Estimated reading time: 5 minutes

The African economy has suffered three major shocks in quick succession, namely, the COVID-19 pandemic, spillovers from geopolitical tensions and supply chain disruptions. This, coupled with widening fiscal deficits, exchange rate volatility and natural disasters have eroded the fiscal space of African economies and increased debt levels.

More recently, the monetary tightening policies, particularly in advanced economies has made it expensive for African governments to service their existing debts. With approximately 40% of Africa’s debt denominated in foreign currency, the risk of sovereign default remains elevated.

The World Bank indicates that the last three years have seen more defaults than the entire last two decades before; with 18 sovereign defaults in developing countries. African countries are therefore under immense pressure to review and renegotiate their debts in order to avoid further defaults on their obligations.

The advent of the Creation of the Global Sovereign Debt Roundtable, which also includes the private sector and borrowing countries, marked another step forward. However, the IMF has indicated that it will adopt a country-focused approach in dealing with sovereign debt issues while preparing for a systematic approach should the need arise.

Debt and financing: A changing environment

The continent still faces a big financing gap. Multilaterals have bemoaned increasing debt servicing costs which are crowding out investment in infrastructure, health and green projects, amongst others.

Country debt profiles are increasingly comprised of non-concessional borrowing, complicating debt restructuring in case of defaults and increasing risk aversion. Some of the countries have made efforts to restructure their debts to reduce the burdens; for example, the IMF has approved an Extended Credit Facility of US$3 billion to support Ghana’s efforts in restoring macroeconomic stability, ensuring debt sustainability and promoting more inclusive growth.

The rising debt in Africa and the high risk of sovereign default hampers the activities of export credit agencies (ECAs) on the continent. However, this challenge has also presented opportunities for flexibility, for example, cover for down payments, higher percentages of cover for both political and commercial risks, as well as longer tenors.

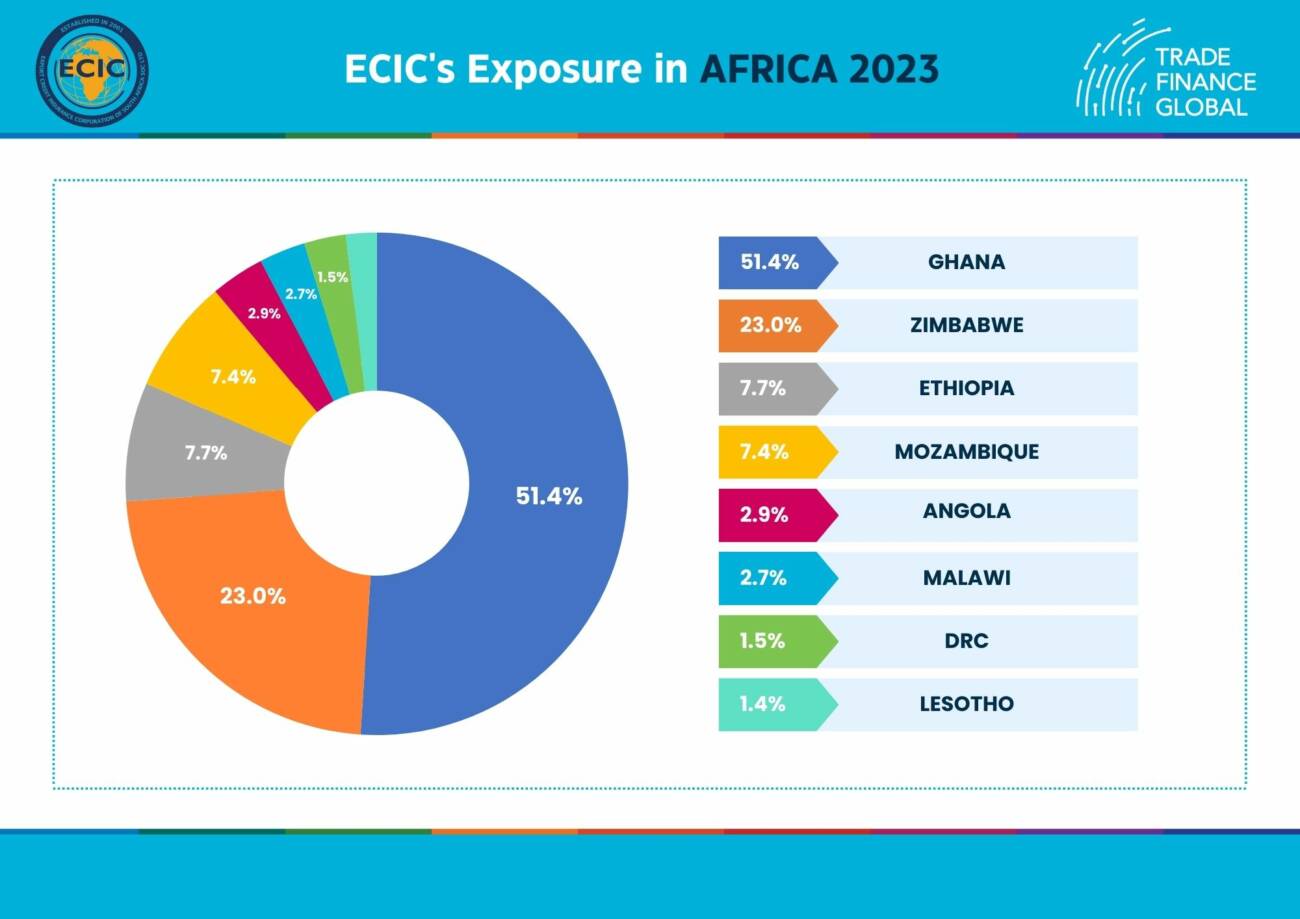

The continent facing debt issues, continues to be a major playing field for Export Credit Insurance Corporation of South Africa (ECIC SA), with Ghana accounting for 51.4% of total exposure, followed by Zimbabwe and Ethiopia at 23.0% and 7.7%, respectively.

From an industry viewpoint, the ECIC portfolio has shifted away from its traditional mining focus. Currently, power generation leads as the top sector, accounting for 45.8% of total exposure, with construction following closely at 40%.

Economic backdrop of the region

Frail macroeconomic fundamentals, including high debt levels, weak fiscal balances, an uncertain economic growth outlook and an acute funding squeeze are all at play and creating a challenging environment for ECAs to underwrite sovereign projects in the Sub-Saharan Africa (SSA) region.

Even those which displayed darling economic prospects, are riddled with debt default contagion fears. Meanwhile, prudent fiscal policy is not supported by stimulus policies that boost economic growth in the medium term. The current risk-averse environment, with an acute funding squeeze as a result of tightened financial conditions, has resulted in SSA countries having limited access to affordable external financing.

Despite the precarious economic backdrop in the region, lenders and ECAs still have some appetite to continue underwriting sovereign projects in SSA, instead of amplifying the funding squeeze. Adjustments aimed at providing security and cushioning to lenders and ECAs that are more stringent in the event of default are being worked into contracts.

Credit enhancements in sovereign contracts are now a focal point and include among others,

- Assets pledged as security for an obligation;

- Contingent equity commitments;

- Revenues in the form of royalties or hard currency;

- Revenue linked to a wealth fund or levies;

- Funds kept in offshore accounts and incorporating debt service reserve account, to name a few.

This encourages continued investment in the region while ensuring lenders and the ECA’s are also sufficiently protected.

ECIC SA continues to have appetite, with a solid pipeline on the continent despite the risks associated with the rising debt levels. The availability of ECIC SA products on the continent is critical in achieving intra-Africa trade and accelerating the pace of industrialisation.

The corporation continues to engage with governments and multilateral institutions to find solutions, particularly credit enhancements to enable prudent lending in countries facing payment difficulties, or those currently at high-risk of debt distress.

Furthermore, the corporation will continue to diversify its exposure to minimise vulnerability to single markets and further increase collaboration with other ECAs to limit the risks associated with full exposure in debt-distressed countries.

Noting the shift, ECIC SA launched a new product within its line of business called Trade Credit Insurance, and also revived its bond and working capital product offerings in efforts to close the gap as most insurers had limited appetite for short-term transactions on the continent.

This will be a major boost to trade and enable South African companies to expand their footprint on the continent, with the implementation of African Continental Free Trade Area Agreement (AfCFTA).

Editor’s Note: This article was written by the Political, Economic, Analysis & Research (PEAR) Unite at ECIC SA.