- Indonesia faces a critical energy security gap, with limited oil reserves and a daily supply shortfall forcing heavy reliance on costly imports.

- Structural weaknesses in refining capacity and uneven storage distribution increase supply chain risks, particularly for eastern regions of the archipelago.

- Achieving energy resilience requires expanding storage hubs, boosting domestic refining, diversifying supply sources, and decentralising infrastructure investment.

Indonesia’s energy security is facing a critical situation. With over 280 million people, Indonesia is the fourth-most populous country in the world, and its economy is growing rapidly: yet its energy supply is worryingly limited.

Currently, Indonesia maintains an operational oil inventory of only 23 to 25 days – a significant shortfall to the International Energy Agency’s (IEA) 90-day benchmark. This is a logistical hurdle, yes: but it also represents a liquidity crisis for the world’s most essential resource.

In the realm of finance, a lack of liquid reserves leads to insolvency; in the realm of national security, it leads to paralysis. Indonesia has long been exposed to risk as a result of inadequate storage, and the clock is ticking for the issue to be tackled.

The escalating conflict in the Middle East and renewed threats to the Strait of Hormuz serve as a harsh wake-up call. Indonesia no longer has the luxury of waiting for global markets to stabilise. To protect its GDP growth and to ensure social stability, the country must transition from being a passive buyer to emerging as an active operator of its energy infrastructure.

The existing operational reality

1. Refining capacity vs demand

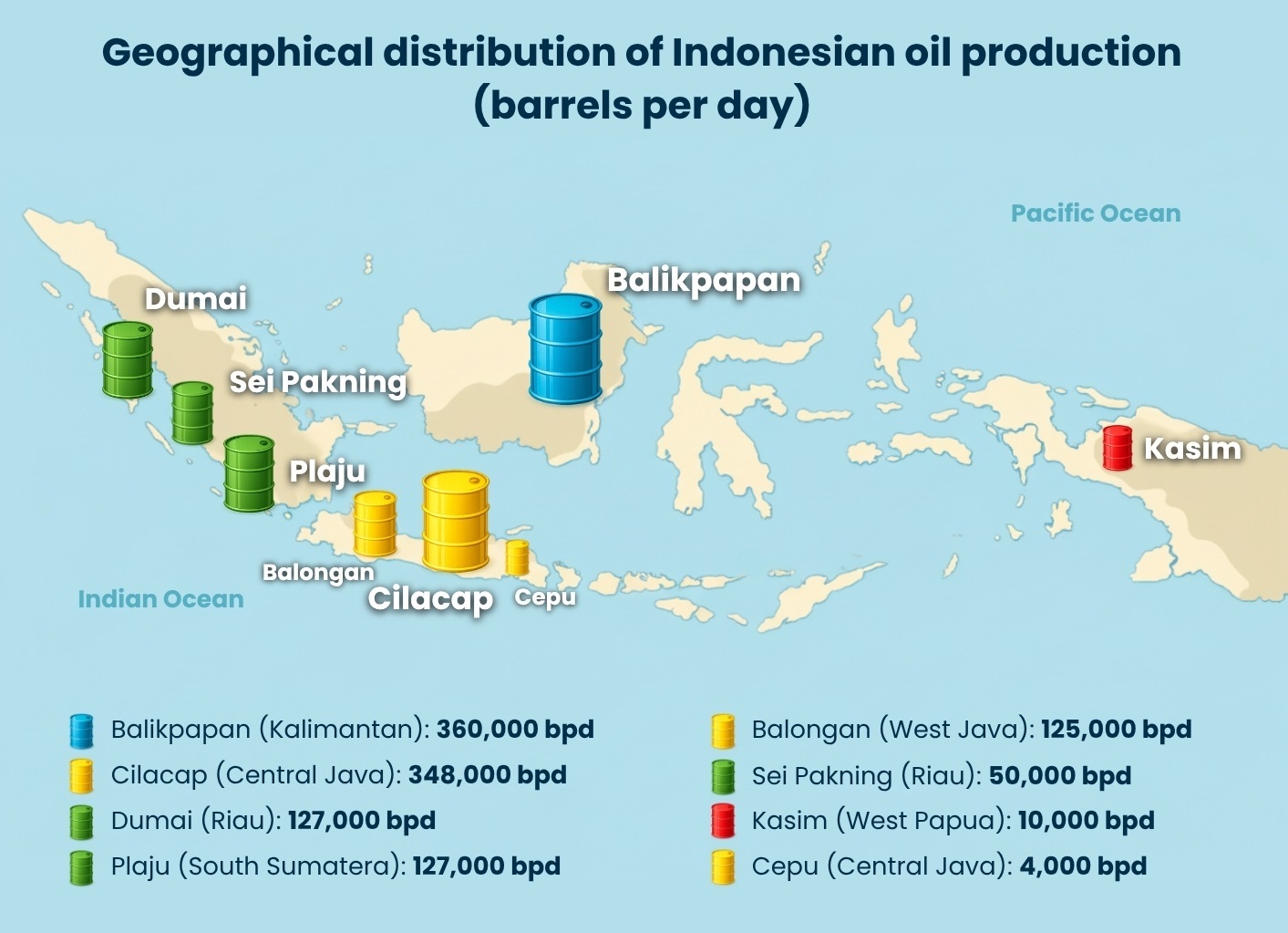

Indonesian state-owned Pertamina currently operates eight oil refineries, with a total capacity of approximately 1.2 million barrels per day (bpd). However, with domestic consumption reaching 1.6 million bpd, the country faces a structural daily deficit of 400,000 bpd.

This gap is currently bridged by importing expensive petroleum products, often through third-party traders, which adds a layer of ‘middleman’ costs and reduces Indonesian sovereign control over the supply chain.

2. Storage concentration risk

The current landscape of storage hubs across Indonesia reveals a heavy concentration to the west of the country, leaving the eastern region underserved and creating a massive internal supply chain risk.

The islands Java and Sumatra hold the lion’s share of national reserves, while Kalimantan serves as the nerve centre for the 2026 refinery development master plan (RDMP).

Conversely, Sulawesi, which is located to the east of Borneo, and Papua, Indonesia’s easternmost province, are limited to small ‘distribution’ terminals, with no significant strategic reserve capacity.

A reliance on imports

Lifting refers to the process of drilling wells and bringing raw crude oil and natural gas from underground reservoirs to the surface. Refining, on the other hand, is the industrial process of transforming raw crude oil into usable petroleum products.

Last year, Indonesia had an average crude oil lifting of 605,300 bpd, having achieved 100% of its target for the first time since 2016. For this year, the government has raised the target to 620,000 bpd. However, although production is stabilising, it remains far below national demand, requiring significant imports to sustain the economic engine.

Given that the total refining capacity of the country is 1.2 million bpd per day, and the daily consumption of petroleum products is 1.6 million, there is a petroleum product shortage of 400,000 barrels per day.

For crude oil, the average lifting amount hovers around 600,000 bpd, which, when subtracted from the total refining capacity, equates to a shortage of 600,000 bpd. This means that the total daily import requirement for crude oil and petroleum products for Indonesia is roughly 1 million bpd.

The four-pillar strategy for resilience

To achieve true energy sovereignty, Indonesia must execute two urgent mandates: build additional storage in the eastern region and develop medium-sized refineries to close the daily consumption gap.

- Expanding storage: The Bitung strategic hub

Because Indonesia is an archipelago – a cluster of islands scattered across a the sea – a single energy centre in Java is inefficient and strategically dangerous. Bitung, located in the North Sulawesi province, is perfectly positioned to become the primary eastern port hub.

As an international port hub and special economic zone (SEZ), Bitung provides a ‘back door’ to the Pacific, bypassing the congested and vulnerable Malacca Strait.

Geographically, Bitung offers a natural draft of 12 to 15 meters and is shielded by the Lembeh Strait, making it ideal for very large crude carriers (VLCCs). Its proximity to the Pacific significantly reduces shipping times to and from the west coast of the US and the Americas.

By integrating large-scale onshore storage with floating storage using VLCC tankers (which involves repurposing these massive tankers as stationary offshore holding tanks rather than transport vessels), Bitung can ensure that Maluku, Ternate, and Papua remain resilient, even if western supply lines are disrupted.

- Prioritising domestic lifting and upgrading

For decades, Indonesia’s reliance on imports has exposed its trade balance to global price shocks. Policy must mandate that domestic oil lifting is prioritised for national refineries first. Maximising domestic assets could improve Indonesia’s national credit profile and reduce the need for external borrowing.

The 2026 Balikpapan RDMP upgrade, which brought the Balikpapan refinery to the European Union’s EURO V standards, enforced strict emissions limits. The initiative proved that Indonesia can meet international environmental standards, while simultaneously strengthening domestic supply.

- Diversifying sources through counter-trade

Currently, 25% of Indonesian crude oil comes from the Middle East. Thereby, the continuation of the effective closure of the Strait of Hormuzwould be a national catastrophe.

Although the February 2026 Agreement on Reciprocal Trade (ART) with the US provides a more secure, Office of Foreign Assets (OFAC)-compliant supplier base that aligns with the US’ regulatory and legal standards, Indonesia should also pursue aggressive counter-trade agreements.

By swapping and capitalising the country’s abundant natural resources, such as nickel, coal, rubber, or crude palm oil (CPO) directly for crude oil, Indonesia can bypass the volatility of the US dollar and preserve vital foreign exchange (FX) reserves.

From a commodity trade finance (CTF) perspective, this ‘commodity Swap’ model reduces currency risk and ensures Indonesia’s natural wealth is used as direct leverage for energy security.

- Decentralising refining: Medium-sized facilities

Indonesia must complement its ‘mega-refineries’ by investing in medium-sized refineries in different relevant zones. This eliminates the ‘archipelagic tax’, the extreme cost of transporting refined fuel across thousands of islands.

Refining locally minimises logistics costs and provides regional energy independence. If a disaster or conflict strikes one zone, the others can continue to function, preventing a total national shutdown.

Strategic challenges to overcome

Despite their urgency, it’s crucial to recognise that these solutions face significant institutional hurdles.

For these solutions to be successfully implemented, Indonesia has to move away from its ‘everything is easy to get’ complacency that has defined its energy policy for decades.

On top of this, building storage and refineries requires substantial capital. SEZ incentives and creative financing must be leveraged to attract global investors.

Tying the two together, Indonesia is currently battling a lack of synergy. Success is subject to integrated coordination between the Ministry of Energy, Pertamina, and the Ministry of Finance.

Indonesian President Prabowo Subianto upholds a 100% renewable energy vision for 2035. This is expected to be achieved through accelerating biodiesel (moving from B50, which is 50% biodiesel, 50% petroleum diesel, to B100, which is 100% pure biodiesel) and developing 100 gigawatts (GW) of solar and geothermal power.

However, a green future cannot be guaranteed if the current economy stalls due to an energy shortage.

—

A crisis is often a blessing in disguise, and the current global tensions have pushed Indonesia to a point where being passive is no longer an option. By expanding storage in hubs like Bitung, developing new medium-sized refineries, utilising creative counter-trade efforts, and decentralising the country’s refining capacity, Indonesia can build a foundation for permanent stability.

If executed successfully, Indonesia can turn this wake-up call into true energy independence and long-term sovereignty.