On the 5th of February 2018, the Dow Jones suffered the worst day in over six years. Followed by a global stock market plunge, the Index dropped in average 4.6% – or 1’175 points. It might not have been a drop with the same magnitude than in 1987 or 2008, but for investors, this means that they must be more cautious and that the marathon of record highs might very well come to an end.

Monday, the 5th of February

It seemed to be a common Monday for most of us. Even though the Dow Jones Industrial Average – the oldest, and probably most relevant, stock market index – showed some weakness the week preceding the crash, no one would have expected that it would experience the biggest drop, since 2011, on a single day.

This “earthquake” was felt all over the global financial world:

- The S&P 500 (major benchmark) dropped during the same day by 4.1%

- The FTSE 100 (London index) dropped by 2.64% to its lowest level since last April.

- The DAX (Frankfurt index) dropped by 2.83%

- Japan’s NIKKEI 225 index dropped by 4.6%

Image: Dow Jones Industrial Average (Source: Yahoo Finance)

Nevertheless, this was only a one-day crash… On Tuesday, markets were already recovering from those plunges. So, what could be the reason for this crash?

Are the algorithmic or technical traders responsible, as it happened before in 2010? Was it just a quick correction, as a consequence of overpriced markets? Or are there more profound reasons behind it? Here are a few plausible explications.

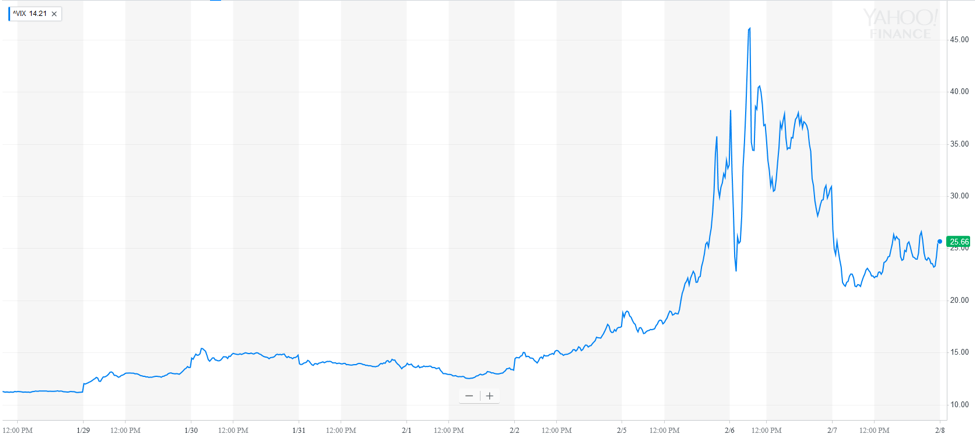

CBOE Volatility Index (VIX)

Even though a few would like to blame the high-frequency traders, it is very unlikely that they are responsible. As the name states it, high-frequency trading algorithms are performing transactions in the amount of 500’000 per second. In other words, the crash would have been much quicker and with a higher magnitude.

The CBOE Volatility Index, also called the “Fear-Index”, could be one of those plausible explanations. It hit the highest point since before President Trump’s election. The index determines the expected volatility in the S&P 500 over the next 30 days and is an indicator of the confidence of investors in the market. An increase of the index generally means that there is more uncertainty about future trends. At that time, a more risk-averse investor will try to get a risk-neutral position, by selling some of their securities.

CBOE Volatility Index (Source: Yahoo Finance)

On Monday, the VIX index jumped by approximatively 28%. The highest since the day of the Presidential election in the United States. Some analysts will blame the index, along with some other reasons, for the drop as it became very popular in recent years (https://www.ft.com/content/839c4d5c-0afb-11e8-8eb7-42f857ea9f09).

However, one might say that it could the other way around: volatility spiked because of the rapid decrease of index quotations.

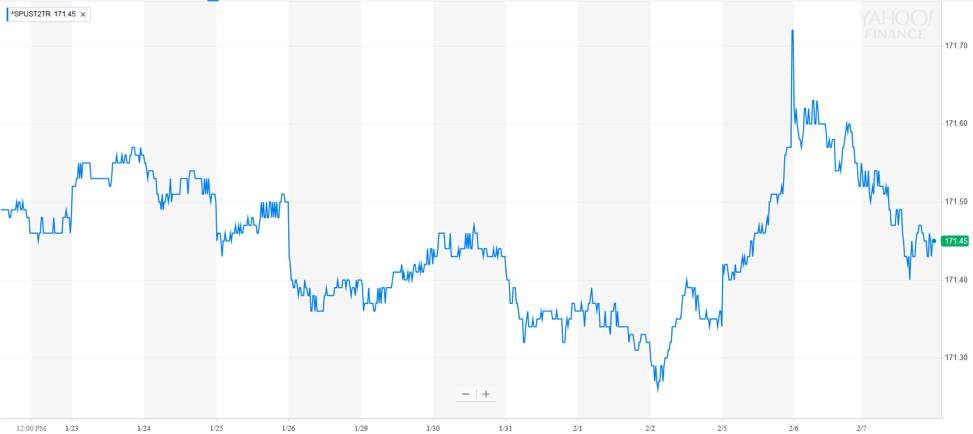

Increase in bond yields

By taking a more fundamental approach, it is important to consider bond yields.

To the basics of bonds: emitting bonds is the way of raising debt as a government. Generally, like in the United States and Germany, bonds are considered the safest investment possible. This is, since the probability of repayment by such economies is very high.

The yield and the price of bonds are inversely and non-linearly related. That is: a higher yield decreases the price, whereas a lower yield increases it.

During the week before Monday, yields were at their highest and therefore prices of bonds were quite low. Because of the happening on Monday and the relationship between the yield and the price, an increase in the price was to be expected (as seen in the following graph).

Image: 2 Year T-note prices (Source: Yahoo Finance)

When economic conditions push market participants towards safer investment – which is i.e. usually the case during a rise of unemployment and a recession – the yields (in other words, the revenue) are decreasing due to a higher demand for such risk-free assets. On the other hand, when economies are growing, and inflation is high, those same yields rise, and prices are cheap.

Higher rates should, therefore, have a positive effect on stock prices, but the stock market was spooked that inflation would start to rise quickly and the Fed would change its policies to strongly, hurting the recovery. Consequently, money that was invested in stock markets was moved from there towards bond markets, causing a sell-off and a drop in the equity markets.

Fear of the increase in interest rates and the foreseeable ending of Quantitative Easing

As stated in the previous paragraph, the fear of a rise in interest rates could be the main reason for Monday’s drop. As markets react to information and emotion of individuals, the statement that the Federal Reserve of the United States will most certainly increase the rate in the next meeting, investors got afraid that borrowing money in future will be more expensive – again.

Since 2008, interest rates were at their lowest. And to further stimulate economies, central banks all over the world followed a program of injecting large amounts of money into markets – the so-called Quantitative Easing (QE). Both decisions worked well enough to stimulate the global economy ever since, but consequently bloated stock markets, which were drowned under huge amounts of debts and cash. Many analysts would say that this “easy-money” is the reason for the record-breaking marathon that the DJI ran during the last decade, and some of them predicted a crash as markets are consequently highly over-valuated.

As, since a few years, economic growth is showing more sustainable rates (2-3%) again, central banks are starting to reduce the buying of never-ending debt (QE) and increase the interest rates of fear from over-inflation.

It is at the same time this over-inflation fear that quenched investors out of the market, as they fear that the tax reform that has been signed by President Trump recently will provoke the very same symptoms.

Like in every fairytale, there is an end. The returns on stock markets could not have been sustainable on the long-term. And this end might have happened now. Even though only one day after the stock market recovered, one can expect further corrections in the short-term and further shocks in the markets, that will relate with announcements of central banks.

Nevertheless, as it has always been the case with markets, big crashes are not predictable and forecasts for future development, as well as many theories behind crashes, will most certainly not be accurate.

Calling Monday the 5th February a 2018 a Black Monday would be an overrated statement. As Mark Carney, governor of the Bank of England said: “What has happened in volatility markets is not an entirely surprising development”. Investors should be more cautious in future, with an ending of QE and a rise in interest rates, but expectations for global economic growth remains stable.