, Trump has passed a series of executive actions that further put a wedge between China and the US that will require the Biden administration to reverse. In other words, while the Biden administration may put the floor to the US-China deterioration, it is very unlikely that it will reverse to the Obama years. So far, China has done well in recovering in 2020 thanks to its containment of the virus, which has helped with growth recovering. That said, US-China tensions still constitute an important risk for China in 2021, and the region as a whole. This is particularly the case as different stakeholders in the US call for additional actions to contain Mainland China, whether Congress or even NATO in its new position paper. Beyond the US, China-related tensions are growing elsewhere, especially in Australia. Beyond the straining of economic relationships, a more disruptive risk could come in the security realm, such as Taiwan and the South China Sea.

Conclusion

The Covid-19 pandemic has hit Asian economies hard, on top of what had already been difficult in 2019 due to the trade war, China’s decelerating growth, and other idiosyncratic issues, especially in India. As for the pandemic, the shock has been very different across geographies. Beyond the extent of lockdowns and the size of the policy response, whether fiscal or monetary, the underlying characteristics of Asian economies also explain differences in growth trends. Countries with current account deficits have suffered as risk-off episodes, especially last March, have complicated their necessary external funding, constraining their fiscal support. On the positive front, Mainland China, Taiwan, and Vietnam have managed to recover from the Covid shock faster not only because of a better sanitary response to the pandemic but also for structural reasons, related to their sectoral specialization. In fact, an important lesson to draw from the winners and losers of this pandemic is how important an early containment might be but also the sectoral specialization and the fundamentals, especially how costly it might be to depend on foreign funding.

Regarding policy response, the region has shown much more courage as opposed to previous crises even in emerging Asia. This is more the case on the monetary front than on the fiscal front – with the clear exception of Japan and Singapore. The introduction of full-fledged quantitative easing in some more geographies, such as Australia, and even in some emerging countries such as Indonesia, India, and the Philippines are welcome. Looking forward, most countries in the region would do well to improve the efficiency of fiscal policy for countercyclical purposes. The good news is that aggressive easing in developed markets has driven rates and the USD lower, helping with risk appetite.

Among major Asian economies, Mainland China has clearly been the first in and the first out with a rather robust recovery. We expect the recovery to continue to be supported by the roll-out of new vaccines. Against such background and supported by base effects and the impact of the 2020 fiscal policy stimuli, growth in 2021 will be much faster even if cyclical. The rotation away from Covid-19 sectors into the real economy will help old sectors, especially transportation, energy, and retail sales, as well as countries most dependent on them. Challenges of Covid-19 have also facilitated the progress of a number of reforms in India, Indonesia, and the Philippines, to which investors will pay even more attention as the clouds of the Covid-19 pandemic continue to be lifted. Japan, instead, will have a harder time in terms of lifting the economy beyond a statistical rebound and notwithstanding a much bigger fiscal and monetary stimulus. The minimal structural reform during the Abenomics years will continue to push down potential growth.

Overall, with growth staging a comeback and companies resuming investment after a massive drop in 2020, our outlook remains positive but not without acknowledging the hangover of the pandemic. In fact, faster debt accumulation is an important negative consequence of Covid-19 and the policy response, not only in Asia but globally. The second negative consequence is an acceleration of demographic problems due to the fall in the fertility rate across the globe. In Asia, this hits aging economies much more brutally than those with a still positive demographic dividend. On the positive side, there is a silver lining to Covid-19, namely a potential boost to regional trade integration thanks to RCEP.

Finally, a number of important risks remain in our positive scenario to 2021. The first and most obvious one relates to vaccine-related delays which could come from production or distribution bottlenecks but also renewed lockdowns. At the other end of the spectrum, an inflationary shock could appear due to supply constraints on the back of pent-up demand from a smooth vaccine rollout and widespread optimism. Supply constraints would obviously hit economies with current account deficits more severely. The third one comes from growing tensions between the US and Mainland China, especially as they move further from economics to security issues. Taiwan and the South China Sea are clearly the most important flashpoints. Finally, such a complicated geopolitical outlook, coupled with the lessons learned from Covid-19 regarding supply disruptions could push the reshuffling of value chains further, with important consequences for Asia. The risk of decoupling, or even deglobalization if more generalized, could actually extend beyond trade towards technology or even finance, with obvious negative consequences for growth in Asia and globally.