Australia

Australia Hong Kong

Hong Kong Japan

Japan Singapore

Singapore United Arab Emirates

United Arab Emirates United States

United States France

France Germany

Germany Ireland

Ireland Netherlands

Netherlands United Kingdom

United Kingdom

Accelerating trade digitalization to support MSME financing

Micro, small and medium-sized enterprises (MSMEs) are the backbone of the economy, representing 95 per cent of all companies worldwide and accounting for 60 per cent of employment. They are fundamental to the day-to-day provision of goods and services around the world. Yet, many struggle to grow and trade. Among the many challenges that MSMEs face, lack of access to finance, including trade finance, is frequently identified as a critical barrier to growth. The MSME financing gap is a reality that cannot be ignored and that should be tackled with determination if we wish to ensure that small players are given a chance to thrive.

Digital technologies from cloud computing, to APIs, the internet of things, artificial intelligence and distributed ledger technologies open a range of new opportunities in this respect. New business models and new approaches to MSME financing are emerging. The technology is there, holding interesting promises. Yet, MSMEs continue to struggle to access financing, including trade finance, with ripple effects on their ability to grow and trade. How can we unleash the potential of these technologies?

The current pandemic, which has had a devastating impact on small businesses, has shown that going digital is no longer optional. It is necessary. But digitalization requires more than simply technology. It requires an enabling regulatory environment.

This publication explores how digital technologies can be leveraged to facilitate MSME financing. It provides examples of relevant use cases and discusses challenges faced by practitioners. While the potential of digital technologies to facilitate MSME financing is significant, this publication shows that a more holistic approach is needed to unleash the potential of these technologies to facilitate MSMEs’ access to finance, including trade finance. Coordinated action on issues ranging from standards, to how to leverage data and what type of data, digital identity, regulation and how to close the digital divide is needed. Policy-makers, technologists, practitioners, bankers, and all other stakeholders must work together to devise, agree, and then execute upon a roadmap that will catalyze action.

We need to think small and act big!

Foreword, by:

TradeTech Hub

1 | TradeTech – Home

2 | The Role of Technology in Trade

3 | Cloud Computing

4 | Optical Character Recognition (OCR)

5 | Internet of Things (IoT)

6 | Application Programming Interfaces (API)

7 | Distributed Ledger Technology (DLT)

8 | Big Data Analytics

9 | Artificial Intelligence (AI)

10 | Quantum Computing

11 | TradeTech Research

12 | 2021 Whitepaper

13 | ITC AI Guide

Authors

Contents

- Foreword from Xiaozhun Yi, Deputy Director-General, World Trade Organization (WTO) and John W.H. Denton AO, Secretary General, International Chamber of Commerce (ICC)

- Author’s Introduction

- Trade Digitalization and Financing: new hope for MSMEs?

- The role of technology

- Digital technologies in trade

- Appendices

Copyright © Trade Finance Global 2020. Please reference Trade Finance Global when citing this publication

Imagine how different the world might look today if, in 1976, Apple Computer couldn’t get the US$ 15,000 in financing they needed to buy the parts to fulfill their first order. How many entrepreneurial visions with the potential to change the world have fizzled out of existence due to a lack of funds? Dead in the water without so much as a chance for life.

For many micro, small and medium-sized enterprises (MSMEs) around the world today, access to financing can mean the difference between prosperity and bankruptcy. Working to identify, understand, and ultimately overcome the challenges that MSMEs face in their quest for acquiring financing will help ensure that the next Apple Computer doesn’t cease to exist before it has a chance to change the world.

This publication seeks to identify some of these most pressing challenges, understand them, and explore the potential application of digital technologies to mitigating their impact. To that end, interviews have been conducted and surveys administered with experts in the field of MSME financing, including in some cases trade financing, to shed light on these issues and explore the ways that technology can be used.

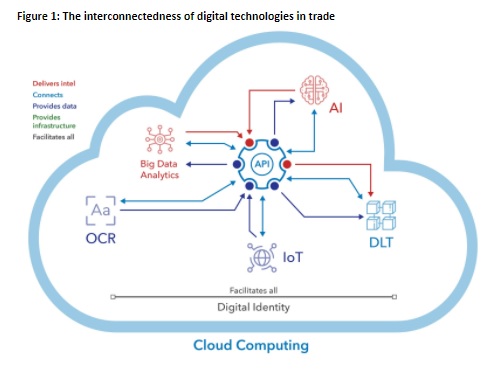

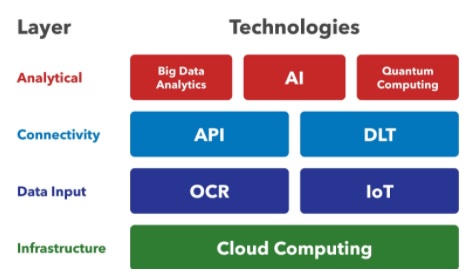

This publication will begin by examining some of the challenges that have been identified as impacting MSME financing, as well as the role that the COVID-19 pandemic has had in moulding the landscape. Next, it will move on to examine key digital technologies, their potential benefit to the industry, in particular to MSME financing, the adoption challenges they face, a selection of case studies and companies utilizing these technologies, and recommendations for overcoming these challenges. These technologies include cloud computing, optical character recognition (OCR), internet of things (IoT), big data analytics, artificial intelligence (AI), quantum computing, distributed ledger technology (DLT) and application programming interface (API).

Premier Launch Video

Assistant Editor and Lead Researcher

Carter Hoffman, Trade Finance Global

Carter is a Research Associate at Trade Finance Global focusing on the impact of emerging technologies on international trade. He holds international business and science degrees from Brock University in Canada and the European Business School in Germany. Carter’s work has been featured in publications and articles supported by the SME Finance Forum, managed by the International Finance Corporation, World Trade Organization, and International Chamber of Commerce.

Want to read our previous papers?

TFG and WTO published Blockchain & DLT in trade: Where do we stand in November 2020. The previous paper, TFG / ICC and WTO’s publication “Blockchain & DLT in trade: A reality check” in November 2019 at the WTO Global Blockchain Forum is available here.

Industry Association Partners

Contributors

- Wahida Mohamed Athman Ali, Islamic Fintech Hub of Sub Saharan Africa

- Stephen Arnold, Helaba

- Raphael Barisaac, UniCredit

- Kris Van Broekhoven, KomGo SA

- Dai Bedford, Ernst & Young LLP

- Oliver Belin, TradeIX/Marco Polo

- Colin Camp, Pelican

- Andre Casterman, Casterman Advisory, ITFA

- Natasha Condon, J.P. Morgan

- Nicholas Demetriou, essDOCS

- Arnaud Doly, Nabu

- Kate Drew, CCG Catalyst

- Sean Edwards, ITFA

- Thomas Frossard, Tinubu Square

- Merisa Lee Gimpel, Lloyds Banking Group

- Christoph Gugelmann, Tradeteq

- Lars Hansén, Enigio Time AB

- Hans Huber, Commerzbank

- Agnès Hugot, Fast Track Trade

- Daniel Huszár, efcom GmbH

- Katrin Kahr, Raiffeisen Bank International AG

- Atul Khekade, TradeFinex Tech Ltd.

- Michelle Knowles, Absa Group

- Joshua Kroeker, Contour

- Oswald Kuyler, ICC DSI

- Cecile Andre Leruste, Accenture

- Rebecca Liao, Skuchain Inc.

- Iain MacLennan, Finastra

- Pamela Mar, Fung Group

- Vinay Mendonca, HSBC

- David Meynell, tradefinance.training

- Barbara Meynert,Fung Group

- Marta Mróz-Sipiora, Asseco Poland

- Peter Mulroy, FCI

- John Omoti, Bank of China

- Samantha Pelosi, BAFT

- Joel Schrevens, China Systems

- Dr. Paul Sin, Deloitte Consulting

- Michael Sugirin, Standard Chartered

- Shona Tatchell, Halotrade

- Marc Vandermolen, KBC

- Michael Vrontamitis, Trade Digitalisation Working Group, ICC Banking Commission

Infographics, Charts & Diagrams

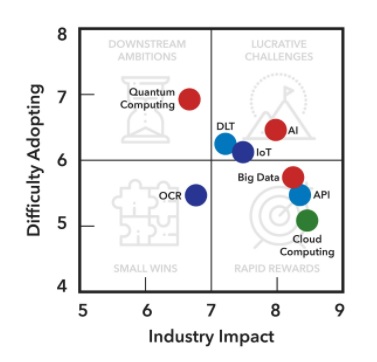

Source: Research by ICC, TFG and WTO

Source: Research by ICC, TFG and WTO

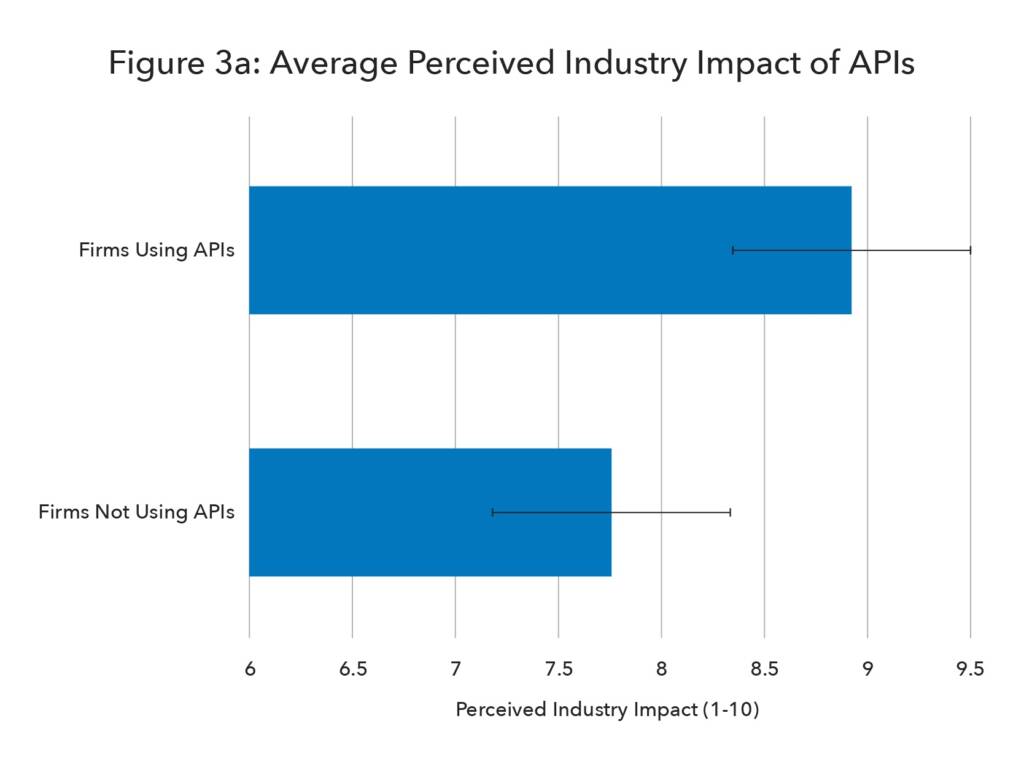

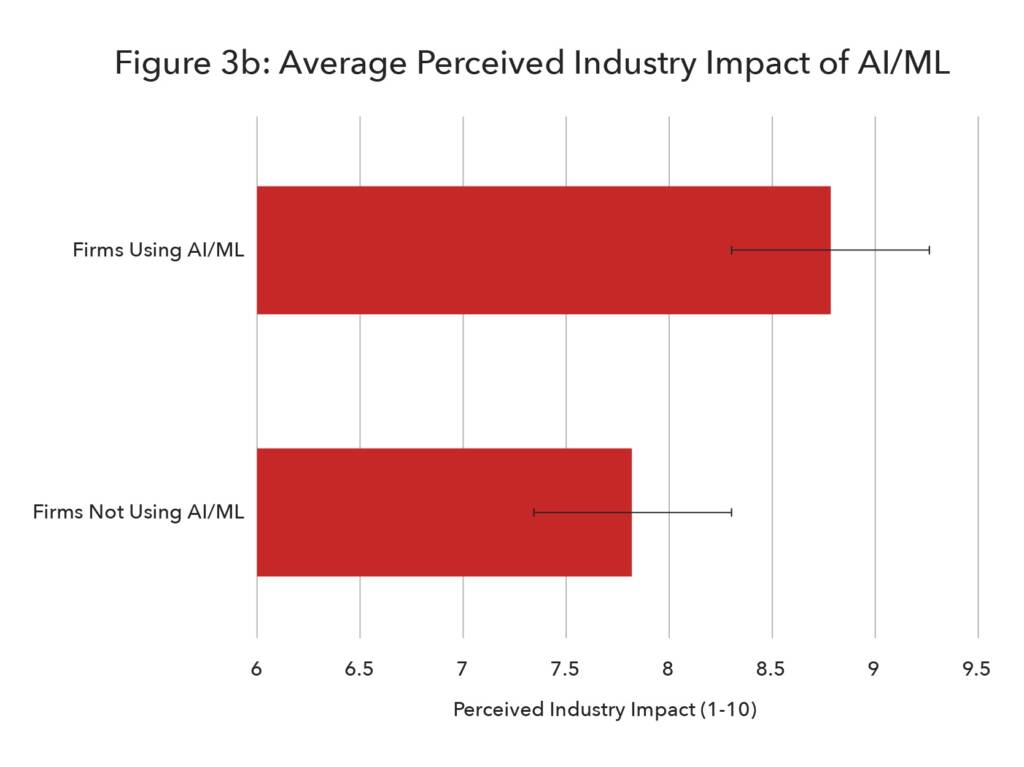

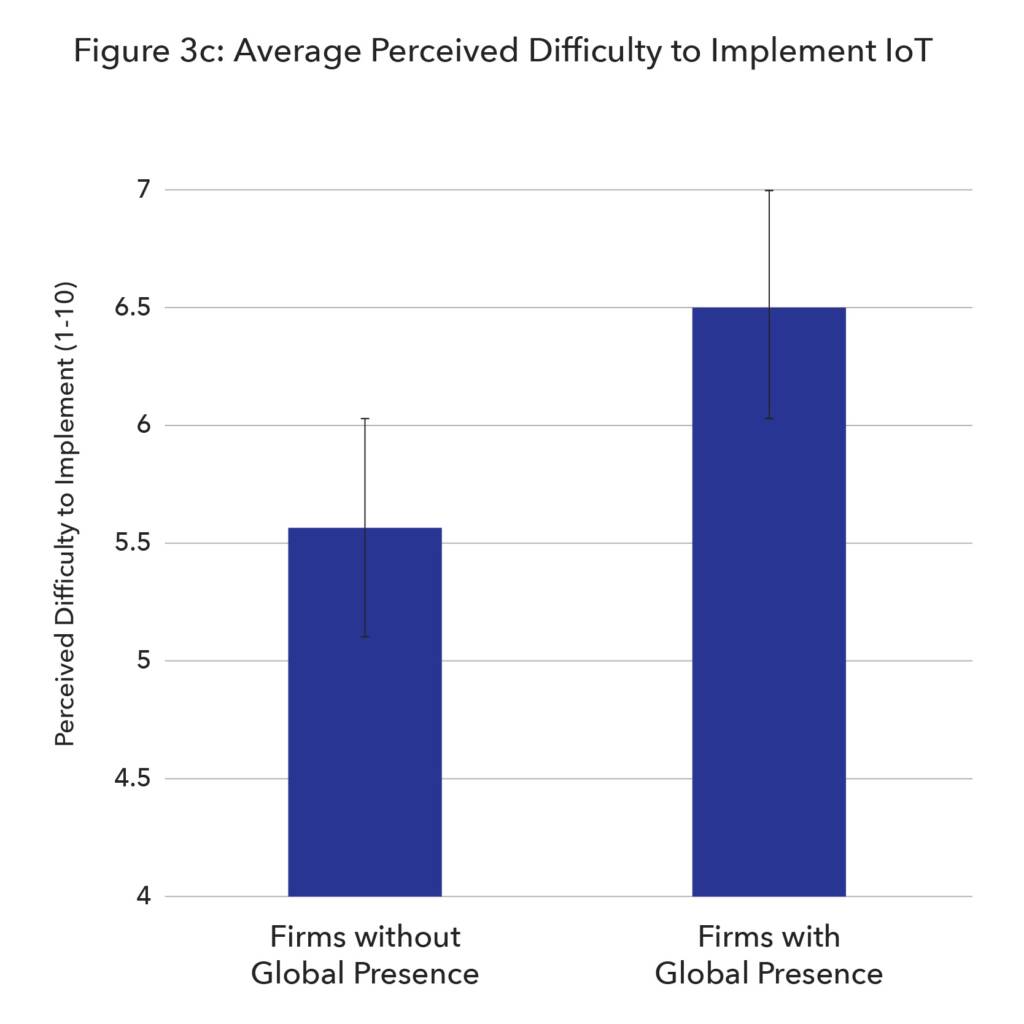

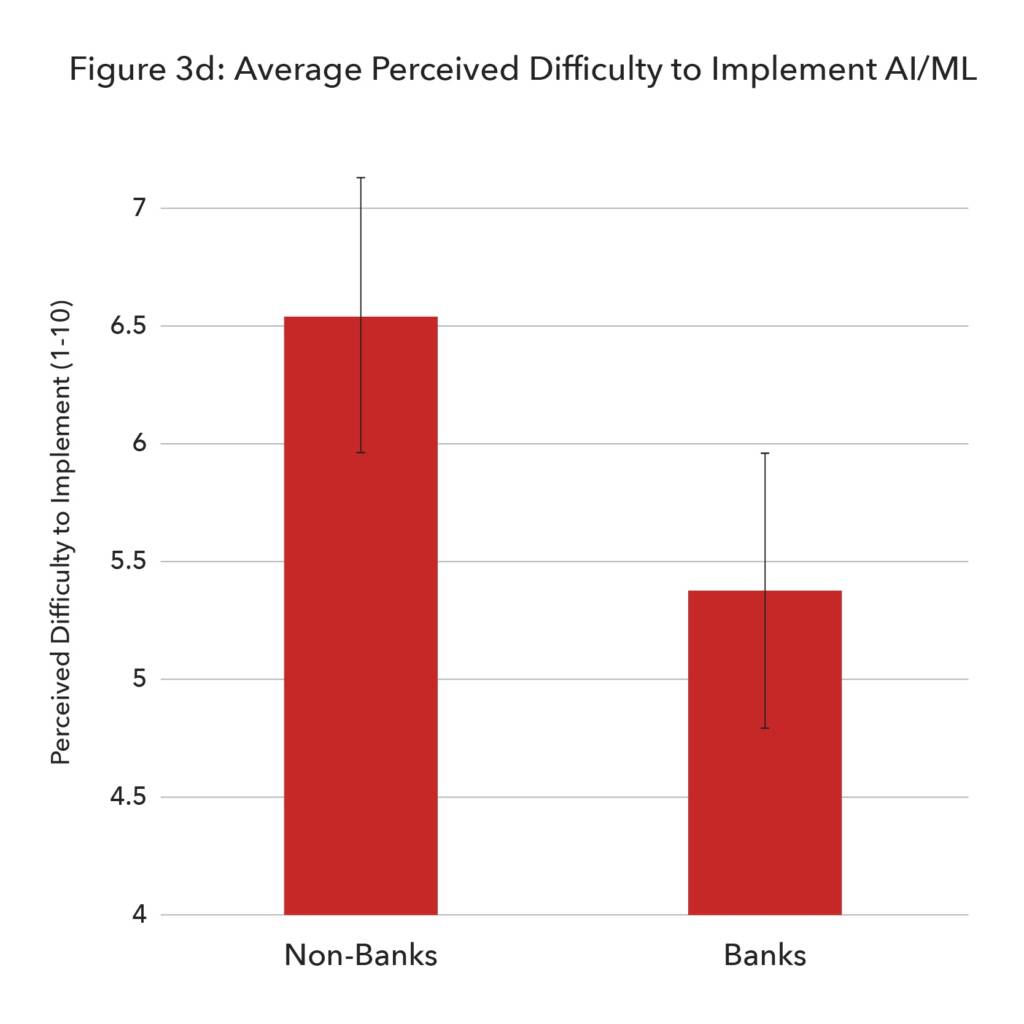

After plotting the aggregate data points in the above matrix, further analysis was conducted to determine if there is any significant variation in these perceptions of impact and difficulty between the different self-identified stakeholder groups represented in the survey responses. Specifically, this analysis focussed on differences between (1) firms using each technology to facilitate financing and firms that are not, (2) firms with a global presence and those with only a regional or local presence, (3) firms identifying as banks and those not identifying as banks, and (4) firms identifying as financiers and firms not identifying as financiers.

Most of the analyses did not unveil statistically significant differences amongst the groups (i.e. firms using cloud to facilitate financing and firms not using cloud to facilitate financing perceive cloud as having, on average, an equal impact on the industry). There were, however, four instances where statistically significant differences were found:

Comments are closed.