Estimated reading time: 5 minutes

In the world of finance for micro and small and medium-sized enterprises (SMEs), there’s a clear division between two crucial groups: Capital Deployers and Capital Providers. On one side, we have micro, small, and medium enterprises in emerging markets, brimming with potential due to growing local demand and export opportunities.

On the other side are the Capital Providers from developed economies, where interest rates are low, leading them to seek higher returns through greater risk.

In order to address this division and its subsequent issues, we must look at the limitations to capital flow, and how we can solve these issues.

1. Capital Deployers – Micro, small, and medium enterprises (MSMEs) in emerging markets are experiencing growth driven by increasing local demand and the potential for exports. However, they face a significant challenge in obtaining sufficient funds to cover their working capital requirements and to finance business expansion. When these enterprises do receive additional capital, it often leads to further growth, as they are far from reaching the point of diminishing marginal returns.

International Finance Corporation (IFC) estimates that 65 million firms, or around 40% of formal micro and SMEs in emerging countries have an unmet financing need of $5.2 trillion every year. Astonishingly, these firms represent 90% of businesses and 50% of employment globally.

2. Capital Providers – Capital Providers are individuals and institutions who provide capital or extend credit, oftentimes from developed economies, where interest rates are typically low. As a result of the economic conditions, they are willing to seek out investments with higher risks, in exchange for the possibility of higher returns.

Millennials and Gen Z have higher economic power than any generation that preceded them. They earn more, save more, and invest early. More importantly, they are ready to invest in risky assets. For millennials, as per a Fortune commentary, 31% started investing before age 21, compared to only 9% of baby boomers and 14% of Gen X.

The demand and supply of capital are connected by banks, traditionally via sourcing deposits and offering loans. While a bigger question remains – can a small investment from a Gen Z or a boutique hedge fund traverse and finance micro enterprises in remote towns in emerging markets?

Capital should flow from the point of surplus to the point of optimal opportunity seamlessly and this is the real testament to a perfect capital market. What hinders this capital flow?

Three perspectives on hindrances to capital flow

1. MSMEs’ limitations

As per WTO publication, over 50% of trade finance requests by SMEs are rejected worldwide, as compared to just 7% for multinational companies. It indicates that global liquidity is concentrated among large institutions and their clients.

Why? MSMEs in emerging markets often lack audited financial statements and credit ratings from reputed agencies.

The unavailability of credit ratings creates an asymmetric perception of the creditworthiness of MSMEs and their business viability. The financial needs of MSMEs are usually below a certain benchmark, which makes handling their accounts an operational challenge for conventional commercial banks. This situation often forces MSMEs to reduce their growth plans in order to stay within their limited financial means.

2. Small investors’ limitations

Small investors often don’t have the chance to put their money into assets that are carefully vetted for creditworthiness, provide a wide range of investment options, and offer returns greater than those of bank deposits. Either investors knowingly take huge risks in equities or shift to risk-free low-yielding bank deposits.

3. Banks’ limitations

Commercial banks prefer lending to large corporates considering the availability of credit rating, collaterals, easy due diligence, and multi bank relations. Basel regulations requiring lower capital allocation corresponding to low-risk weighted assets (RWA) further encourage this prudent approach. In effect, large banks fail to notice the abundant MSME financing prospects in emerging markets.

Who can overpower these limitations and connect this gap?

Again, the answer seems to be ‘banks,’ as they are regulated, highly capitalised, and have stringent due diligence processes – hence they are aptly positioned to connect capital deployers and capital providers.

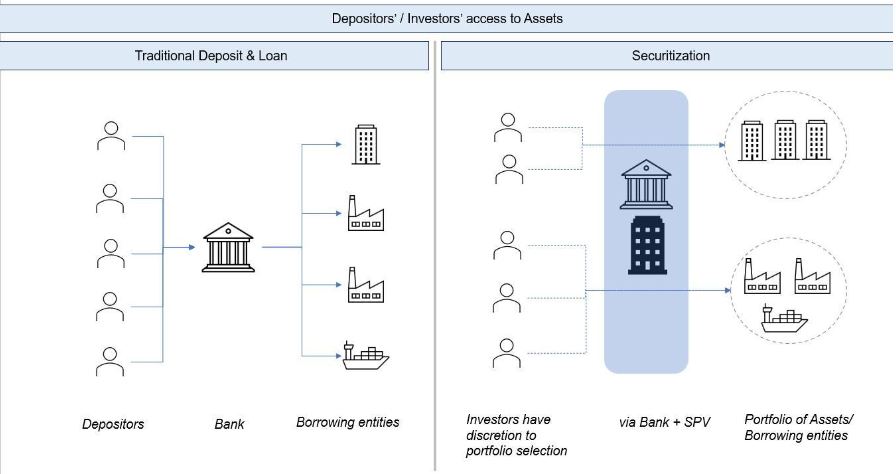

If traditional deposit and loan approaches can not bridge this gap, what are the options?

One of the possibilities is through “securitisation” of assets (or receivables) that are backed by real cash flows. As a lender, a bank can create a portfolio of select assets (loans, receivables), repackage them through an SPV (special purpose vehicle) and sell them to investors as interest-bearing securities.

Securities carry external credit ratings and bring risk-reward transparency. Cashflows from the borrowing entities pass through the bank and SPV to reach Investors as periodic interest (coupon) payments.

Taking this cue, large commercial banks can start lending or lend more to MSMEs, while sharing a portion of associated risk and return with investors.

As shown above, a depositor lacks the discretion to select a specific portfolio of assets, whereas, securitisation grants this decision-making authority to the investor.

What’s In It For Me (WIIFM) in view of securitisation?

Securitisation presents distinctive opportunities and challenges:

Opportunities:

- Interest-bearing securities can be fractionalised into digital tokens using blockchain technology that can attract a broader investor base (both institutional and retail).

- Once the modus operandi is in place, at regular intervals, banks can package assets and issue securities via SPV.

Challenges:

- In a high-interest rate regime, securitised assets should compete with bank deposits on the yield to attract investors.

- Client coverage costs will significantly go up for large banks while expanding their reach to MSMEs in emerging markets.

The securitisation of retail loans is not new in matured economies. Applying this approach to MSMEs, particularly in emerging markets, is a game changer.

It’s a win-win for both MSMEs and investors as it bridges the finance gap and creates a new asset class for investment. Banks also win as they de-risk exposure, expand the customer base, and cross-sell products.

Above all, nurturing MSME aspirations broadens the financial inclusion net and propels global economic growth faster.

The views expressed in this article are solely of the author and do not necessarily reflect the opinions of his employer.